Please use a PC Browser to access Register-Tadawul

Get It

Wells Fargo (WFC): Exploring Valuation as Shares Dip 2% This Week

Wells Fargo & Company WFC | 74.10 | -1.53% |

Despite this week's share price dip, Wells Fargo has shown solid momentum over the long haul with a 17.4% year-to-date share price return and an impressive 12.5% total shareholder return over the past twelve months. With performance like this, sentiment may be shifting as investors weigh both recent volatility and the bank’s strong multi-year gains.

If you're curious about what other opportunities are out there, now is an ideal moment to broaden your search and discover fast growing stocks with high insider ownership

With shares trading just below analyst targets and a healthy track record of growth, the big question for investors is whether Wells Fargo remains undervalued or if its future prospects are already baked into the current price.

Wells Fargo's most widely followed valuation narrative places its fair value significantly above the recent closing price, positioning shares as undervalued according to consensus expectations. The narrative draws on both recent performance improvements and optimistic projections for the bank's future profitability.

A strong focus on digital banking and client experience improvements has driven consistent gains in mobile banking adoption, digital account openings, and customer satisfaction. This positions Wells Fargo for scalable growth and cost efficiencies, supporting both revenue growth and net margin expansion as more banking activity shifts online.

Want to see what assumptions drive this bullish outlook? The real story is hidden in growth estimates and a well-above-average future profit multiple. Find out which performance factors the narrative is betting on, then decide whether the numbers add up.

Result: Fair Value of $93.54 (UNDERVALUED)

However, sustained competitor pressure or slower than expected digital transformation could quickly challenge the optimism behind Wells Fargo’s current valuation narrative.

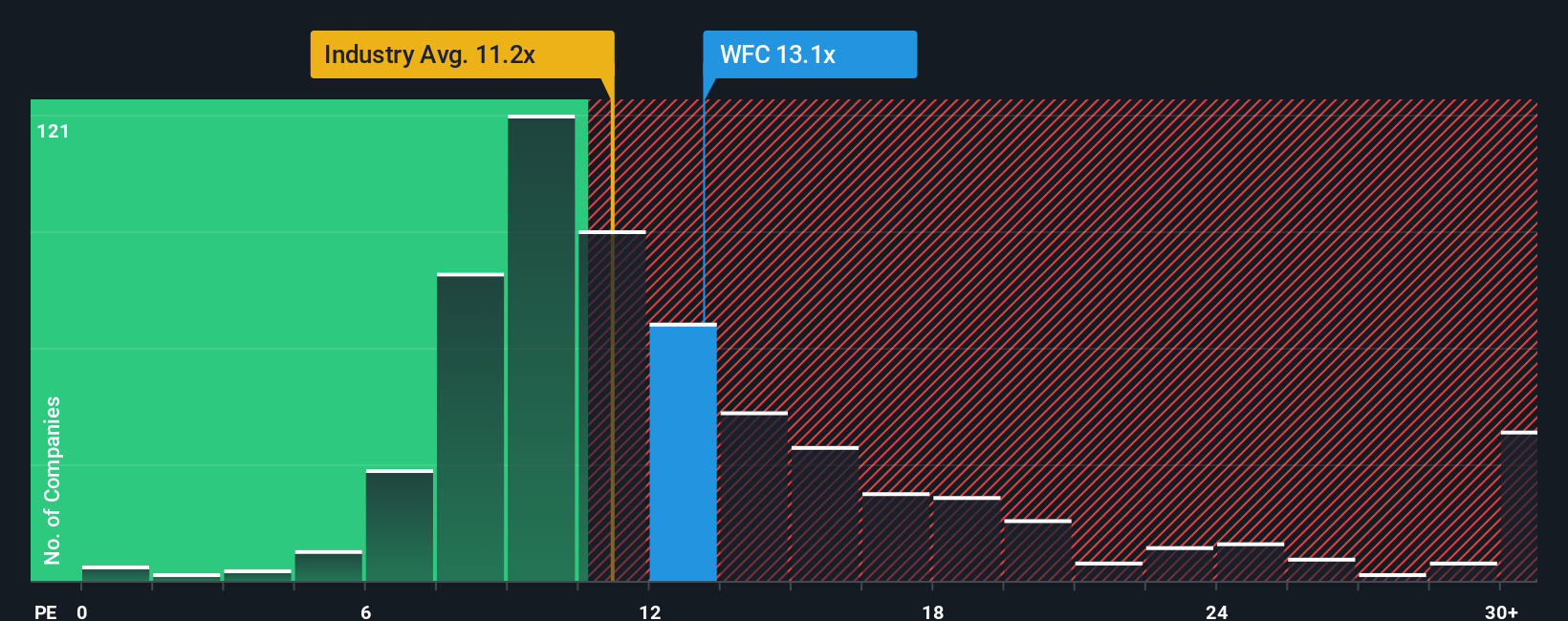

While Wells Fargo appears undervalued versus fair value estimates, a look at its price-to-earnings ratio tells a different story. Shares currently trade at 13x earnings, which is more expensive than both peer (12.1x) and industry (11x) averages. The market’s fair ratio, based on trends, sits at 13.9x. This means Wells Fargo’s premium price relative to competitors could pose risks if growth expectations fall short. Does the market’s higher valuation signal confidence, or does it caution us to keep expectations in check?

If you see things differently or want to dig through the numbers on your own terms, you can build a personalized view in just a few minutes. Do it your way

A great starting point for your Wells Fargo research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

Don't let your investing journey stop here. There are standout opportunities you could be missing across fast-growing sectors and innovative niches. Take action before others do.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.