Please use a PC Browser to access Register-Tadawul

Get It

What Paycom Software (PAYC)'s Enhanced HR Automation Tools and New EY Study Mean for Shareholders

Paycom Software, Inc. PAYC | 166.61 | +0.32% |

We've found 17 US stocks that are forecast to pay a dividend yield of over 6% next year. See the full list for free.

To own Paycom Software stock, investors need to believe that automation and AI-driven innovation will keep Paycom at the forefront of HR cost savings, fueling ongoing adoption and competitive differentiation. The latest Direct Data Exchange® upgrades, underpinned by EY-reported rising costs for manual HR processes, reinforce the near-term catalyst of higher client engagement and retention. However, the update does not materially alter the major immediate risk that widespread industry adoption of similar AI tools could narrow Paycom's differentiation and pressure margins.

Among recent announcements, the launch of “I want,” Paycom’s command-driven AI engine, stands out as most relevant. With EY’s report reflecting the steep labor costs tied to manual HR data searches, “I want” directly addresses growing client demand for cost reduction and efficiency, supporting Paycom’s case for platform stickiness and increased revenue per user in the quarters ahead. Still, the potential for further product commoditization among competitors...

Paycom Software's outlook anticipates $2.5 billion in revenue and $586.5 million in earnings by 2028. Achieving this would require 8.1% annual revenue growth and a $170.8 million increase in earnings from the current $415.7 million.

Uncover how Paycom Software's forecasts yield a $246.69 fair value, a 19% upside to its current price.

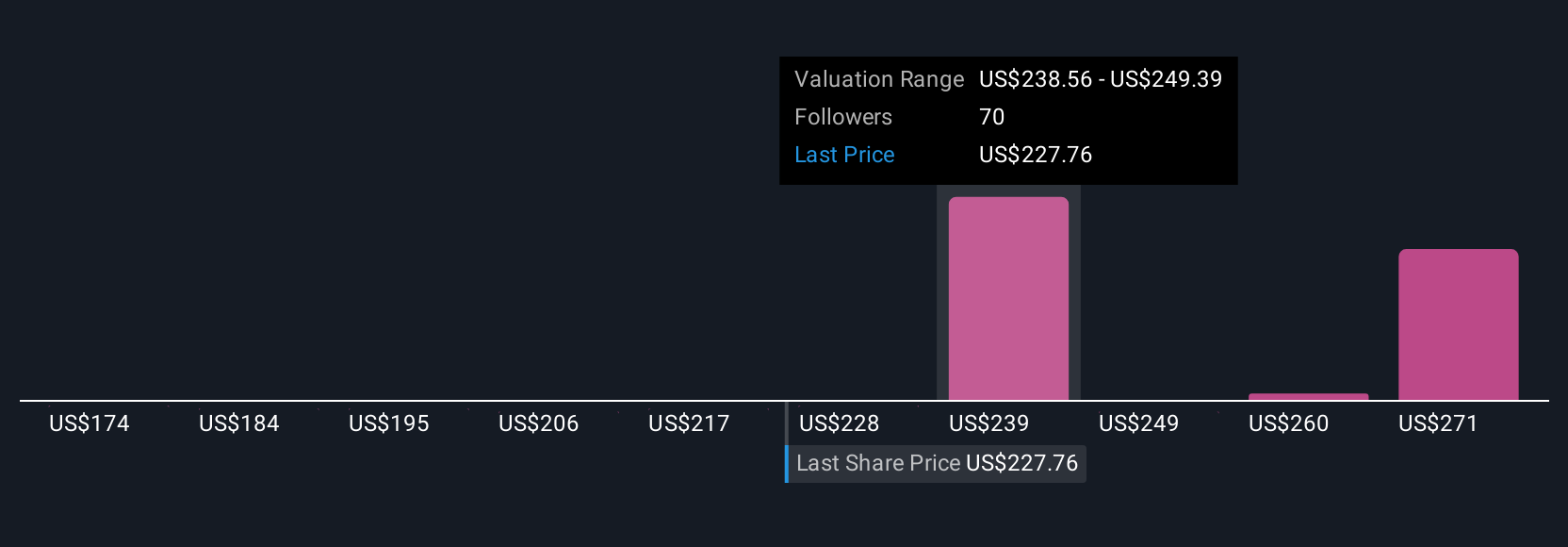

Five fair value estimates from the Simply Wall St Community range from US$226 to US$393 per share. While opinions differ, accelerating industry adoption of AI-powered automation may impact Paycom’s long-term profit margins and pricing power, so consider how your outlook aligns with these community viewpoints.

Explore 5 other fair value estimates on Paycom Software - why the stock might be worth just $226.28!

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

Early movers are already taking notice. See the stocks they're targeting before they've flown the coop:

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.