Please use a PC Browser to access Register-Tadawul

Get It

Why Elastic (ESTC) Is Up After Announcing $500M Buyback and New AI Cloud Inference Service

Elastic N.V. ESTC | 76.31 | -3.76% |

Uncover the next big thing with financially sound penny stocks that balance risk and reward.

To be an Elastic shareholder, you need to believe that the company’s continued investment in AI and cloud-powered solutions can drive sustained revenue growth and margin expansion, despite intense competition and the risk of product commoditization. The new US$500 million share repurchase and launch of Elastic Inference Service appear value-accretive but do not materially shift the near-term catalyst of driving adoption of integrated AI search and analytics, nor the biggest risk from hyperscaler competition.

The most relevant announcement is the release of the Elastic Inference Service, which enhances Elastic’s AI and generative search capabilities for cloud customers and reinforces the company’s core differentiation focus. By natively integrating GPU-accelerated inference into Elastic Cloud, this move further addresses enterprise demand for performance, scalability, and streamlined workflows, which ties directly into the company’s main growth catalysts.

However, on the other side, it’s important for investors to consider how direct cloud-native competitors might ...

Elastic's outlook projects $2.3 billion in revenue and $50.5 million in earnings by 2028. This assumes annual revenue growth of 13.9% and a $134 million increase in earnings from the current level of -$83.5 million.

Uncover how Elastic's forecasts yield a $120.16 fair value, a 48% upside to its current price.

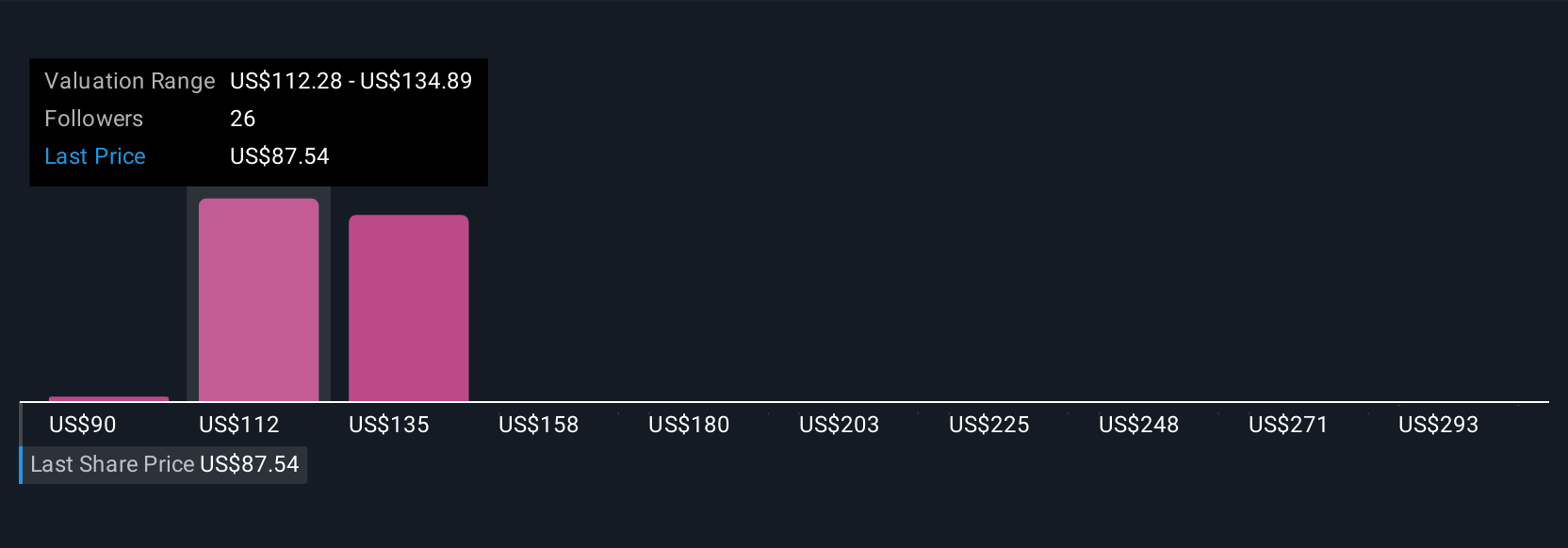

Seven Simply Wall St Community members estimate Elastic’s fair value between US$89.66 and US$315.80. While many see growth potential from AI-powered adoption, the competitive threat from hyperscalers remains an important factor influencing future performance and investor conviction.

Explore 7 other fair value estimates on Elastic - why the stock might be worth just $89.66!

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

Opportunities like this don't last. These are today's most promising picks. Check them out now:

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.