Please use a PC Browser to access Register-Tadawul

Get It

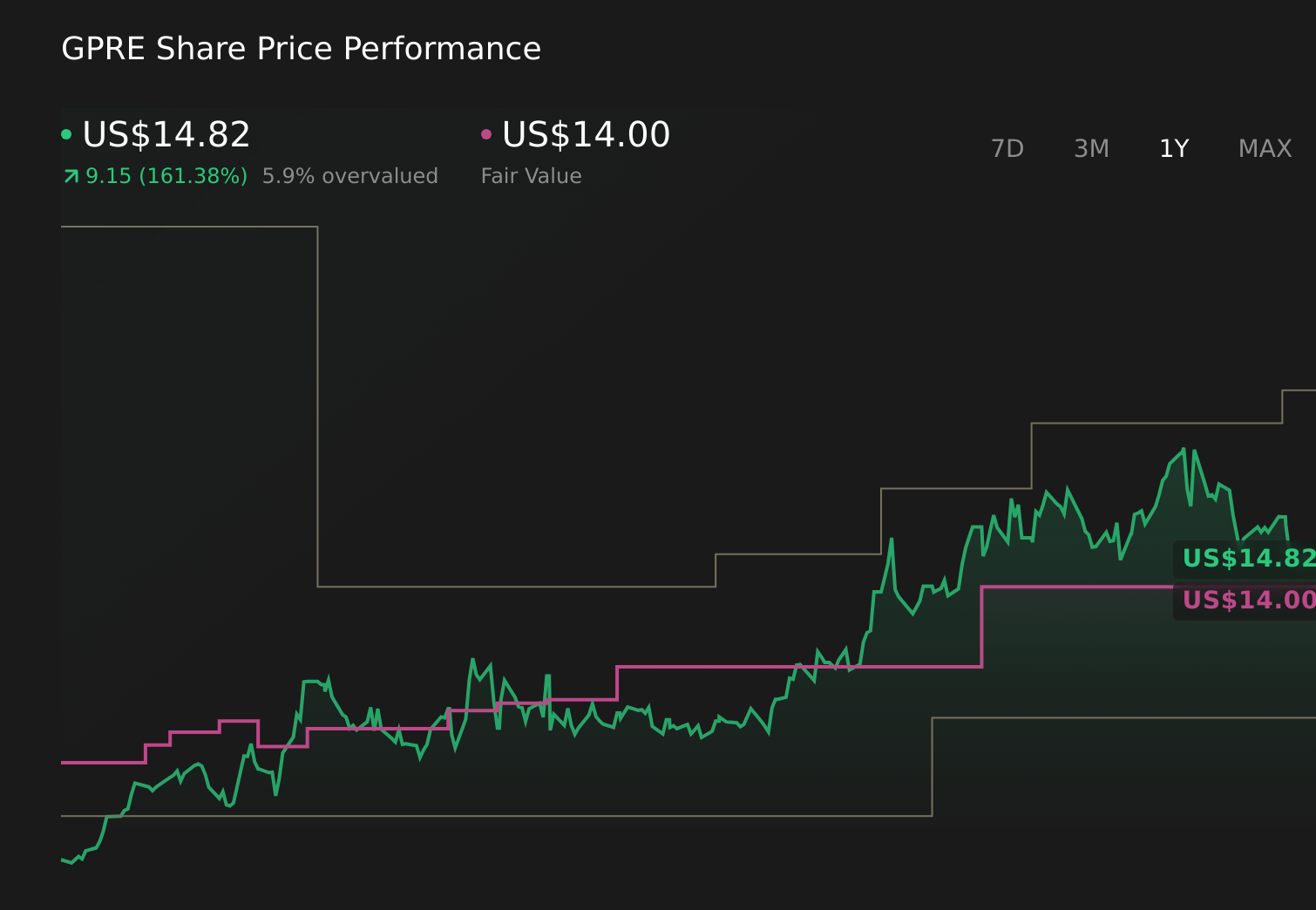

Why Green Plains (GPRE) Is Up 19.6% After Returning To Profit On Lower Sales - And What's Next

Green Plains Inc. GPRE | 14.02 | +3.32% |

This technology could replace computers: discover 23 stocks that are working to make quantum computing a reality.

To own Green Plains, you need to believe in its shift from a pure ethanol producer to a broader low-carbon platform that can eventually produce consistent profits from fuels, protein, and carbon credits. The return to quarterly profitability in Q4 2025, despite weaker volumes, supports the near term catalyst around cost control and operational execution. However, the full year loss and continued reliance on policy support keep regulatory and execution risk front and center for shareholders.

The most relevant recent announcement here is the Q4 and full year 2025 earnings release. It shows how Green Plains translated lower sales of US$428.85 million in the quarter into a positive net income of US$11.94 million, while the full year still ended with a net loss of US$121.28 million. This split result connects directly to the key catalyst of improving efficiency and the risk that the underlying business has not yet delivered consistent, company wide profitability.

Yet investors should pay close attention to how policy risk around carbon credits could affect Green Plains’ ability to sustain this improvement...

Green Plains’ narrative projects $3.4 billion revenue and $116.3 million earnings by 2028.

Uncover how Green Plains' forecasts yield a $11.56 fair value, a 22% downside to its current price.

Before this earnings surprise, the most optimistic analysts were assuming revenues of about US$3.4 billion and earnings of roughly US$116 million by 2028, which is far more optimistic than the baseline view and could be challenged if margin volatility and high debt, highlighted by recent losses, prove harder to overcome than they expected.

Explore 2 other fair value estimates on Green Plains - why the stock might be worth 22% less than the current price!

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

Don't miss your shot at the next 10-bagger. Our latest stock picks just dropped:

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.