Please use a PC Browser to access Register-Tadawul

Get It

Will Moelis (MC) Analyst Support Reinforce Its Standing in a Shifting Investment Banking Landscape?

Moelis & Co. Class A MC | 63.18 | +0.72% |

We've found 18 US stocks that are forecast to pay a dividend yield of over 6% next year. See the full list for free.

To own Moelis shares, an investor usually needs to be confident in the firm’s ability to grow its deal flow and earnings through specialized advisory services and expansion efforts, especially in areas like Private Capital Advisory. The recent reaffirmed 'Outperform' rating likely reinforces this narrative in the short term, but the lowered price target and ongoing volatility in transaction activity mean the most important catalyst, consistent growth in fee-generating mandates, remains unchanged, and key risks around expense pressure and earnings swings are not materially impacted by this news.

One recent development closely tied to catalysts is Moelis’s strong Q2 earnings, which showed a jump in net income to US$41.54 million from last year’s US$13.16 million. While this improvement is encouraging for margin and revenue momentum, the short-term focus still sits on whether such performance can be sustained through continued expansion and stable deal activity in a competitive sector.

By contrast, higher compensation costs tied to Moelis’s aggressive hiring and retention model remain a risk investors should be watching closely if...

Moelis is projected to reach $2.1 billion in revenue and $381.7 million in earnings by 2028. This outlook assumes a 15.3% annual revenue growth rate and reflects a $183.6 million increase in earnings from the current $198.1 million.

Uncover how Moelis' forecasts yield a $80.00 fair value, a 22% upside to its current price.

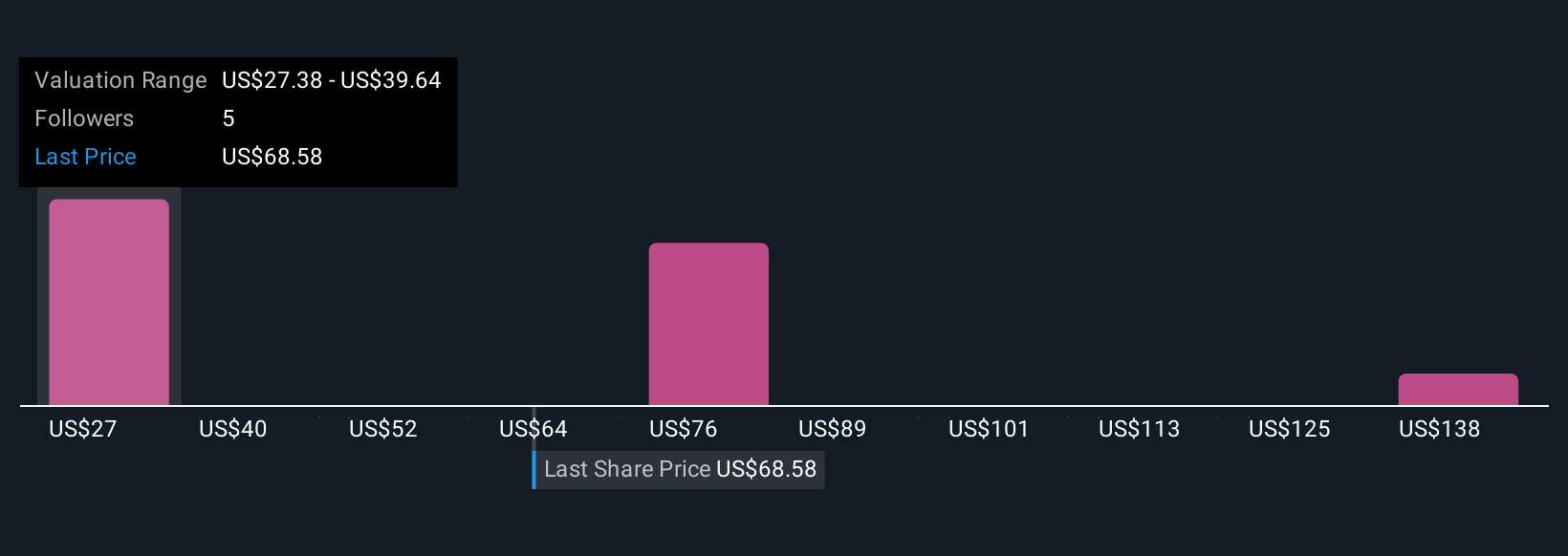

Three private investor estimates from the Simply Wall St Community put Moelis’s fair value between US$27.42 and US$150. In a marketplace where opinions widely differ, ongoing investments in talent and higher expenses could have broad implications for how you assess the company’s long-term performance.

Explore 3 other fair value estimates on Moelis - why the stock might be worth over 2x more than the current price!

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

Markets shift fast. These stocks won't stay hidden for long. Get the list while it matters:

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.