Please use a PC Browser to access Register-Tadawul

Get It

A Look At Canadian Solar (CSIQ) Valuation After Japan Storage Milestone And U.S. Expansion Plans

Canadian Solar Inc. CSIQ | 21.37 21.01 | +3.24% -1.68% Pre |

Canadian Solar (CSIQ) just switched on its first grid connected battery storage project in Japan, a 2 MW, 8.25 MWh system in Hokkaido that anchors a broader global storage push.

For you as a shareholder or potential investor, this Japan milestone sits alongside new U.S. focused financing plans and asset restructuring. All of these elements may influence how the market reassesses Canadian Solar’s growth profile and risk mix.

The Japan storage launch follows a guidance update pointing to lower 2025 profit, a planned US$350m private credit loan for U.S. expansion, and asset reshuffling around tax incentives. The share price is at US$19.90, representing a 97.62% 1 year total shareholder return, alongside weaker multi year returns and a 40.74% 3 month share price decline, suggesting short term momentum has cooled even as the stock has rebounded strongly over 12 months.

If this storage news has you thinking more broadly about the energy transition, it could be a good time to scan our 24 power grid technology and infrastructure stocks for other grid focused opportunities.

With the shares at US$19.90, only a small discount to the average analyst target and a modest intrinsic value gap, the question is whether recent weakness signals a mispriced storage story or if the market already sees future growth coming.

At $19.90, the most followed narrative pegs Canadian Solar’s fair value at about $23.33, implying upside that leans heavily on the storage and electrification story.

Canadian Solar is experiencing robust demand from the global acceleration of electrification (driven by booming data center, AI, and energy-intensive applications), which, combined with their expansion of energy storage solutions and solar module shipments, is likely to increase long-term revenue growth.

The company's forward integration into battery storage, with plans to expand BESS manufacturing capacity from 10 GWh to 24 GWh by 2026 and battery cell capacity from 3 GWh to 9 GWh, positions Canadian Solar to capture higher-margin business and increase average order value, positively impacting future net margins and earnings.

Want to see what sits behind that storage led upside case? The narrative leans on double digit top line expansion, rising profitability, and a future earnings multiple that is far from stretched. Curious how those moving parts combine to reach a fair value above today’s price?

Result: Fair Value of $23.33 (UNDERVALUED)

However, this upside story still leans heavily on policy support and trade conditions, as shifting U.S. incentives or new tariffs could quickly reset expectations.

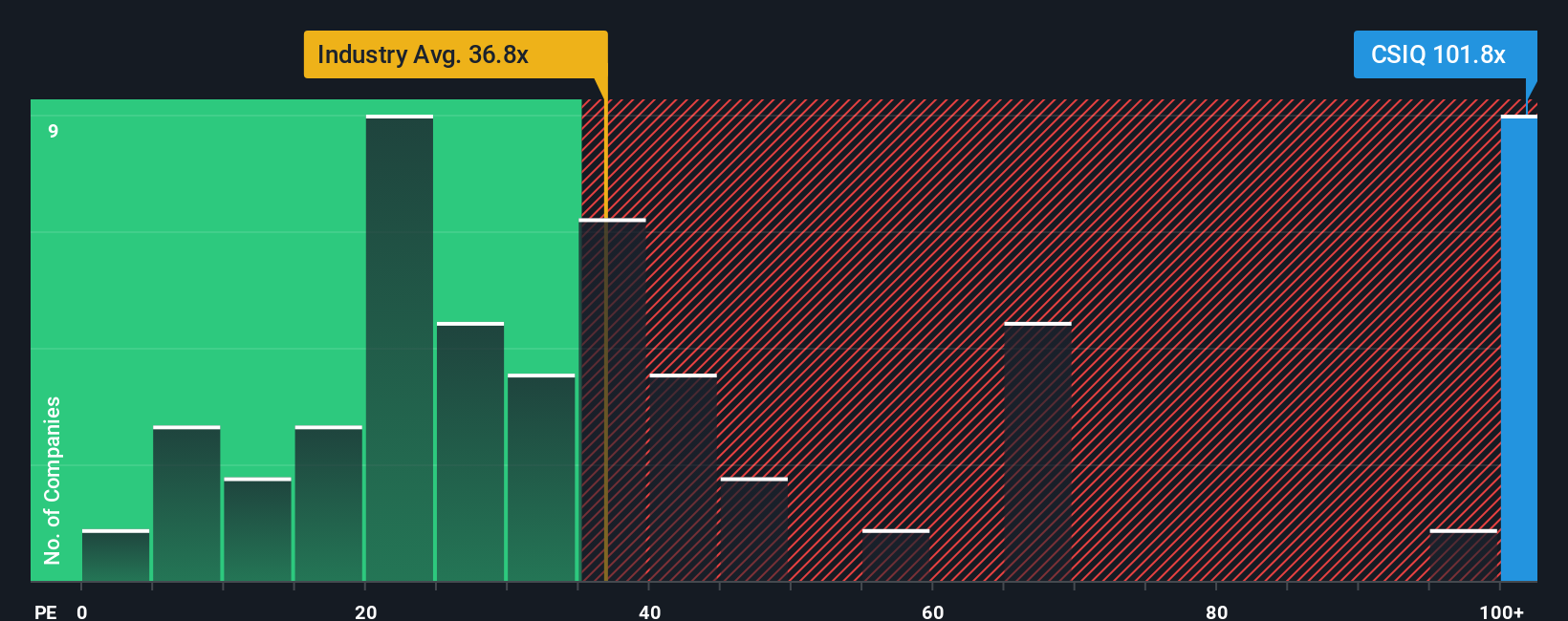

The fair value narrative suggests upside, but the P/E picture is less friendly. At 82.7x earnings, Canadian Solar trades richer than the US Semiconductor industry at 46.4x and above the peer average of 57.6x, even though its own fair ratio is 137.1x. That gap leaves you weighing more valuation risk or more opportunity.

Before you lean on P/E alone, it may help to see what the numbers imply in more detail so you can judge whether this premium feels justified or stretched. See what the numbers say about this price — find out in our valuation breakdown.

If you look at the numbers and reach a different conclusion, or simply prefer to test your own view, you can build a tailored thesis in just a few minutes, starting with Do it your way

A great starting point for your Canadian Solar research is our analysis highlighting 3 key rewards and 3 important warning signs that could impact your investment decision.

If you are weighing what to do next after looking at Canadian Solar, do not stop here, you could miss other ideas that fit your style and risk comfort.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.