Please use a PC Browser to access Register-Tadawul

Get It

A Look At Hagerty (HGTY) Valuation As New Marketing Leaders Target Membership Growth

Hagerty Inc Class A HGTY | 11.63 | +2.15% |

Hagerty (HGTY) has reshaped its marketing leadership, promoting Marc Burns to Chief Marketing Officer and naming Matt Teshera Senior Vice President of Marketing. Both leaders will focus on membership experience and integrated brand efforts.

For you as an investor, these appointments tie directly to how Hagerty aims to grow and retain its member base, which sits at the heart of its collector car insurance, membership and marketplace model.

Hagerty’s share price has eased recently, with a 7 day share price return of 4.29% and a 90 day share price return of 9.87%, even as 1 year total shareholder return sits at 19.88% and 3 year total shareholder return at 25.76%. This suggests that longer term holders have fared better than recent buyers.

If this marketing reshuffle has you thinking about where else leadership could drive growth, it might be a good time to broaden your scope and check out our 23 top founder-led companies.

So with Hagerty’s shares easing in recent months, trading at $12.06 with an implied 13% gap to analyst targets and an intrinsic value estimate slightly above today’s price, is this a genuine opening, or is the market already baking in future growth?

Hagerty’s most followed narrative points to a fair value of $13.67, compared with the last close at $12.06, so you are looking at a modest valuation gap built on a detailed long term earnings path.

The ramping State Farm partnership is expected to significantly accelerate new business growth, providing access to over 500,000 current program vehicles and thousands of motivated agents, materially expanding Hagerty's customer acquisition funnel and recurring commission revenues at attractive margins over the next several years.

Read the complete narrative. Read the complete narrative.

Want to see what is baked into that $13.67 figure? Revenue climbing steadily, margins stepping up sharply, and a future earnings multiple that needs to compress meaningfully. Curious how those pieces fit together into one fair value number? The full narrative lays out the exact path.

Result: Fair Value of $13.67 (UNDERVALUED)

However, you also need to weigh the risk that younger drivers stay less interested in classic cars, and that taking on 100% of underwriting risk magnifies any loss shocks.

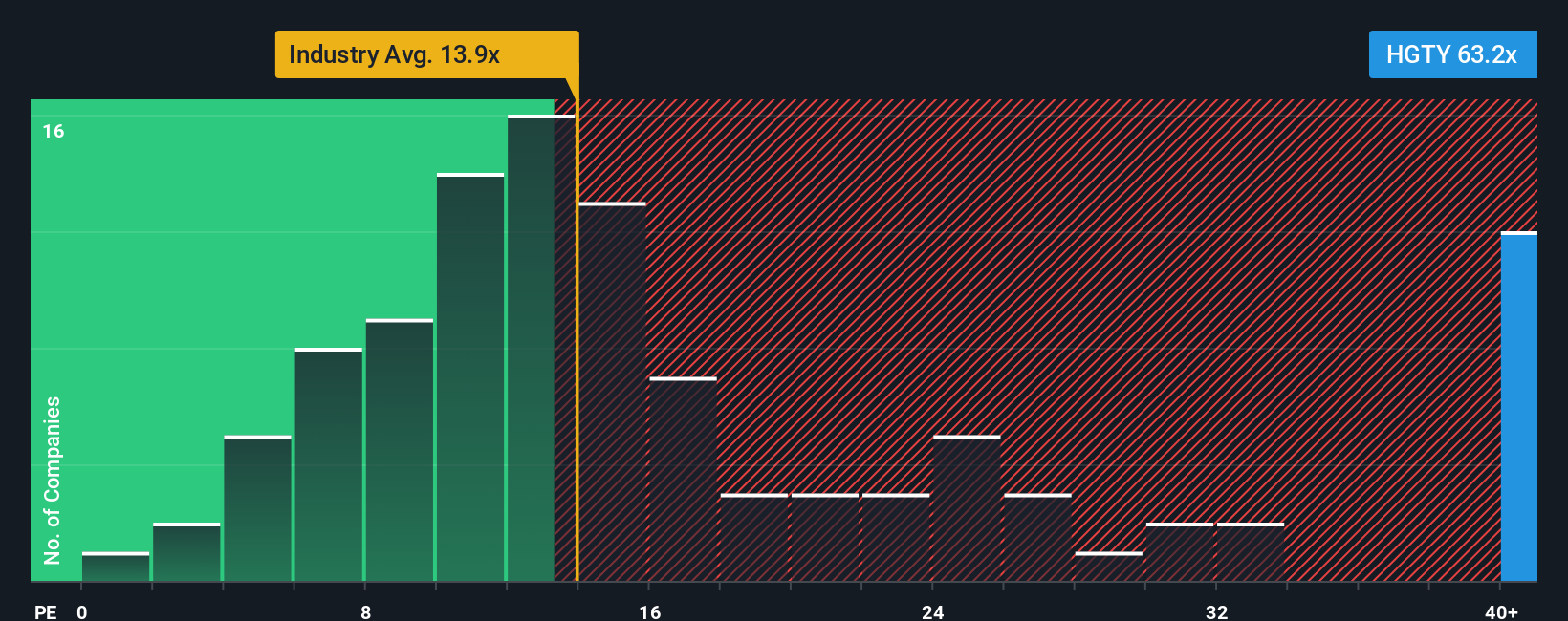

That 11.8% “undervalued” label sits awkwardly next to where the market is actually pricing Hagerty today. On a P/E of 36.4x, the shares trade above the US Insurance industry at 12.3x, the peer average at 31.9x, and the 28.1x fair ratio our model suggests the market could move toward over time.

For you, that gap points to less of a clear mispricing and more of a higher expectations setup, where even small disappointments could matter just as much as positive surprises. How comfortable are you paying well above the fair ratio and sector norms for this story?

If you see the numbers differently, or want to stress test your own assumptions against the data, you can build a personalized Hagerty thesis in just a few minutes, starting with Do it your way.

A good starting point is our analysis highlighting 2 key rewards investors are optimistic about regarding Hagerty.

If Hagerty has sharpened your thinking, do not stop here. Use the Simply Wall St Screener to line up fresh ideas that match your approach.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.