Please use a PC Browser to access Register-Tadawul

Get It

Assessing Abbott Laboratories (ABT) Valuation After Q4 Nutrition Weakness And Ongoing Device Strength

Abbott Laboratories ABT | 108.49 | +0.32% |

Abbott Laboratories (ABT) is back in focus after its fourth quarter update, where weakness in the Nutrition segment pulled overall sales growth below Wall Street expectations and prompted CEO Robert Ford to begin reshaping that business.

The recent Q4 earnings miss and softer Nutrition outlook have weighed on sentiment, with a 30 day share price return of an 11.99% decline and a 1 year total shareholder return of a 12.96% decline. The modest 3 year total shareholder return of 3.70% suggests only limited long term gains so far, despite the latest 1 day and 7 day share price rebounds.

If this update has you rethinking your healthcare exposure, it could be a good moment to see what else is out there through healthcare stocks.

With Abbott now trading below its recent levels and sitting at a discount to some analyst targets, the key question for you is whether current issues are already reflected in the price or whether the market is still attributing value to potential future growth.

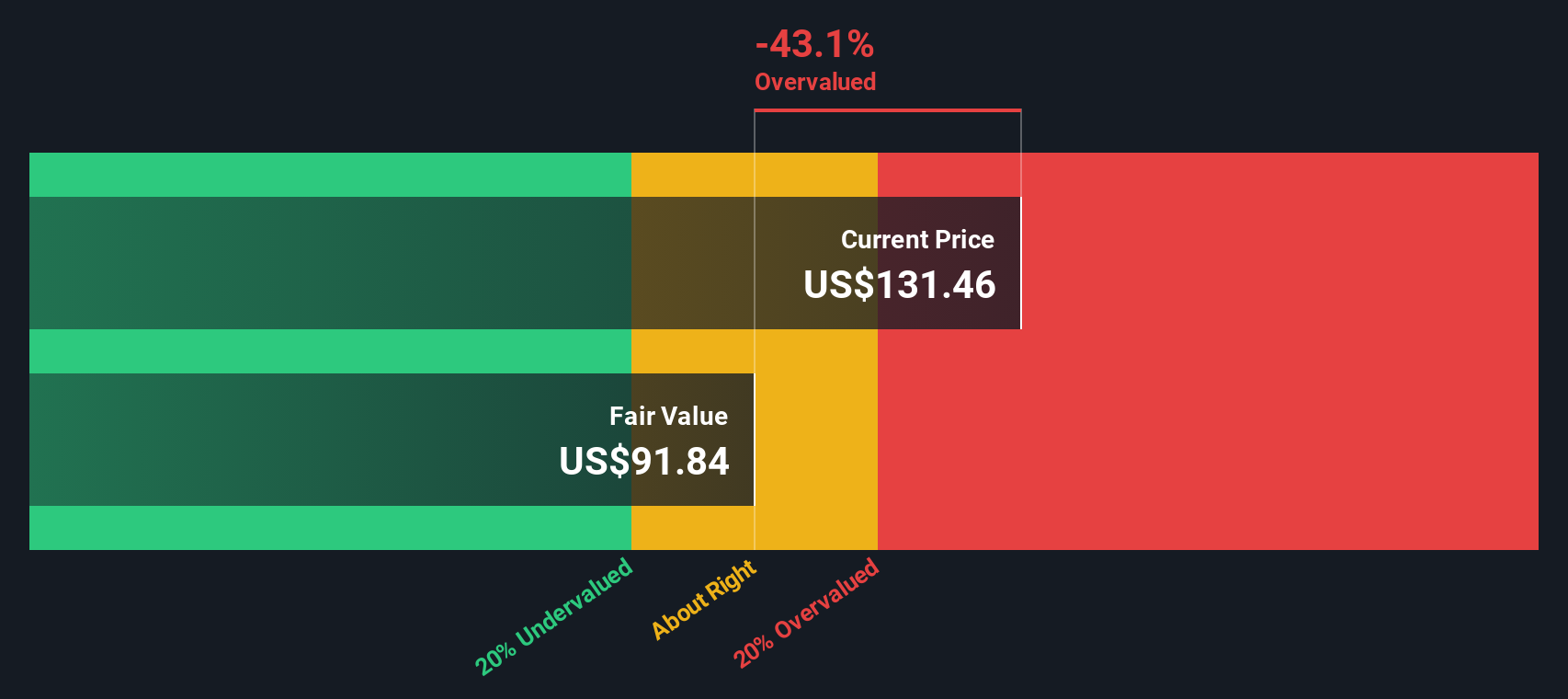

With Abbott Laboratories closing at $109.30 against a most-followed fair value estimate of $136.47, the valuation debate is centered on how durable its earnings mix can be.

Abbott's ongoing innovation in high-margin segments, most notably through the FreeStyle Libre franchise (with next-gen, dual-analyte sensors and new software integrations) and pipeline launches in structural heart and rhythm management devices, positions the company to capture incremental market share and drive net margin expansion.

Curious what earnings profile sits behind that value gap? The narrative leans on steady revenue compounding, a reset margin path, and a richer earnings multiple that is far from conservative.

Result: Fair Value of $136.47 (UNDERVALUED)

However, you still need to weigh risks such as pricing pressure in diagnostics and potential integration challenges around the pending Exact Sciences deal, which could unsettle the earnings story.

There is a twist when you compare the narrative fair value of $136.47 with our DCF result. On our numbers, Abbott is pricing above an estimated future cash flow value of $93.49, which points to an overvalued signal. So which story do you trust more: earnings power or cash flows?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Abbott Laboratories for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 875 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

If the story here does not quite match your view, or you would rather work from the raw numbers yourself, you can build a fresh narrative in just a few minutes, starting with Do it your way.

A great starting point for your Abbott Laboratories research is our analysis highlighting 5 key rewards and 1 important warning sign that could impact your investment decision.

If Abbott is only one piece of your portfolio puzzle, you can broaden your watchlist today with targeted stock ideas built from clear data and consistent criteria.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.