Please use a PC Browser to access Register-Tadawul

Get It

Assessing Alphabet (NasdaqGS:GOOGL) Valuation As Gemini 3 And AI Momentum Shape Expectations For Q4 Results

Alphabet Inc. Class A GOOGL | 303.13 | -0.15% |

Recent optimism around Alphabet (GOOGL) has centered on Gemini 3, rising demand for its Tensor Processing Units, and solid Google Cloud momentum, all ahead of the company’s upcoming fourth quarter earnings release.

Alphabet’s recent story sits on top of a strong run, with a 30 day share price return of 7.25% and a 90 day gain of 19.13%, while the 1 year total shareholder return of 66.32% and 3 year total shareholder return of about 3.3x reflect how sentiment around its AI push, Gemini 3 rollout and Google Cloud progress has built over time despite occasional regulatory and autonomous driving headlines.

If Gemini 3 and Alphabet’s AI build out have your attention, it could be a good moment to broaden your view with other high growth tech and AI stocks that are also riding the AI infrastructure wave.

After a 66% 1 year total return and a recent 30 day gain of 7.25%, Alphabet is priced for high expectations. With AI optimism at full volume, investors may ask whether there is still a realistic entry point here or whether future growth is already reflected in the current price tag.

At a last close of $338, the narrative pins Alphabet’s fair value at about $340, which frames the current price as well below its long term potential.

Alphabet is a compounding machine hiding under an ad empire. With AI monetization finally catching fire, Cloud turning profitable, and more YouTube monetization coming, this isn’t just a “big tech stock”, it’s an innovation platform priced like a mature business. You get high margin growth, significant cash flow, a strong balance sheet, and exposure to everything from AI to driverless cars. It offers technology diversification inside a single ticker.

Curious what sits behind that upgrade from “mature business” to cash compounding platform, according to oscargarcia? The narrative leans on robust margins, steady growth, and a richer future earnings multiple to justify that gap. The numbers behind those assumptions may surprise you.

Result: Fair Value of $340 (UNDERVALUED)

However, this upbeat story can crack if regulatory pressure bites harder than expected, or if AI tools meaningfully erode the profitability of Google’s core search and ads engine.

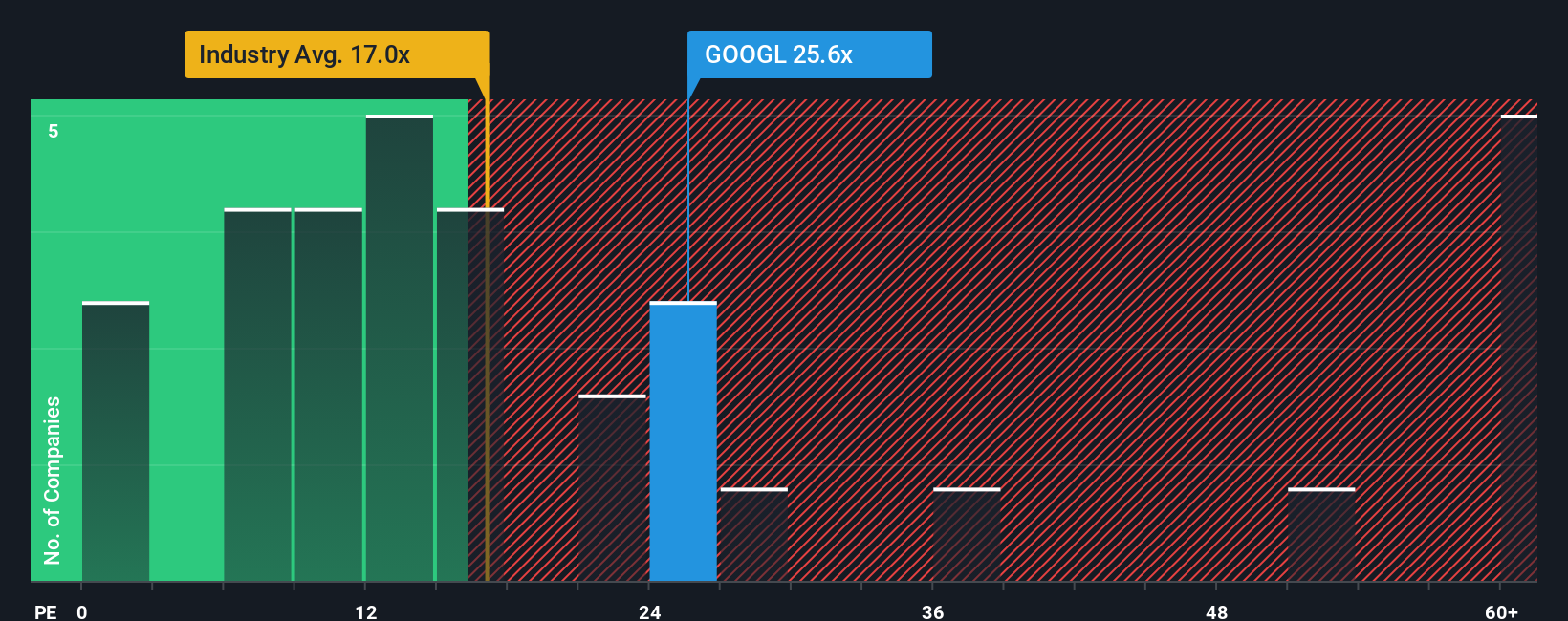

That $340 fair value narrative meets a different story when you look at today’s earnings. At a P/E of 32.8x, Alphabet trades at more than double the US Interactive Media and Services average of 15.5x, although below peers at 44.7x and under a fair ratio of 41.3x.

This combination of premium pricing, relative discount to peers, and gap to the fair ratio suggests both valuation risk and potential upside if sentiment shifts. The open question for you is whether that current P/E already reflects enough of Alphabet’s AI and Cloud ambitions.

If you see the data pointing in a different direction, or simply want to stress test these assumptions yourself, you can build your own view in a few minutes using Do it your way.

A good starting point is our analysis highlighting 2 key rewards investors are optimistic about regarding Alphabet.

If Alphabet is already on your radar, it makes sense to scan a few more angles so you are not missing opportunities hiding in plain sight.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.