Please use a PC Browser to access Register-Tadawul

Get It

Assessing NGL Energy Partners (NGL) Valuation After Revenue Beat And Positive Market Reaction

NGL Energy Partners LP NGL | 12.42 12.40 | +3.50% -0.16% Pre |

NGL Energy Partners (NGL) has drawn fresh attention after surpassing revenue forecasts while reporting earnings per share below expectations. This mix coincided with a positive share price reaction and renewed interest in its midstream operations.

That strong revenue print and the recent 52 week high have come alongside a 90 day share price return of 78.28% and a 1 year total shareholder return of 108.59%, so recent momentum is building on already very strong multi year gains.

If NGL’s move has you thinking about what else is gaining attention in energy infrastructure, it could be a good time to look at fast growing stocks with high insider ownership as another source of ideas.

With NGL Energy Partners now trading near its 52 week high after very strong recent returns, the key question is whether that intrinsic discount hints at mispricing or if the market is already baking in future growth.

On the numbers, NGL Energy Partners' current valuation looks modest, with a P/S of 0.4x that sits well below both industry and peer averages.

The P/S ratio compares the company’s market value to its revenue, which can be useful for businesses that are not currently profitable. For NGL, this lens helps frame a picture where the market is placing a relatively low value on each dollar of sales, even though earnings have been improving over several years. The partnership is still reporting a loss of $51.848 million on revenue of $3,250.313 million.

Against the wider US Oil and Gas industry average P/S of 1.5x and a peer group average of 1.9x, NGL’s 0.4x figure is far lower. This suggests the market is pricing in weaker prospects or higher risk than for many peers. However, compared with the SWS fair P/S ratio estimate of 0.4x, the current market multiple sits right on that level. This could indicate less room for a straightforward re-rating toward that fair ratio.

Result: Price-to-Sales of 0.4x (UNDERVALUED)

However, you still have to weigh risks such as the recent 25.35% annual revenue decline and the fact that NGL is loss making despite strong unit price momentum.

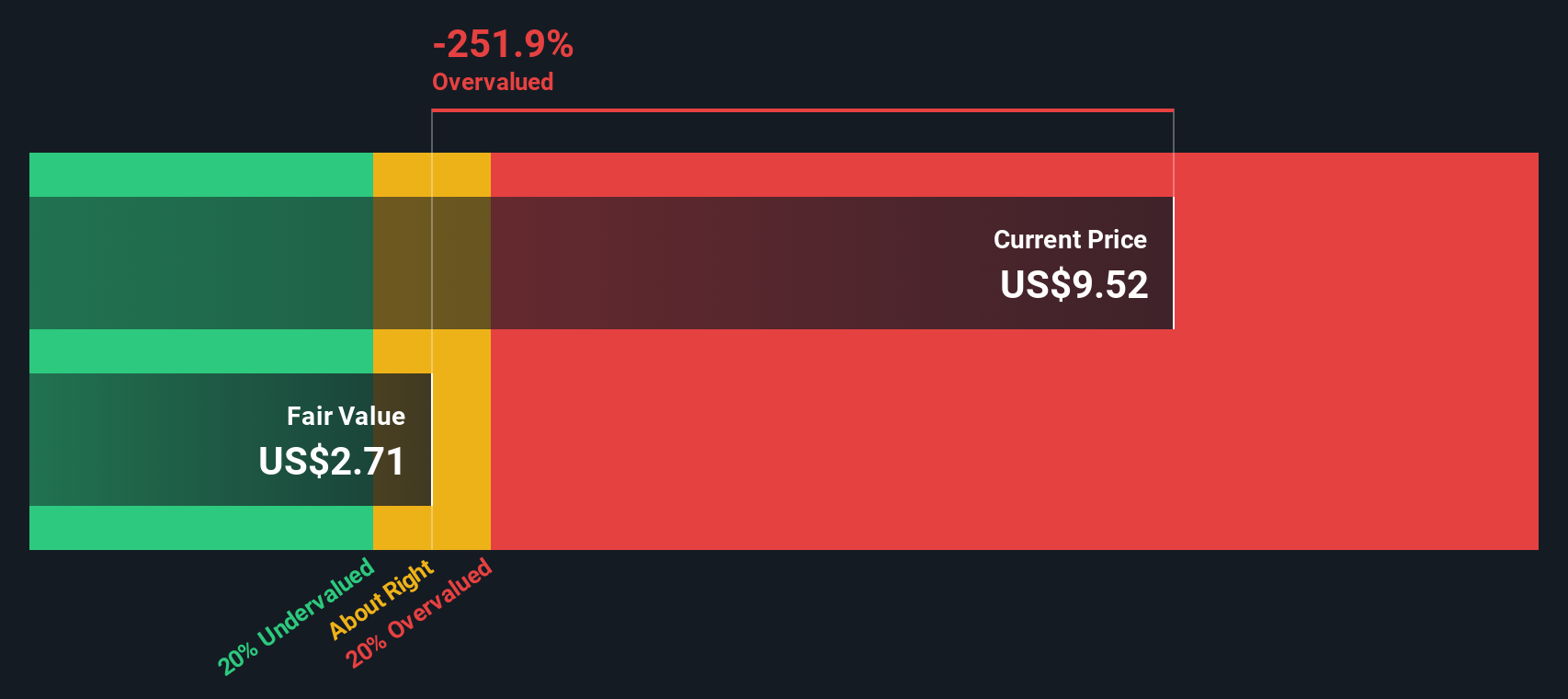

While the low 0.4x P/S suggests NGL Energy Partners is cheap on sales, our DCF model adds a different angle. On that framework, the units trading at $11.41 sit below an estimated future cash flow value of $16, which points to an undervalued picture based on cash generation rather than revenue alone. The question is which yardstick you trust more when a business is still loss making today.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out NGL Energy Partners for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 879 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

If you look at the numbers and reach a different conclusion, or just prefer to test your own view against the data, you can build a full narrative in a few minutes using Do it your way.

A good starting point is our analysis highlighting 3 key rewards investors are optimistic about regarding NGL Energy Partners.

If you stop with just one stock today, you could miss other opportunities that match your style, so let the data surface a few strong candidates for you.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.