Please use a PC Browser to access Register-Tadawul

Get It

Assessing Protagonist Therapeutics (PTGX) Valuation After Rusfertide NDA Filing And Rising Analyst Optimism

Protagonist Therapeutics, Inc. PTGX | 82.76 | -0.40% |

Protagonist Therapeutics (PTGX) is back in focus after filing a New Drug Application for rusfertide in polycythemia vera with partner Takeda, alongside fresh analyst enthusiasm and insider share sales for tax purposes.

The stock’s recent 3.06% 1 day and 9.90% 90 day share price returns, alongside a very large 1 year total shareholder return of about 2.3x, suggest momentum building around the rusfertide filing and broader clinical story, despite a modest 1 month share price pullback.

If this kind of biotech catalyst has your attention, it could be a good moment to scan other healthcare stocks that might be setting up for their own clinical or regulatory turning points.

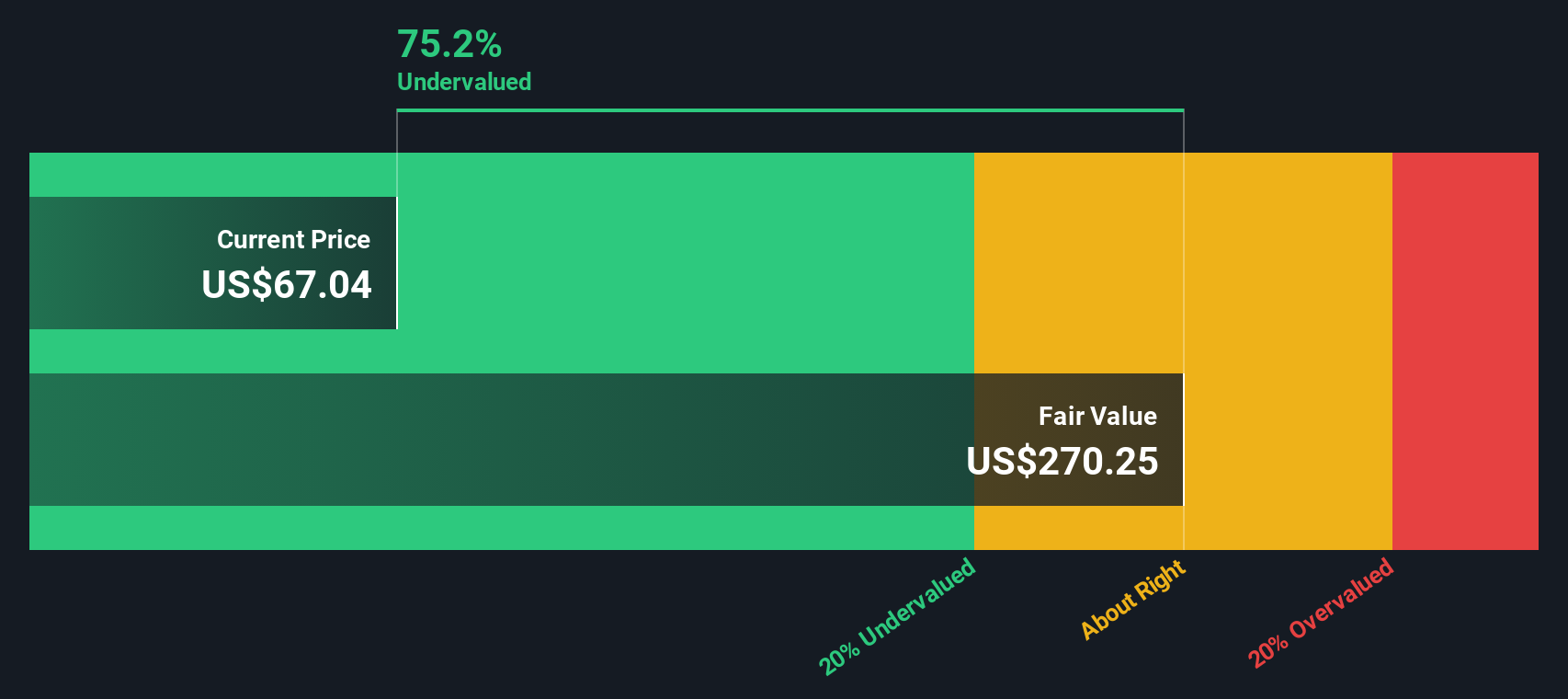

With PTGX trading at US$85.59 against an average analyst target around US$101 and an internal intrinsic value estimate implying a sizable discount, you have to ask: is this a genuine opportunity, or is the market already pricing in future growth?

On a P/E of 116.6x, Protagonist Therapeutics looks priced well above typical biotech valuations, especially with the last close at $85.59 and strong recent share price returns in the rearview.

The P/E ratio compares what investors are paying for each dollar of current earnings. For a clinical-stage focused biotech like PTGX, a high P/E often reflects expectations for future revenue and profit expansion around its pipeline rather than current profitability alone.

Here, the market is assigning a P/E multiple of 116.6x, while the peer average in US biotechs sits at 25.8x and the estimated fair P/E from the SWS model is 33.9x. That is a sharp premium to both peers and the level the fair ratio model suggests the multiple could move toward if sentiment or expectations reset around earnings power.

Result: Price-to-Earnings of 116.6x (OVERVALUED)

However, that rich P/E and heavy reliance on rusfertide and icotrokinra progress mean any clinical, regulatory or partnership setback could quickly challenge the current optimism.

While the 116.6x P/E makes PTGX look expensive, our DCF model tells a very different story. On that measure, the shares at $85.59 sit about 74.3% below an estimated future cash flow value of $332.81, which highlights a potential difference between earnings based and cash flow based views.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Protagonist Therapeutics for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 872 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

If you see the numbers differently or want to stress test your own view, it only takes a few minutes to build and refine a personalised thesis, then Do it your way.

A great starting point for your Protagonist Therapeutics research is our analysis highlighting 2 key rewards and 2 important warning signs that could impact your investment decision.

If you only stop at one company, you could miss some of the most interesting setups on the market, so use this as a springboard to widen your watchlist.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.