Please use a PC Browser to access Register-Tadawul

Get It

BlackSky Technology (BKSY): Valuation in Focus After $30M Defense Contract Win

BlackSky Technology Inc Class A BKSY | 25.52 | +2.28% |

BlackSky Technology (BKSY) just landed a multi-year contract worth over $30 million to deliver its Gen-3 tactical ISR services to a strategic international defense customer. This move highlights the company’s growing position in the defense intelligence market.

BlackSky’s shares have been volatile, with the recent $30 million contract announcement offering a bright spot amid pressure from slowing revenue growth and widening losses reported last week. After a strong year-to-date share price return of 27.41%, momentum has reversed lately, highlighted by a sharp 54.34% drop in the past month. Long-term total shareholder return sits higher at 55.66% over the last year.

If contract wins and shifting momentum have you rethinking your watchlist, now is a great opportunity to spot fresh defense and aerospace names with See the full list for free.

This recent contract has reignited debate around BlackSky’s potential valuation. Is the stock now set for a turnaround with further upside on offer, or could the market already be factoring in its future growth prospects?

Compared to the last close at $13.62, the most widely followed narrative puts BlackSky Technology's fair value at a much higher $27.29 per share. The spread between market price and narrative estimate turns heads, especially as fresh contract news circulates.

The ramp-up of the Gen-3 satellite constellation, coupled with demonstrated high performance and lower costs, is creating strong demand and contract expansion (especially once general availability launches in Q4). This is likely to drive a step-function increase in recurring imagery and analytics revenues in 2025 and beyond.

Is this pricing justified by BlackSky’s ambitious revenue projections, climbing margins, and bold plans for recurring sales growth? There is more behind this fair value than meets the eye. Find out which head-turning assumptions power such a high price target before everyone else does.

Result: Fair Value of $27.29 (UNDERVALUED)

However, persistent revenue volatility and growing dependence on international contracts could quickly undermine the optimistic outlook that is driving current valuations.

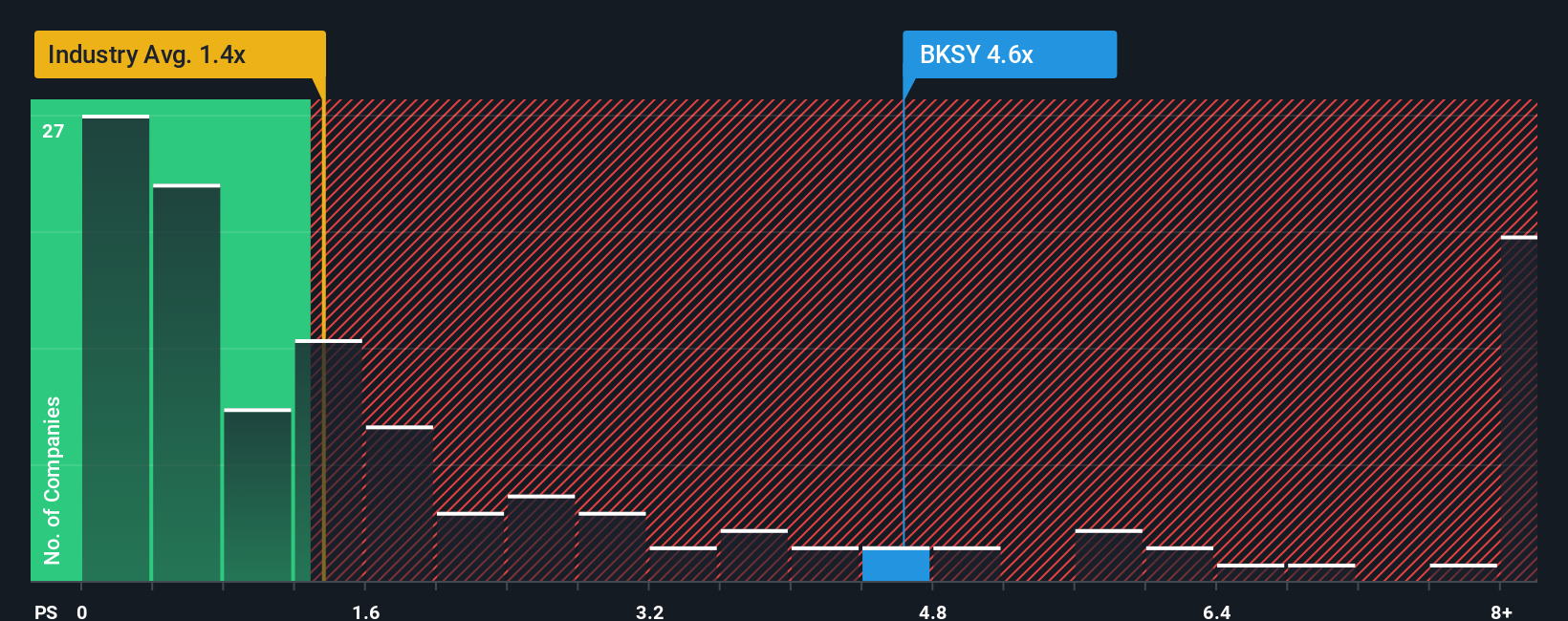

Looking beyond fair value narratives, the market puts a premium on BlackSky Technology's revenue, trading at a Price-to-Sales ratio of 4.8x. This is well above the US Professional Services industry average of 1.4x, the peer average of 1.7x, and the fair ratio of 3.2x. When a company trades far above these benchmarks, it often signals investor excitement about growth potential. However, it also creates valuation risk if expectations are not met. Will BlackSky's fundamentals justify these elevated multiples, or could sentiment shift quickly?

Not convinced by the consensus or eager to dive into the numbers firsthand? You can piece together your own perspective in minutes: Do it your way

A great starting point for your BlackSky Technology research is our analysis highlighting 2 key rewards and 4 important warning signs that could impact your investment decision.

Don’t let great opportunities pass you by. Make your next smart move by checking out standout stocks in booming sectors using Simply Wall Street’s powerful screener.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.