Please use a PC Browser to access Register-Tadawul

Get It

CRH (NYSE:CRH) Valuation in Focus Following Major Buyback and Rising Infrastructure Demand

CRH Plc Sponsored ADR CRH | 126.40 126.86 | -0.46% +0.36% Pre |

CRH (NYSE:CRH) recently announced a sizable share buyback program, signaling confidence in its balance sheet and a commitment to shareholder value. This move comes as the company benefits from strong infrastructure demand and positive sector trends.

Beyond the buyback, CRH has attracted fresh optimism thanks to rising infrastructure demand, its $2.1 billion Eco Material acquisition in North America, and ongoing capital investments linked to the AI-powered data center boom. Recent moves, like the appointment of Patrick Decker to the board, reinforce a sense of momentum. Momentum is clearly building: CRH’s 90-day share price return sits at 22.3%, and its one-year total shareholder return is 27.9%, a level that speaks to how investors are rewarding both earnings growth and capital efficiency.

If you want to keep up this discovery streak, consider exploring fast growing stocks with high insider ownership for other fast-moving opportunities catching investors’ attention right now.

With these robust gains and bullish forecasts in mind, investors might wonder if CRH is still undervalued at current levels or if the market has already priced in its next wave of growth.

With CRH trading at $116.03 and the most closely followed narrative estimating its fair value at $129.86, the stock is trading well below what analysts consider justified. This creates a compelling outlook, especially when taking into account recent margin improvements and sector momentum.

Strategic reinvestment into production automation, operational efficiencies, and capacity expansions at key aggregate and cement facilities is enabling CRH to achieve consecutive margin expansion (Q2 margins up 70bps YoY), increasing overall profitability and underpinning robust earnings growth.

Want to know what’s fueling this bullish valuation? There is a surprising blend of steady growth projections and a future profit multiple more commonly found in high-growth industries. Discover which numbers and assumptions are quietly driving this premium fair value estimate and see what might really power CRH’s next chapter.

Result: Fair Value of $129.86 (UNDERVALUED)

However, shifts in U.S. infrastructure funding or integration risks from recent acquisitions could quickly change the outlook for CRH’s growth story.

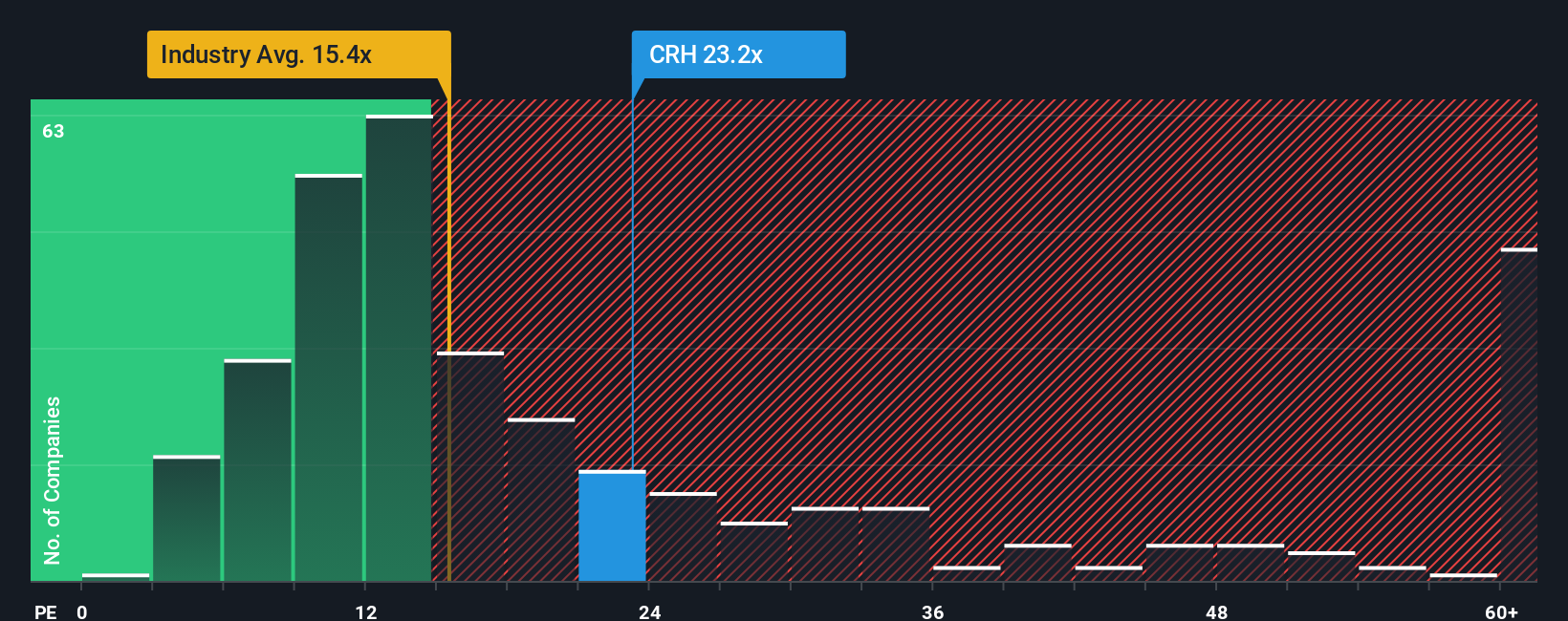

While our fair value estimate indicates CRH is undervalued, the stock actually trades at a price-to-earnings ratio of 23.8x, which is high compared to the global industry average of 15.6x and even above most peers. Its fair ratio is closer to 26.8x, which implies investors are paying up for its future prospects but not betting on irrational exuberance either. Does this premium mean further gains, or could lofty expectations add extra risk?

If you see the story differently or want to dive deeper on your own, you can build a custom narrative in just a few minutes. Do it your way.

A great starting point for your CRH research is our analysis highlighting 2 key rewards and 2 important warning signs that could impact your investment decision.

Smart investors never settle for just one opportunity. Take your strategy to the next level with these hand-picked avenues and stay a step ahead of the market’s next move.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.