Please use a PC Browser to access Register-Tadawul

Get It

Freeport-McMoRan (FCX) Margin Improvement Challenges Premium Valuation Narrative

Freeport-McMoRan, Inc. FCX | 47.38 48.31 | -1.52% +1.96% Pre |

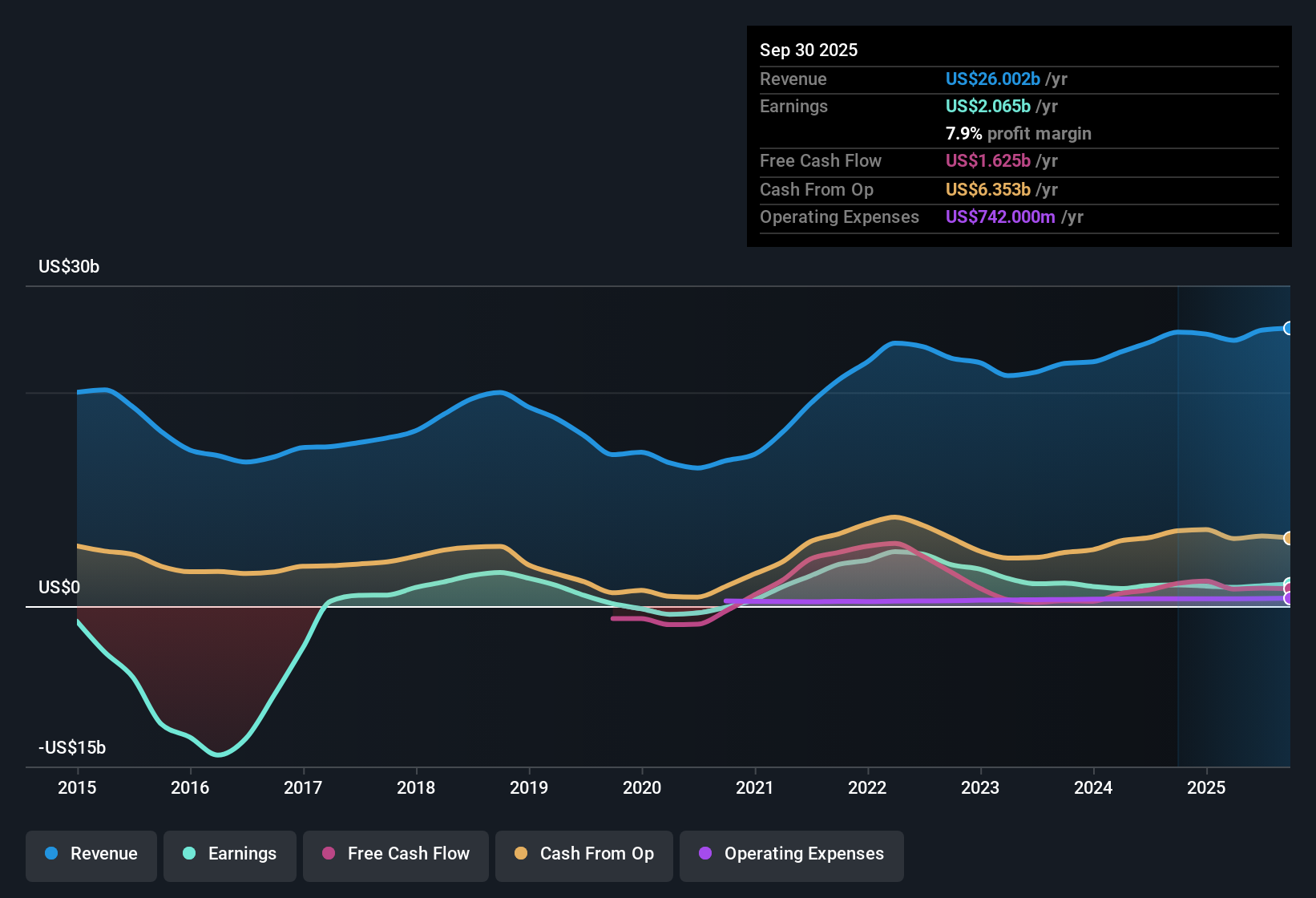

Freeport-McMoRan (FCX) reported earnings forecasted to grow at 22.24% per year, with revenue projected to increase annually at 6.6%, trailing the broader US market’s 10% growth rate. Net profit margins reached 7.9%, a slight improvement from last year’s 7.8%, and the company delivered a modest year-over-year earnings growth of 3.8%, outperforming its five-year average decline of -5.1% per year. These results, combined with a lack of identified risks and a perception of undervaluation based on discounted cash flow measures, set the stage for investor optimism even as the stock trades at a premium relative to industry peers.

See our full analysis for Freeport-McMoRan.The next step is to see how these headline numbers compare with the prevailing narratives investors follow most closely. Some expectations will hold up, while others may get a fresh perspective.

Consensus analysts believe further margin upside is possible as catalysts like the Indonesian smelter and US innovation scale up. The question remains whether this will be enough to keep Freeport’s earnings growth ahead of peers. 📊 Read the full Freeport-McMoRan Consensus Narrative.

To see how these results tie into long-term growth, risks, and valuation, check out the full range of community narratives for Freeport-McMoRan on Simply Wall St. Add the company to your watchlist or portfolio so you'll be alerted when the story evolves.

Have a unique take on the numbers? Share your insights and build a narrative in just a few minutes: Do it your way

A good starting point is our analysis highlighting 3 key rewards investors are optimistic about regarding Freeport-McMoRan.

Despite strong margin progress, Freeport-McMoRan’s premium valuation and dependence on catalysts raise concerns about consistent value compared to industry peers.

If you’re looking for companies where the price better matches earnings potential, filter your search using our these 870 undervalued stocks based on cash flows and uncover stocks offering greater upside for the risk taken.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.