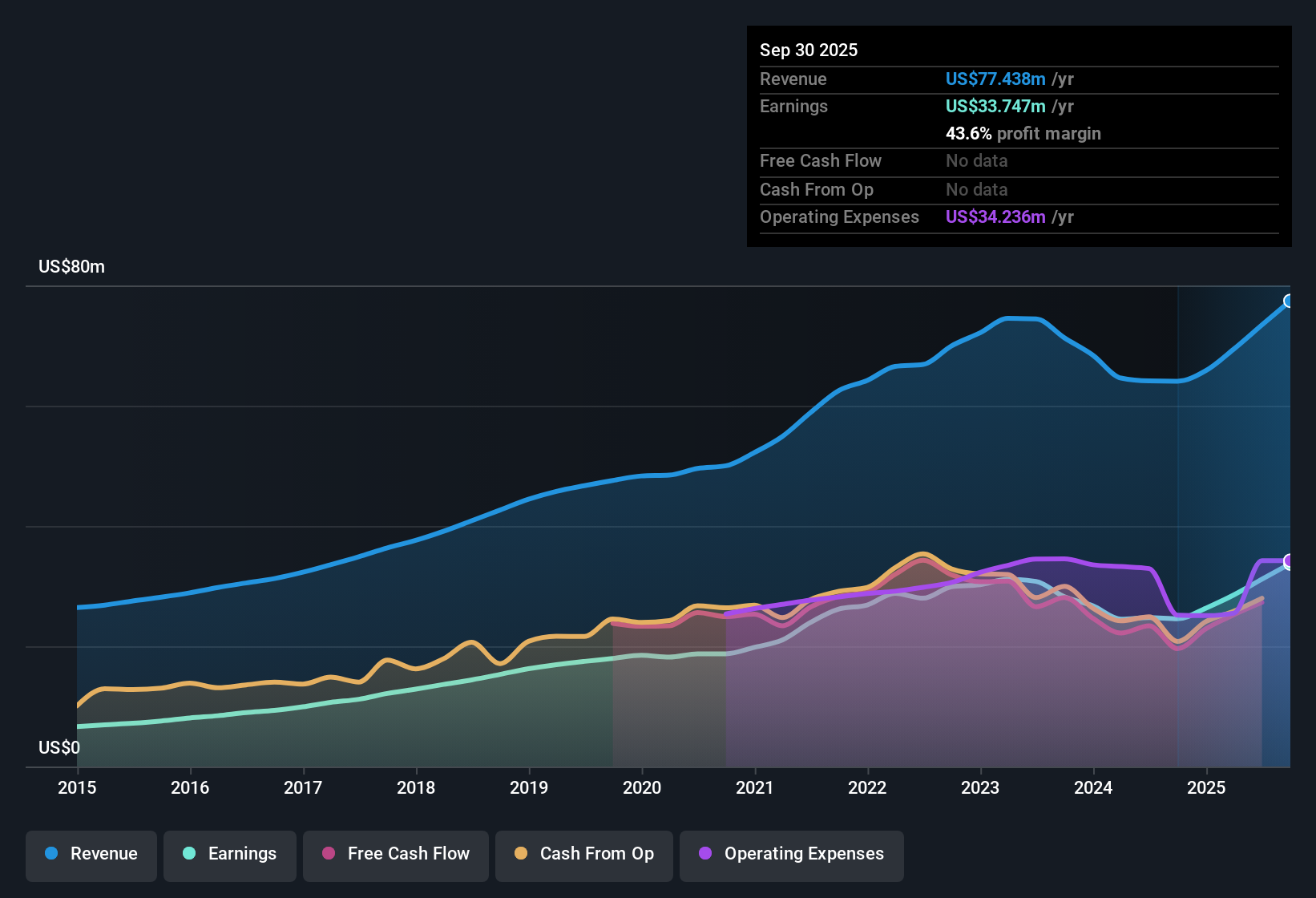

Greene County Bancorp (GCBC) opened Q2 2026 with total revenue of US$22.0 million and basic EPS of US$0.60, while trailing twelve month figures show revenue of US$82.0 million and EPS of US$2.15, alongside earnings growth of 37.4% over the last year. Over recent quarters, the company has seen revenue move from US$17.5 million and EPS of US$0.44 in Q2 2025 to US$22.0 million and EPS of US$0.60 in Q2 2026. The trailing net profit margin stands at 43.6% versus 38.3% last year, setting up an earnings story that centers on how sustainably the bank is converting revenue into profits.

See our full analysis for Greene County Bancorp.

With the recent figures on the table, the next step is to see how these margins and earnings trends line up with the prevailing narratives around Greene County Bancorp and where the numbers might challenge those views.

NasdaqCM:GCBC Earnings & Revenue History as at Jan 2026

Net Income Nears US$10.3 Million This Period

Q2 2026 net income excluding extra items was US$10.3 million, compared with US$7.5 million in Q2 2025 and US$8.1 million in Q3 2025, while trailing twelve month net income reached US$36.5 million.

What stands out for a bullish view is that reported earnings growth of 37.4% over the last year and trailing net income of US$36.5 million sit well above the five year average growth rate of 4.4%. This supports the idea of a stronger profit run than the longer term trend, even as investors consider how that compares to the more gradual quarterly steps from US$6.3 million in Q1 2025 to US$10.3 million in Q2 2026.

Supporters pointing to earnings strength can also refer to trailing revenue of US$82.0 million versus US$64.1 million at the start of the comparison window, which lines up with the higher profit base.

At the same time, the move in quarterly net income from US$7.5 million in Q2 2025 to US$9.3 million in Q4 2025 and US$10.3 million in Q2 2026 gives that bullish argument a concrete earnings path to reference.

Over the past year Greene County Bancorp shifted from quarterly net income in the mid US$6 million range to over US$10 million, and bulls argue that this profit profile marks a step up from its longer term trend.

🐂 Greene County Bancorp Bull Case

Margins And Loan Quality Work Together

The trailing net profit margin of 43.6% compared with 38.3% a year earlier sits alongside non performing loans that ranged between US$2.9 million and US$4.1 million over the last six reported quarters, with Q2 2026 non performing loans last stated at US$3.6 million.

For investors leaning bullish, the combination of a higher trailing margin and relatively small non performing loan figures compared to total loans, which moved from US$1,501.2 million in Q1 2025 to US$1,670.8 million in Q1 2026, can be interpreted as evidence that profitability and asset quality are working together rather than pulling in opposite directions, although the data also shows non performing loans fluctuating within a narrow band instead of following a single clear direction.

Supporters who focus on credit quality can point out that non performing loans were US$4.1 million in Q2 2025 and US$3.0 million in Q4 2025, so the latest US$3.6 million sits inside that recent range while total loans are higher than a year earlier.

The margin picture, with a trailing level of 43.6%, gives that bullish reading more weight because it links loan book performance to earnings, rather than relying on credit metrics alone.

P/E Of 11.6x And DCF Fair Value Of US$32.47

At a share price of US$23.03, the stock trades on a trailing P/E of 11.6x, which is below the 15.1x peer average and close to the US banks industry at 11.8x, while a DCF fair value of US$32.47 is above the current price.

What is interesting for a bullish angle is that the trailing 37.4% earnings growth and 43.6% net margin sit beside a P/E that is below peers and a DCF fair value that is higher than the current US$23.03 share price. Some investors may see this as a gap between reported profitability and how the market is pricing the company.

Supporters of that view can point to trailing twelve month EPS of US$2.15 versus US$1.44 at the start of the period, which means the 11.6x multiple is sitting on a higher earnings base than a year ago.

The comparison between the current price and the DCF fair value of US$32.47 also gives those bullish arguments a specific reference point, as it ties valuation back to the cash flow based estimate in the data rather than only to Next Steps

Don't just look at this quarter; the real story is in the long-term trend. We've done an in-depth analysis on Greene County Bancorp's growth and its valuation to see if today's price is a bargain. Add the company to your watchlist or portfolio now so you don't miss the next big move.

See What Else Is Out There

Greene County Bancorp’s story leans heavily on recent earnings strength, while loan quality and non performing loans remain in a tight range without a clearly improving trend.

If you would rather focus on companies where balance sheet strength and lower credit risk are clearer, check out our solid balance sheet and fundamentals stocks screener (391 results) today and compare options side by side.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.