Please use a PC Browser to access Register-Tadawul

Get It

Improved Revenues Required Before Zamil Industrial Investment Company (TADAWUL:2240) Stock's 27% Jump Looks Justified

SENAAT 2240.SA | 36.84 | -0.49% |

Zamil Industrial Investment Company (TADAWUL:2240) shareholders have had their patience rewarded with a 27% share price jump in the last month. The last 30 days bring the annual gain to a very sharp 100%.

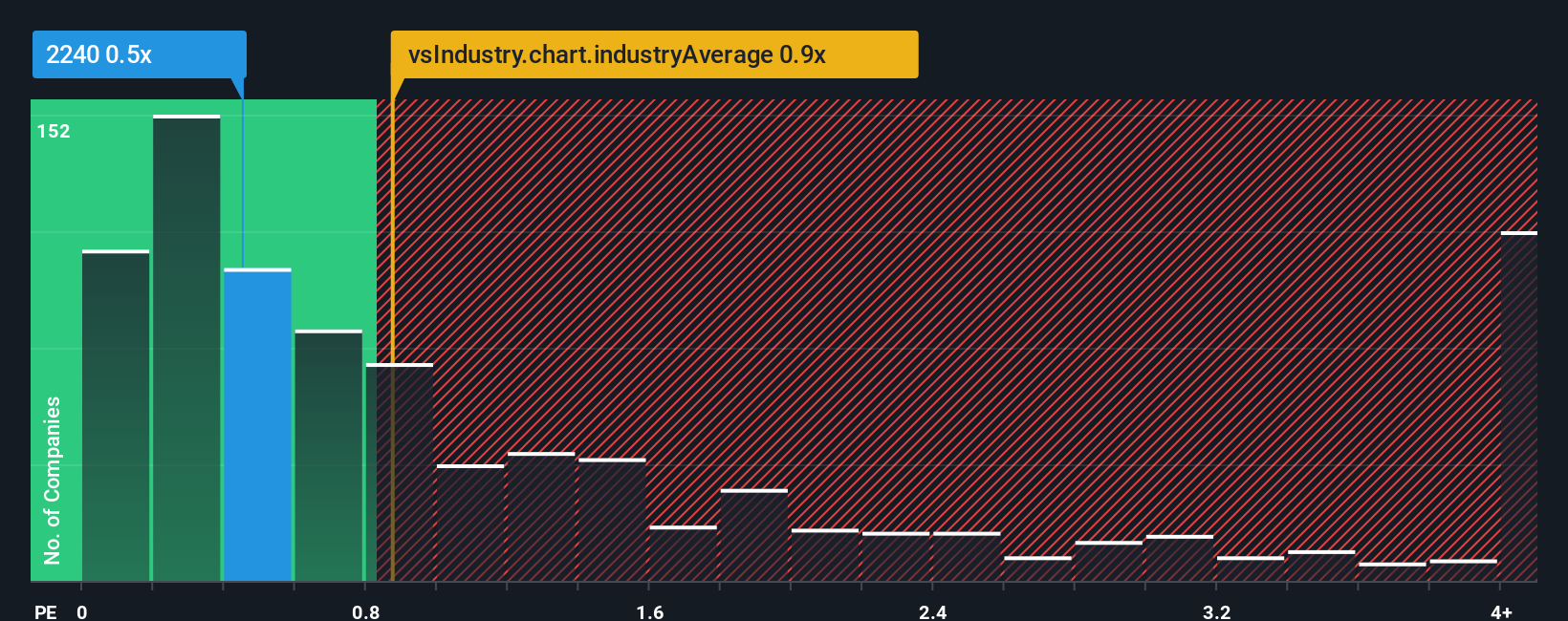

Although its price has surged higher, Zamil Industrial Investment's price-to-sales (or "P/S") ratio of 0.5x might still make it look like a buy right now compared to the Metals and Mining industry in Saudi Arabia, where around half of the companies have P/S ratios above 1x and even P/S above 3x are quite common. Nonetheless, we'd need to dig a little deeper to determine if there is a rational basis for the reduced P/S.

With revenue growth that's superior to most other companies of late, Zamil Industrial Investment has been doing relatively well. It might be that many expect the strong revenue performance to degrade substantially, which has repressed the share price, and thus the P/S ratio. If not, then existing shareholders have reason to be quite optimistic about the future direction of the share price.

Want the full picture on analyst estimates for the company? Then our free report on Zamil Industrial Investment will help you uncover what's on the horizon.In order to justify its P/S ratio, Zamil Industrial Investment would need to produce sluggish growth that's trailing the industry.

If we review the last year of revenue growth, the company posted a terrific increase of 27%. The latest three year period has also seen an excellent 82% overall rise in revenue, aided by its short-term performance. Accordingly, shareholders would have definitely welcomed those medium-term rates of revenue growth.

Looking ahead now, revenue is anticipated to climb by 6.1% during the coming year according to the one analyst following the company. With the industry predicted to deliver 11% growth, the company is positioned for a weaker revenue result.

With this information, we can see why Zamil Industrial Investment is trading at a P/S lower than the industry. Apparently many shareholders weren't comfortable holding on while the company is potentially eyeing a less prosperous future.

The latest share price surge wasn't enough to lift Zamil Industrial Investment's P/S close to the industry median. While the price-to-sales ratio shouldn't be the defining factor in whether you buy a stock or not, it's quite a capable barometer of revenue expectations.

We've established that Zamil Industrial Investment maintains its low P/S on the weakness of its forecast growth being lower than the wider industry, as expected. Shareholders' pessimism on the revenue prospects for the company seems to be the main contributor to the depressed P/S. Unless these conditions improve, they will continue to form a barrier for the share price around these levels.

It's important to make sure you look for a great company, not just the first idea you come across. So if growing profitability aligns with your idea of a great company, take a peek at this free list of interesting companies with strong recent earnings growth (and a low P/E).

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.