Invesco Mortgage Capital (IVR) Dividend Coverage Concerns Challenge Bullish Yield Narratives

Invesco Mortgage Capital Inc. IVR | 8.03 8.03 | -1.47% 0.00% Post |

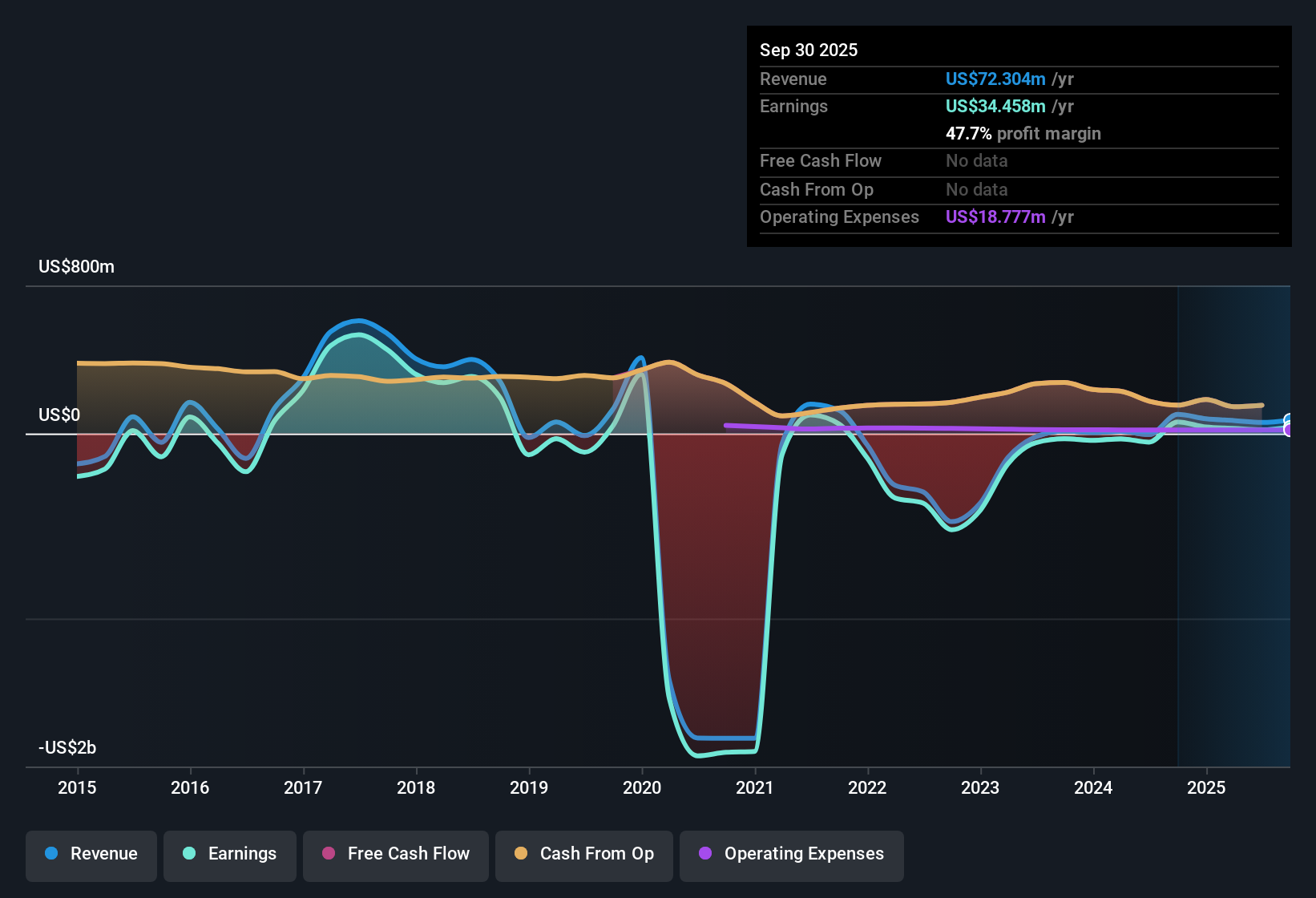

Invesco Mortgage Capital (IVR) just posted its FY 2025 numbers with Q4 revenue of US$56.1 million and basic EPS of US$0.68, giving investors a fresh read on how the portfolio is trading through the mortgage market. Over recent periods, revenue has ranged from US$8.5 million in Q4 2024 to US$57.9 million in Q3 2025, while quarterly EPS has swung between a loss of US$0.40 in Q2 2025 and a gain of US$0.74 in Q3 2025, setting the backdrop for today’s print. With a trailing 12 month net margin of 47.7% compared with a prior 60.8%, the latest results point to solid income generation but with some margin compression now front of mind for investors.

See our full analysis for Invesco Mortgage Capital.With the numbers on the table, the next step is to see how this earnings profile lines up with the prevailing stories around IVR, highlighting where recent performance supports the common narratives and where it pushes back against them.

47.7% net margin now, but below last year’s 60.8%

- IVR’s trailing 12 month net profit margin sits at 47.7%, compared with 60.8% a year earlier, so the business is still generating income on its mortgage portfolio but is doing so with less margin than before.

- What stands out for a bullish view is that this margin compression sits alongside a description of high quality past earnings and multi year profitability. Yet:

- Reported earnings growth over the past five years is cited at 63% per year, which lines up with the idea that IVR has a strong longer run earnings record even though the latest 12 month margin is lower than the prior 60.8% figure.

- That mix of high historical earnings growth and a step down in margin gives bulls something to point to on track record, while also reminding them that the recent period has not matched the prior year’s profitability level.

P/E of 17.9x sits between market and sector

- The shares trade on a P/E of 17.9x, which is below the broader US market average of 19.2x and well below the peer average of 28.7x, but above the US Mortgage REITs industry average of 13x, so IVR is priced in the middle of those reference points.

- Analysts who lean bullish often argue that earnings quality can justify paying a higher multiple. In this case:

- The company is described as having been profitable over the past five years with reported earnings growth of 63% per year, which can help explain why the P/E sits above the 13x industry level even though it is below the wider market and peer averages.

- At the same time, the drop in trailing net margin from 60.8% to 47.7% means anyone leaning bullish has to weigh that mixed profitability trend against the mid range valuation the 17.9x P/E implies.

16.76% dividend yield alongside weak coverage and debt strain

- The stock is offering a 16.76% dividend yield, but that payout is flagged as not well covered by earnings over the last year and sits next to a key risk that debt is not well covered by operating cash flow.

- Critics highlight these as clear bearish points for an income focused name, and the numbers back up those concerns:

- The combination of a high dividend yield and weak earnings coverage means recent profit levels have not comfortably supported the cash being returned to shareholders.

- Debt that is not well covered by operating cash flow, together with a high payout and recent shareholder dilution, points straight at balance sheet and income reliability risks that cautious investors tend to focus on.

Next Steps

Don't just look at this quarter; the real story is in the long-term trend. We've done an in-depth analysis on Invesco Mortgage Capital's growth and its valuation to see if today's price is a bargain. Add the company to your watchlist or portfolio now so you don't miss the next big move.

See What Else Is Out There

Between the step down in net margin, a high 16.76% dividend that is not well covered, and debt pressure, IVR’s income profile looks stretched.

If those strains on payouts and leverage concern you, check out solid balance sheet and fundamentals stocks screener (391 results) to focus on companies built on stronger cash coverage and more resilient balance sheets.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.