Please use a PC Browser to access Register-Tadawul

Get It

Investors Appear Satisfied With Ramaco Resources, Inc.'s (NASDAQ:METC) Prospects As Shares Rocket 27%

Ramaco Resources, Inc. Class A METC | 16.56 | -0.96% |

Ramaco Resources, Inc. (NASDAQ:METC) shareholders are no doubt pleased to see that the share price has bounced 27% in the last month, although it is still struggling to make up recently lost ground. The annual gain comes to 127% following the latest surge, making investors sit up and take notice.

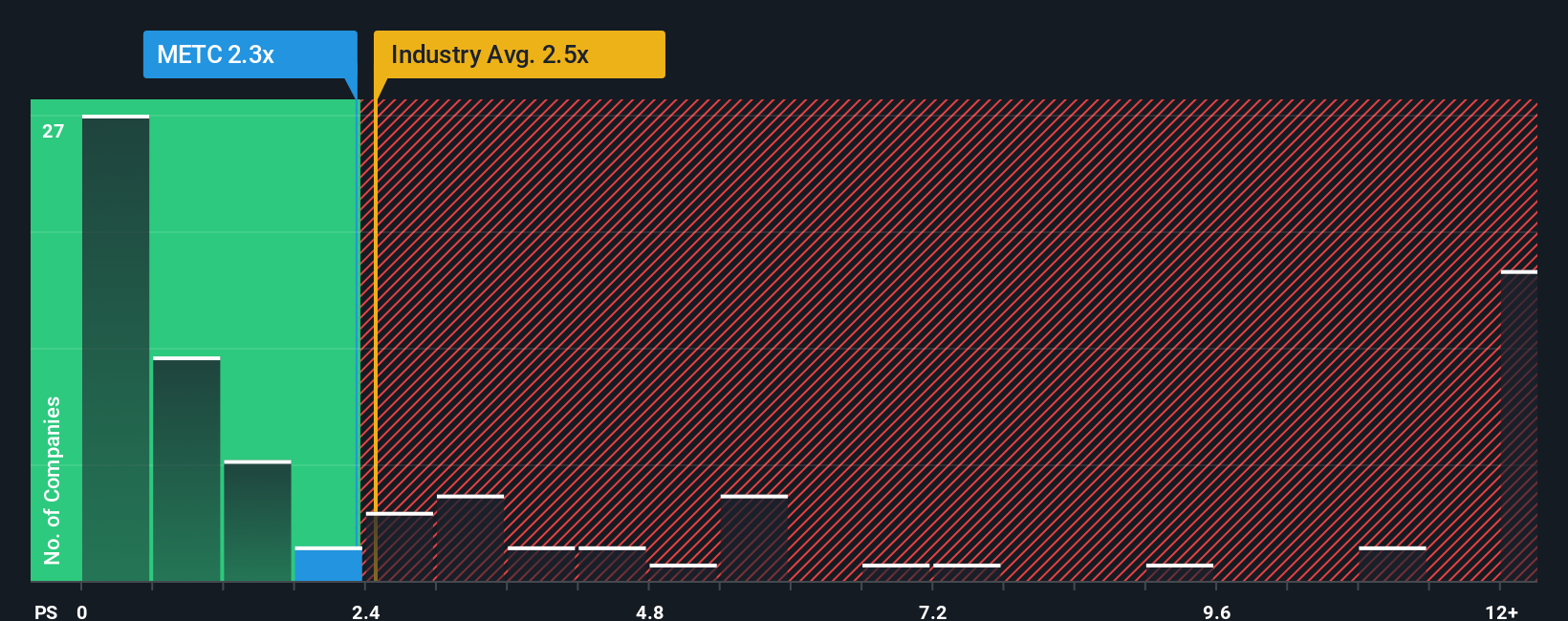

In spite of the firm bounce in price, it's still not a stretch to say that Ramaco Resources' price-to-sales (or "P/S") ratio of 2.3x right now seems quite "middle-of-the-road" compared to the Metals and Mining industry in the United States, where the median P/S ratio is around 2.6x. However, investors might be overlooking a clear opportunity or potential setback if there is no rational basis for the P/S.

Ramaco Resources could be doing better as its revenue has been going backwards lately while most other companies have been seeing positive revenue growth. One possibility is that the P/S ratio is moderate because investors think this poor revenue performance will turn around. You'd really hope so, otherwise you're paying a relatively elevated price for a company with this sort of growth profile.

Keen to find out how analysts think Ramaco Resources' future stacks up against the industry? In that case, our free report is a great place to start.Ramaco Resources' P/S ratio would be typical for a company that's only expected to deliver moderate growth, and importantly, perform in line with the industry.

Taking a look back first, the company's revenue growth last year wasn't something to get excited about as it posted a disappointing decline of 17%. Regardless, revenue has managed to lift by a handy 12% in aggregate from three years ago, thanks to the earlier period of growth. Accordingly, while they would have preferred to keep the run going, shareholders would be roughly satisfied with the medium-term rates of revenue growth.

Shifting to the future, estimates from the eight analysts covering the company suggest revenue should grow by 16% each year over the next three years. With the industry predicted to deliver 15% growth per year, the company is positioned for a comparable revenue result.

In light of this, it's understandable that Ramaco Resources' P/S sits in line with the majority of other companies. Apparently shareholders are comfortable to simply hold on while the company is keeping a low profile.

Its shares have lifted substantially and now Ramaco Resources' P/S is back within range of the industry median. We'd say the price-to-sales ratio's power isn't primarily as a valuation instrument but rather to gauge current investor sentiment and future expectations.

A Ramaco Resources' P/S seems about right to us given the knowledge that analysts are forecasting a revenue outlook that is similar to the Metals and Mining industry. At this stage investors feel the potential for an improvement or deterioration in revenue isn't great enough to push P/S in a higher or lower direction. Unless these conditions change, they will continue to support the share price at these levels.

Having said that, be aware Ramaco Resources is showing 2 warning signs in our investment analysis, you should know about.

If companies with solid past earnings growth is up your alley, you may wish to see this free collection of other companies with strong earnings growth and low P/E ratios.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.