Please use a PC Browser to access Register-Tadawul

Get It

Investors Will Want H.B. Fuller's (NYSE:FUL) Growth In ROCE To Persist

H.B. Fuller Company FUL | 65.94 | +1.06% |

What are the early trends we should look for to identify a stock that could multiply in value over the long term? Amongst other things, we'll want to see two things; firstly, a growing return on capital employed (ROCE) and secondly, an expansion in the company's amount of capital employed. If you see this, it typically means it's a company with a great business model and plenty of profitable reinvestment opportunities. With that in mind, we've noticed some promising trends at H.B. Fuller (NYSE:FUL) so let's look a bit deeper.

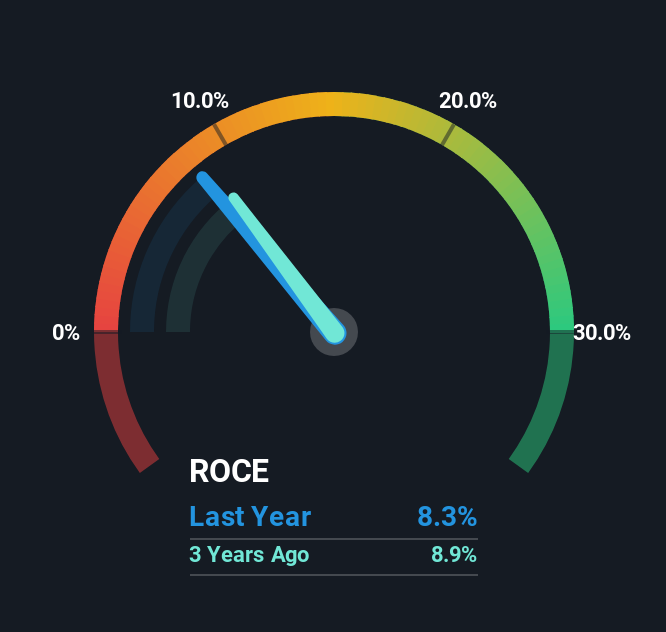

For those who don't know, ROCE is a measure of a company's yearly pre-tax profit (its return), relative to the capital employed in the business. The formula for this calculation on H.B. Fuller is:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

0.083 = US$371m ÷ (US$5.2b - US$674m) (Based on the trailing twelve months to August 2025).

Therefore, H.B. Fuller has an ROCE of 8.3%. In absolute terms, that's a low return but it's around the Chemicals industry average of 9.3%.

In the above chart we have measured H.B. Fuller's prior ROCE against its prior performance, but the future is arguably more important. If you'd like to see what analysts are forecasting going forward, you should check out our free analyst report for H.B. Fuller .

We're glad to see that ROCE is heading in the right direction, even if it is still low at the moment. Over the last five years, returns on capital employed have risen substantially to 8.3%. Basically the business is earning more per dollar of capital invested and in addition to that, 27% more capital is being employed now too. This can indicate that there's plenty of opportunities to invest capital internally and at ever higher rates, a combination that's common among multi-baggers.

A company that is growing its returns on capital and can consistently reinvest in itself is a highly sought after trait, and that's what H.B. Fuller has. Since the stock has only returned 21% to shareholders over the last five years, the promising fundamentals may not be recognized yet by investors. So with that in mind, we think the stock deserves further research.

B. Fuller (1 is concerning) you should be aware of.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.