Please use a PC Browser to access Register-Tadawul

Get It

Is International Flavors & Fragrances (NYSE:IFF) A Risky Investment?

International Flavors & Fragrances Inc. IFF | 63.26 | +0.02% |

Warren Buffett famously said, 'Volatility is far from synonymous with risk.' So it might be obvious that you need to consider debt, when you think about how risky any given stock is, because too much debt can sink a company. Importantly, International Flavors & Fragrances Inc. (NYSE:IFF) does carry debt. But the real question is whether this debt is making the company risky.

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. If things get really bad, the lenders can take control of the business. While that is not too common, we often do see indebted companies permanently diluting shareholders because lenders force them to raise capital at a distressed price. Of course, debt can be an important tool in businesses, particularly capital heavy businesses. The first step when considering a company's debt levels is to consider its cash and debt together.

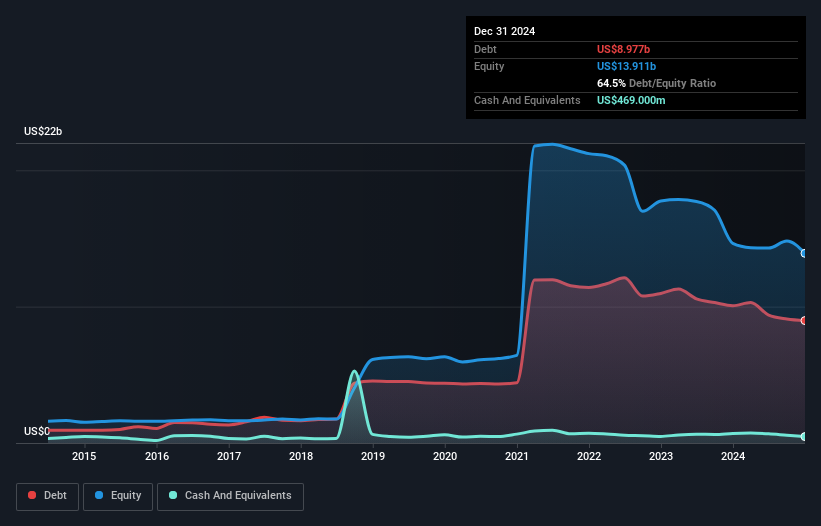

You can click the graphic below for the historical numbers, but it shows that International Flavors & Fragrances had US$8.98b of debt in December 2024, down from US$10.1b, one year before. On the flip side, it has US$469.0m in cash leading to net debt of about US$8.51b.

We can see from the most recent balance sheet that International Flavors & Fragrances had liabilities of US$4.33b falling due within a year, and liabilities of US$10.4b due beyond that. On the other hand, it had cash of US$469.0m and US$1.78b worth of receivables due within a year. So its liabilities total US$12.5b more than the combination of its cash and short-term receivables.

This is a mountain of leverage even relative to its gargantuan market capitalization of US$18.7b. Should its lenders demand that it shore up the balance sheet, shareholders would likely face severe dilution.

We use two main ratios to inform us about debt levels relative to earnings. The first is net debt divided by earnings before interest, tax, depreciation, and amortization (EBITDA), while the second is how many times its earnings before interest and tax (EBIT) covers its interest expense (or its interest cover, for short). The advantage of this approach is that we take into account both the absolute quantum of debt (with net debt to EBITDA) and the actual interest expenses associated with that debt (with its interest cover ratio).

While International Flavors & Fragrances's debt to EBITDA ratio (4.9) suggests that it uses some debt, its interest cover is very weak, at 2.5, suggesting high leverage. In large part that's due to the company's significant depreciation and amortisation charges, which arguably mean its EBITDA is a very generous measure of earnings, and its debt may be more of a burden than it first appears. So shareholders should probably be aware that interest expenses appear to have really impacted the business lately. On a slightly more positive note, International Flavors & Fragrances grew its EBIT at 18% over the last year, further increasing its ability to manage debt. There's no doubt that we learn most about debt from the balance sheet. But it is future earnings, more than anything, that will determine International Flavors & Fragrances's ability to maintain a healthy balance sheet going forward. So if you want to see what the professionals think, you might find this free report on analyst profit forecasts to be interesting.

But our final consideration is also important, because a company cannot pay debt with paper profits; it needs cold hard cash. So we always check how much of that EBIT is translated into free cash flow. Over the most recent three years, International Flavors & Fragrances recorded free cash flow worth 59% of its EBIT, which is around normal, given free cash flow excludes interest and tax. This cold hard cash means it can reduce its debt when it wants to.

While International Flavors & Fragrances's interest cover makes us cautious about it, its track record of managing its debt, based on its EBITDA, is no better. But on the brighter side of life, its EBIT growth rate leaves us feeling more frolicsome. We think that International Flavors & Fragrances's debt does make it a bit risky, after considering the aforementioned data points together. That's not necessarily a bad thing, since leverage can boost returns on equity, but it is something to be aware of. There's no doubt that we learn most about debt from the balance sheet. But ultimately, every company can contain risks that exist outside of the balance sheet. These risks can be hard to spot.

At the end of the day, it's often better to focus on companies that are free from net debt. You can access our special list of such companies (all with a track record of profit growth). It's free.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.