Please use a PC Browser to access Register-Tadawul

Get It

Is It Time To Reassess Recursion Pharmaceuticals (RXRX) After Recent Share Price Weakness

Recursion Pharmaceuticals, Inc. Class A RXRX | 3.42 | -8.06% |

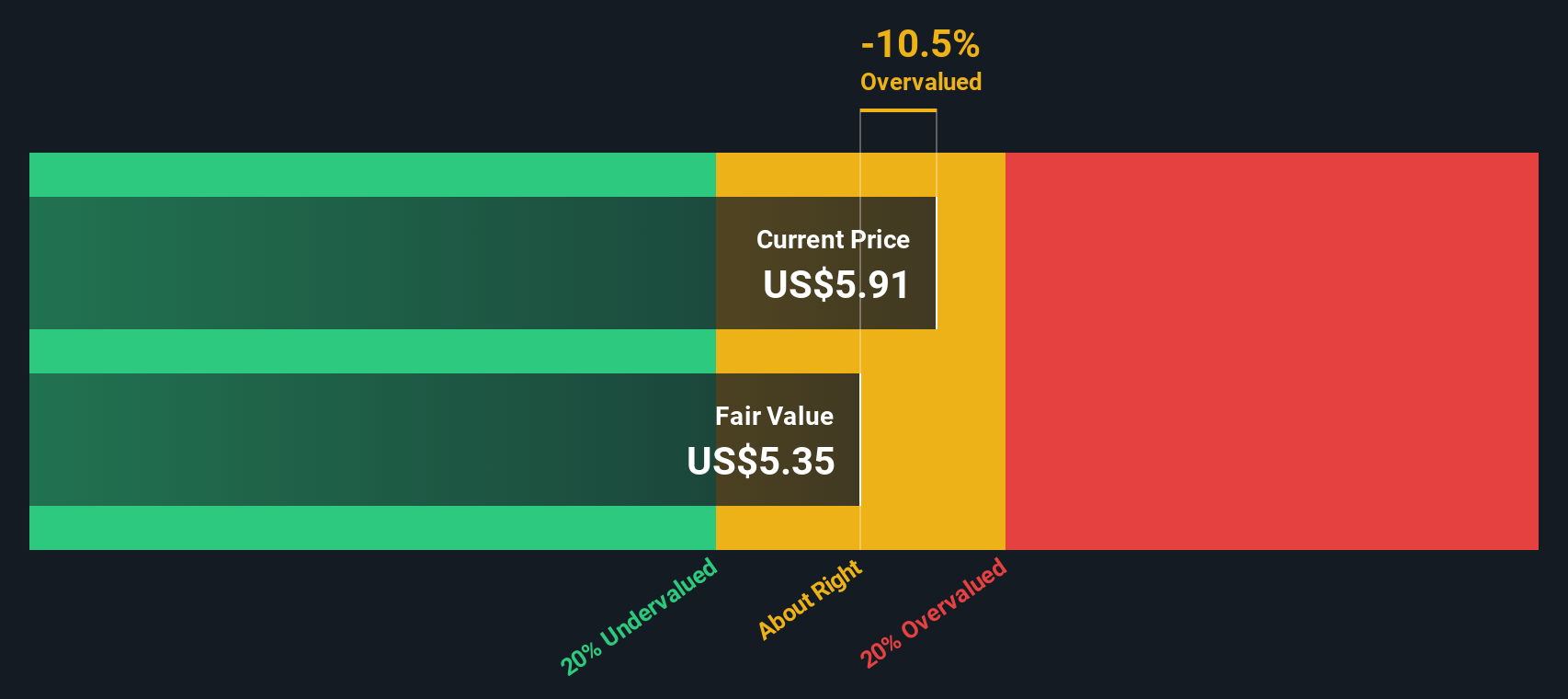

A Discounted Cash Flow, or DCF, model takes estimates of a company’s future cash flows and discounts them back to today’s dollars using a required rate of return. The goal is to see what those future cash flows might be worth right now.

For Recursion Pharmaceuticals, the model used is a 2 Stage Free Cash Flow to Equity approach. The latest twelve month free cash flow is a loss of $453.74 million. Analysts provide specific free cash flow estimates out to 2030, with Simply Wall St extrapolating beyond the early forecast years. Within these projections, free cash flow for 2030 is estimated at $176 million, with interim years showing both negative and positive figures as the business is expected to move toward positive cash generation.

When all those projected cash flows are discounted back, the resulting estimated intrinsic value comes out at about $9.31 per share. Compared with the recent share price of $4.67, the model implies the stock is around 49.8% undervalued on this basis.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Recursion Pharmaceuticals is undervalued by 49.8%. Track this in your watchlist or portfolio, or discover 863 more undervalued stocks based on cash flows.

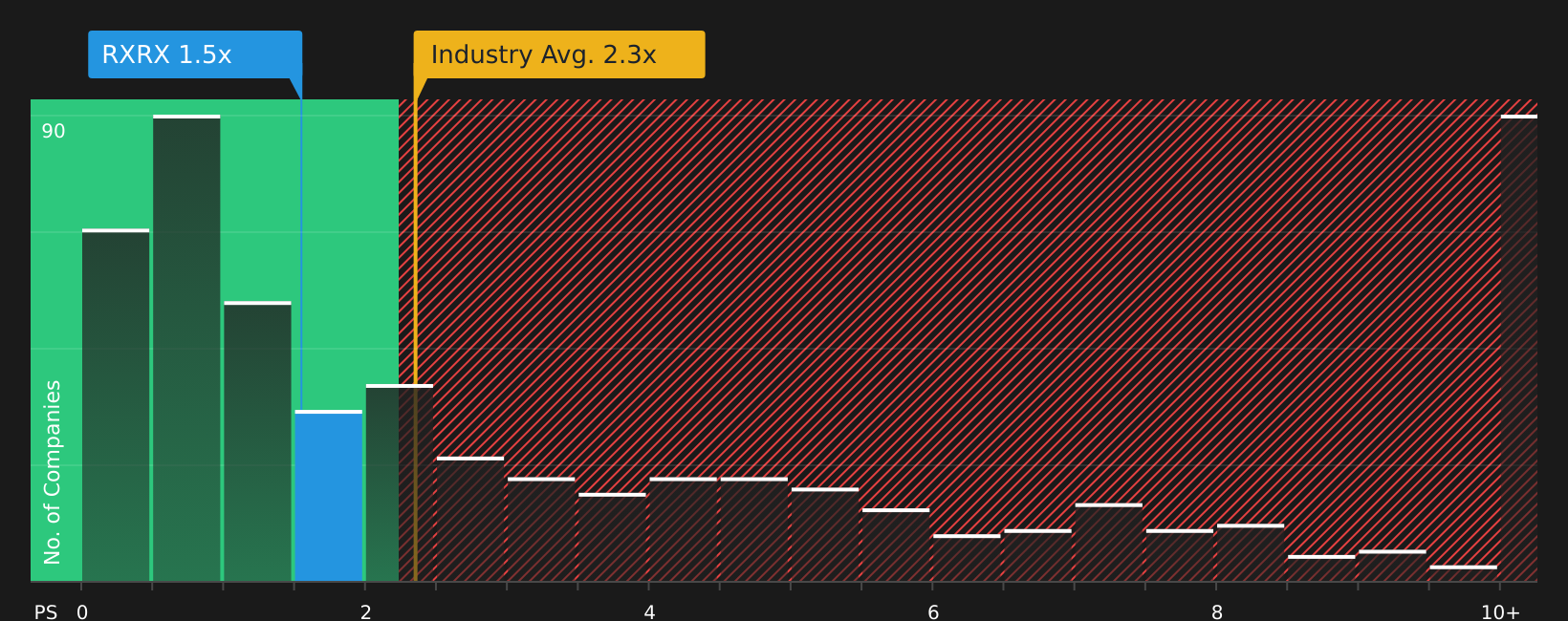

For many profitable companies, the price to book, or P/B, ratio is a useful way to see how the market values the net assets on the balance sheet. Investors often accept a higher P/B when they expect stronger growth or view the business as less risky, while a lower P/B can reflect weaker growth expectations or higher perceived risk.

Growth expectations and risk matter because they tend to shape what feels like a normal or fair multiple. Higher growth and lower risk can justify a richer multiple, while slower growth or higher uncertainty usually point to a more modest one.

Recursion Pharmaceuticals currently trades on a P/B of 2.32x. That sits below the Biotechs industry average P/B of 2.61x and well below the peer average of 63.48x that Simply Wall St has compiled. Simply Wall St also calculates a Fair Ratio, which is the P/B multiple it would expect for the company given factors such as earnings growth, industry, profit margins, market cap and specific risks.

This Fair Ratio is designed to be more tailored than a simple comparison with peers or the broad industry, because those benchmarks can mix very different business models, risk profiles and growth outlooks. By folding in Recursion Pharmaceuticals specific characteristics, the Fair Ratio aims to give a more company-accurate reference point.

In this case, Simply Wall St has not reported a specific Fair Ratio figure, so it is not possible to say purely on this basis whether the current 2.32x P/B looks underpriced, overpriced or about right.

Result: ABOUT RIGHT

P/B ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1445 companies where insiders are betting big on explosive growth.

Earlier we mentioned that there is an even better way to understand valuation, so let us introduce you to Narratives, which are simply your story about Recursion Pharmaceuticals, linked directly to your own revenue, earnings and margin estimates, a fair value, and then a clear comparison to today’s share price.

On Simply Wall St’s Community page, millions of investors use Narratives as an accessible tool to spell out why they think a company will perform a certain way, connect that story to a financial forecast, and see a fair value that updates automatically when new information like news or earnings is added.

For example, one Recursion Pharmaceuticals Narrative might lean on the view that AI enabled drug discovery, recent TUPELO trial data and a fair value of about US$7 per share support a higher future potential. Another more cautious Narrative could stress pipeline, funding and competition risks and lean closer to a fair value near US$3. Seeing these side by side helps you decide whether the current price looks attractive or not for your own approach.

Do you think there's more to the story for Recursion Pharmaceuticals? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.