Is It Too Early To Reconsider Hims & Hers Health (HIMS) After Recent Share Price Pullback?

Hims & Hers Health HIMS | 0.00 |

- If you are wondering whether Hims & Hers Health is reasonably priced at its current level, this article will walk you through what the numbers are actually saying about the stock.

- The share price is at US$29.62, with a 7 day return of 5.6% decline, a 30 day return of 14.6% decline, and a year to date move of 11.3% decline. The 1 year return stands at 4.0% decline and the 3 year return is very large.

- Recent coverage has focused on how the business model is resonating with consumers in areas like telehealth and personalized treatments, alongside questions about how sustainable that traction may be. These themes help frame why the stock has seen periods of strong multi year returns as well as shorter term pullbacks.

- Based on our valuation checks, Hims & Hers Health currently has a valuation score of 2 out of 6. Next we will look at what different valuation methods say about that score, before finishing with a way to assess value that goes beyond simple multiples.

Hims & Hers Health scores just 2/6 on our valuation checks. See what other red flags we found in the full valuation breakdown.

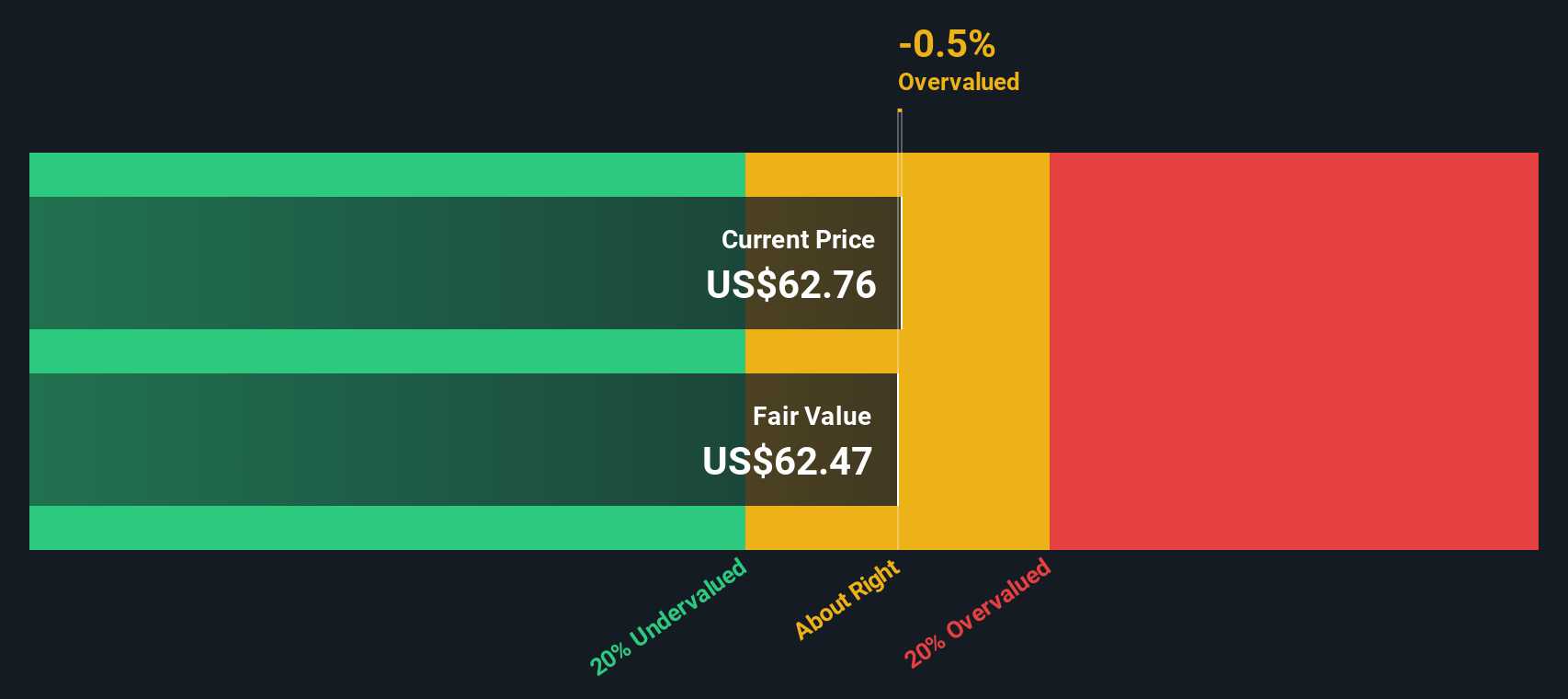

Approach 1: Hims & Hers Health Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow, or DCF, model takes estimates of the cash a company could generate in the future, then discounts those cash flows back into today’s dollars to arrive at an intrinsic value per share.

For Hims & Hers Health, the model used is a 2 Stage Free Cash Flow to Equity approach based on cash flow projections. The latest twelve month Free Cash Flow is about $189.4 million. Analyst estimates and subsequent extrapolations extend out to 2035, with projected Free Cash Flow of $502.5 million in 2030 and later years estimated using gradually moderating growth rates.

Pulling all of those discounted cash flows together, the DCF model indicates an intrinsic value of about $63.39 per share, compared with the current share price of $29.62. That implies an intrinsic discount of 53.3%, based on this method alone.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Hims & Hers Health is undervalued by 53.3%. Track this in your watchlist or portfolio, or discover 864 more undervalued stocks based on cash flows.

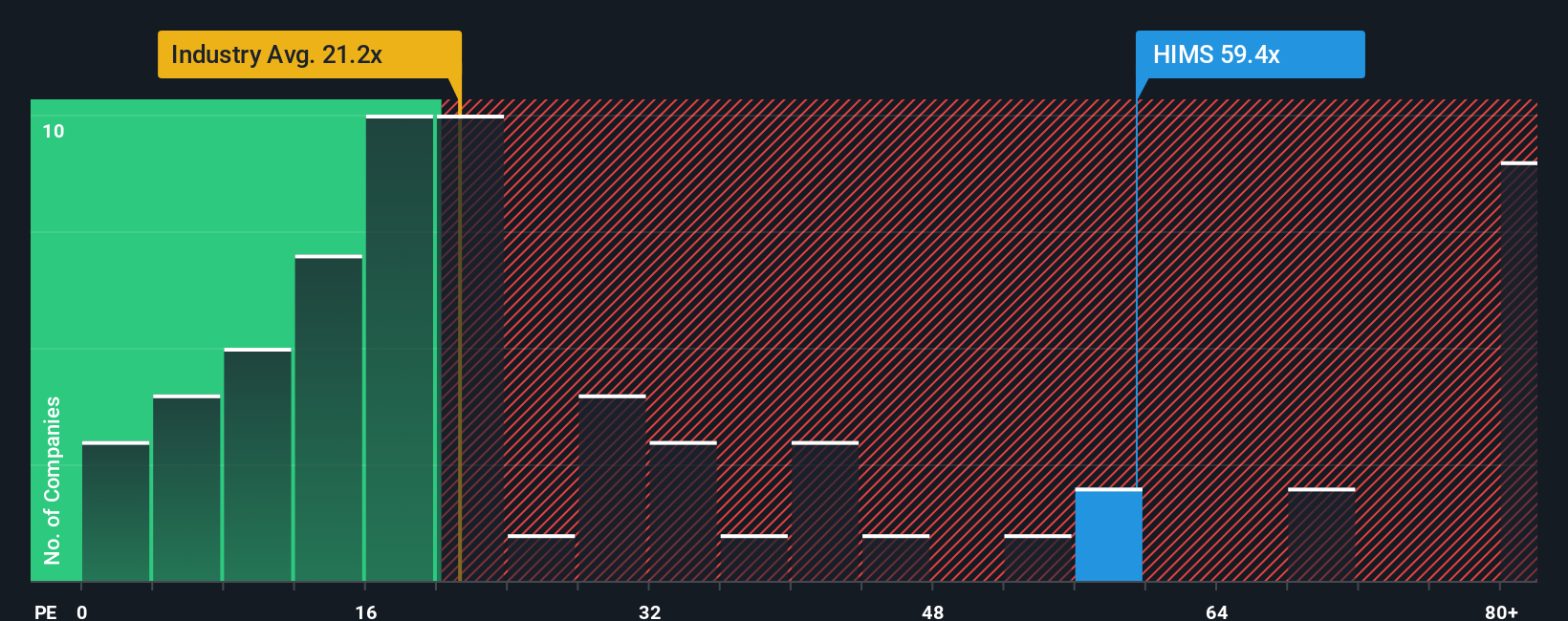

Approach 2: Hims & Hers Health Price vs Earnings (P/E)

For profitable companies, the P/E ratio is a useful way to see how much you are paying for each dollar of current earnings. This makes it a straightforward tool to compare businesses that already generate positive profits.

What counts as a reasonable P/E depends on what the market expects from a company. Higher expected earnings growth or lower perceived risk can justify a higher P/E, while slower expected growth or higher risk usually point to a lower, more conservative P/E being appropriate.

Hims & Hers Health currently trades on a P/E of 50.40x. That sits above the Healthcare industry average P/E of about 23.37x and also above the peer average of 33.55x. Simply Wall St’s Fair Ratio for Hims & Hers Health is 27.16x, which is its view of what a “normal” P/E could look like after considering factors such as earnings growth, industry, profit margins, market cap and company specific risks.

The Fair Ratio is more tailored than a simple industry or peer comparison, because it adjusts for those company characteristics rather than assuming all Healthcare names should trade on the same multiple. Compared with the current P/E of 50.40x, the Fair Ratio of 27.16x suggests the stock is pricing in more optimism than this framework supports.

Result: OVERVALUED

P/E ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1428 companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your Hims & Hers Health Narrative

Earlier we mentioned that there is an even better way to understand valuation, so let us introduce you to Narratives, which let you attach a clear story about Hims & Hers Health to the numbers you care about, such as your own view of fair value and your expectations for future revenue, earnings and margins.

A Narrative links what you believe about a company, for example how its telehealth model might evolve, to a structured forecast and then to a fair value estimate that you can compare directly with today’s share price.

On Simply Wall St, used by millions of investors, Narratives sit in the Community page and are designed to be quick to set up, so you can test a view in minutes rather than building a full spreadsheet model.

Once you have a Narrative, you can see whether your fair value is above or below the current price, which can help you decide if Hims & Hers Health looks more like a potential opportunity or something to be cautious about.

Narratives also update automatically when fresh information such as news or earnings is released, so your story and valuation stay aligned without constant manual tweaks, and in the case of Hims & Hers Health you might see one investor with a relatively high fair value and another with a much lower figure based on more cautious assumptions.

Do you think there's more to the story for Hims & Hers Health? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.