Please use a PC Browser to access Register-Tadawul

Get It

Is NuScale Power (SMR) Pricing Reflect Its DCF Upside After Recent Nuclear Sector Headlines

NuScale Power Corporation Class A SMR | 13.44 | -8.20% |

A Discounted Cash Flow model takes estimates of a company’s future cash flows, then discounts them back to today to get an implied value per share. It is essentially asking what those future cash flows are worth in today’s dollars.

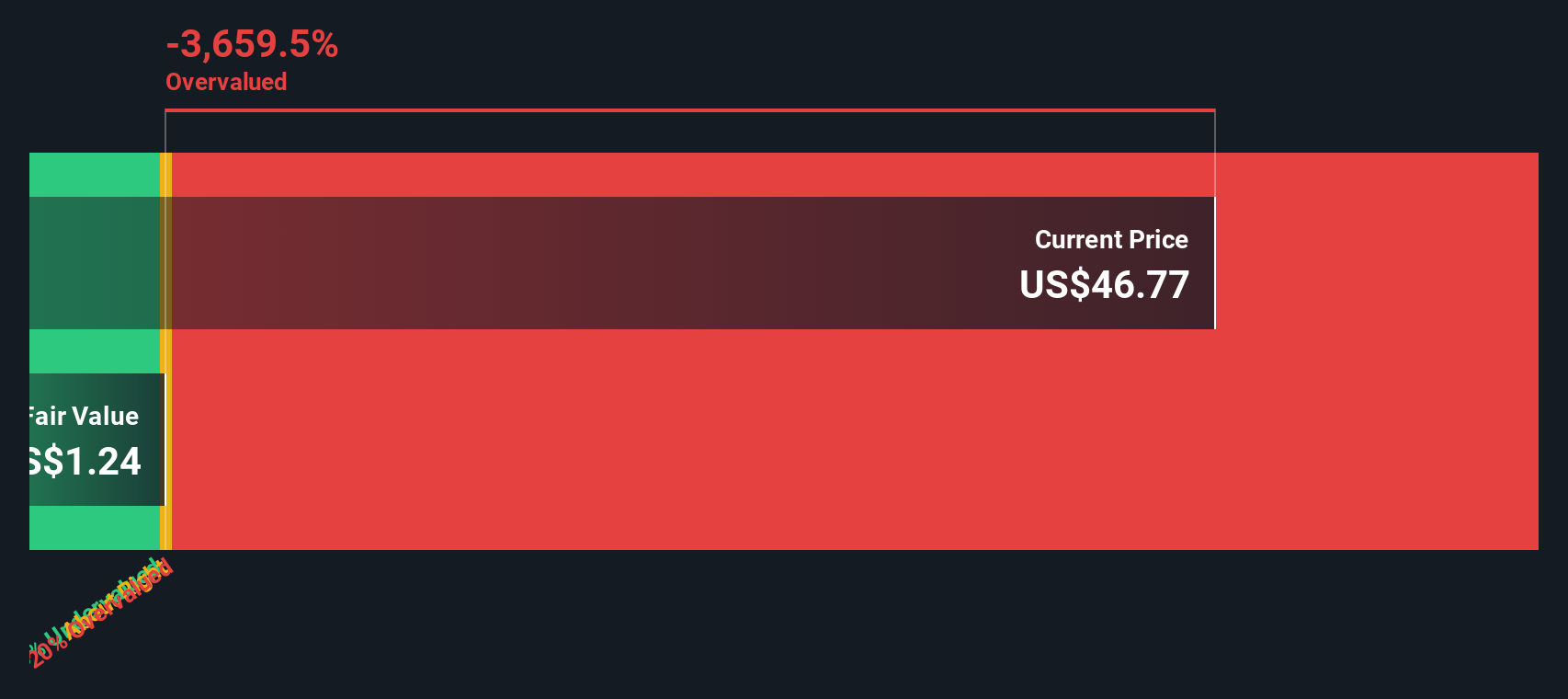

For NuScale Power, the model used is a 2 Stage Free Cash Flow to Equity approach based on cash flow projections. The latest twelve month free cash flow is a loss of $284.04 million. Analyst and extrapolated estimates in the model show free cash flow remaining negative in the medium term, followed by a shift to positive, with a projected free cash flow of $1,792.81 million in 2035. All figures are expressed in dollars and discounted back using Simply Wall St’s assumptions.

Combining all those discounted cash flows, the model produces an estimated intrinsic value of about $50.92 per share. Compared with the current share price of $18.40, this suggests the stock is 63.9% undervalued according to this DCF framework.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests NuScale Power is undervalued by 63.9%. Track this in your watchlist or portfolio, or discover 888 more undervalued stocks based on cash flows.

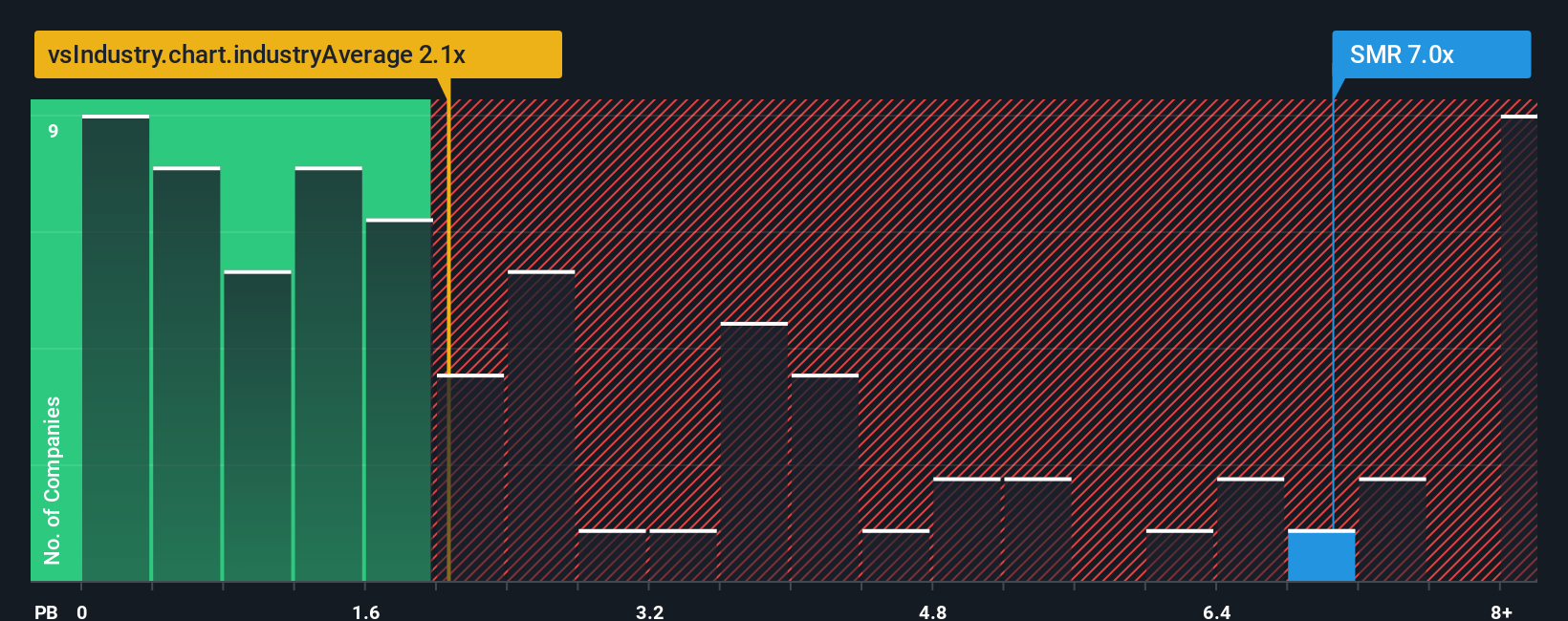

For companies where earnings and cash flows are not yet steady, the P/B ratio is often a useful cross check because it compares what you are paying in the market with the accounting value of the company’s net assets.

In general, higher growth expectations and lower perceived risk can support a higher “normal” multiple, while slower growth or higher risk tend to justify a lower one. It is therefore helpful to compare any P/B figure with relevant benchmarks rather than viewing it in isolation.

NuScale Power currently trades on a P/B of 6.28x. That sits above the Electrical industry average P/B of 2.71x and also above the peer group average of 19.90x. Simply Wall St goes one step further with a proprietary “Fair Ratio”, which is the P/B multiple it would expect for NuScale Power after accounting for factors like its earnings profile, growth characteristics, profit margins, industry, market cap and specific risks.

This Fair Ratio approach can be more tailored than a simple peer or industry comparison because it adjusts for company specific traits instead of assuming one size fits all. However, a Fair Ratio was not available for NuScale Power in the latest data set, so it is not possible to reach a clear P/B based conclusion here.

Result: ABOUT RIGHT

P/B ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1425 companies where insiders are betting big on explosive growth.

Earlier we mentioned that there is an even better way to understand valuation, so let us introduce Narratives, which are simply your story about a company tied directly to your numbers, things like your assumed fair value and your own estimates for future revenue, earnings and margins.

A Narrative links what you believe about NuScale Power’s business, for example its small modular reactor opportunity and funding outlook, to a financial forecast and then to a fair value that you can compare with today’s US$18.40 share price to decide whether you see room to buy, sell, or wait.

You can build and review these Narratives on Simply Wall St’s Community page, where millions of investors share their views, and your Narrative will automatically refresh when new information such as earnings updates or news is added so your fair value view stays aligned with the latest data.

For NuScale Power, one investor might build a Narrative that points to a fair value close to the DCF estimate of about US$50.92, while another might anchor their Narrative near the current market price. This shows how the same facts can support very different but clearly framed decisions.

Do you think there's more to the story for NuScale Power? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.