Please use a PC Browser to access Register-Tadawul

Get It

Is Sportsman's Warehouse Holdings (NASDAQ:SPWH) Weighed On By Its Debt Load?

Sportsman's Warehouse Holdings, Inc. SPWH | 1.49 | -1.00% |

David Iben put it well when he said, 'Volatility is not a risk we care about. What we care about is avoiding the permanent loss of capital.' When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. We note that Sportsman's Warehouse Holdings, Inc. (NASDAQ:SPWH) does have debt on its balance sheet. But the more important question is: how much risk is that debt creating?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. Ultimately, if the company can't fulfill its legal obligations to repay debt, shareholders could walk away with nothing. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. Of course, debt can be an important tool in businesses, particularly capital heavy businesses. When we think about a company's use of debt, we first look at cash and debt together.

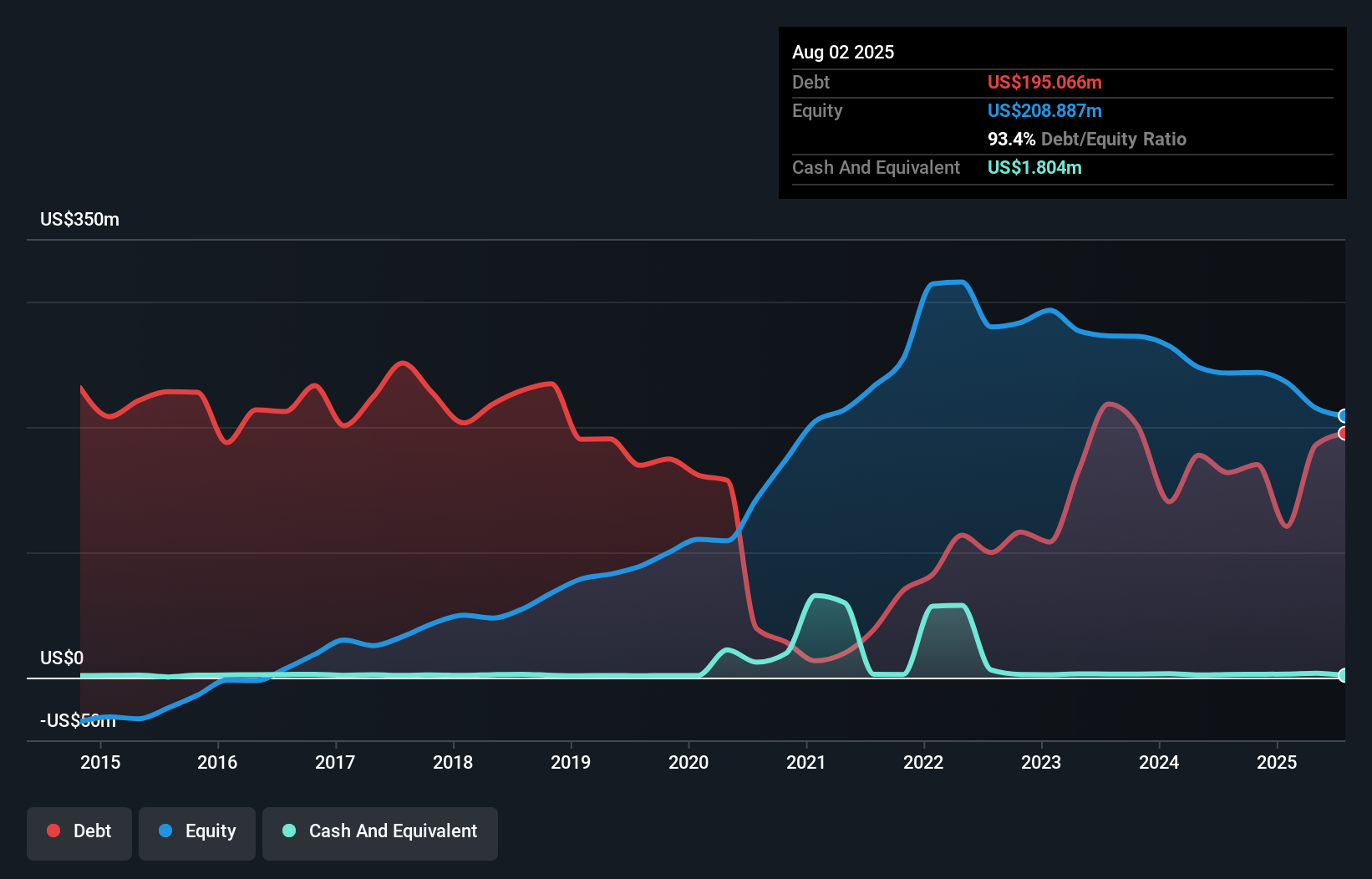

The image below, which you can click on for greater detail, shows that at August 2025 Sportsman's Warehouse Holdings had debt of US$195.1m, up from US$163.5m in one year. Net debt is about the same, since the it doesn't have much cash.

Zooming in on the latest balance sheet data, we can see that Sportsman's Warehouse Holdings had liabilities of US$392.8m due within 12 months and liabilities of US$347.1m due beyond that. Offsetting these obligations, it had cash of US$1.80m as well as receivables valued at US$2.67m due within 12 months. So its liabilities outweigh the sum of its cash and (near-term) receivables by US$735.5m.

The deficiency here weighs heavily on the US$115.3m company itself, as if a child were struggling under the weight of an enormous back-pack full of books, his sports gear, and a trumpet. So we'd watch its balance sheet closely, without a doubt. After all, Sportsman's Warehouse Holdings would likely require a major re-capitalisation if it had to pay its creditors today. There's no doubt that we learn most about debt from the balance sheet. But it is future earnings, more than anything, that will determine Sportsman's Warehouse Holdings's ability to maintain a healthy balance sheet going forward.

In the last year Sportsman's Warehouse Holdings had a loss before interest and tax, and actually shrunk its revenue by 2.9%, to US$1.2b. That's not what we would hope to see.

Importantly, Sportsman's Warehouse Holdings had an earnings before interest and tax (EBIT) loss over the last year. Indeed, it lost a very considerable US$12m at the EBIT level. When you combine this with the very significant balance sheet liabilities mentioned above, we are so wary of it that we are basically at a loss for the right words. Like every long-shot we're sure it has a glossy presentation outlining its blue-sky potential. But the reality is that it is low on liquid assets relative to liabilities, and it burned through US$55m in the last year. So we consider this a high risk stock, and we're worried its share price could sink faster than than a dingy with a great white shark attacking it. There's no doubt that we learn most about debt from the balance sheet. However, not all investment risk resides within the balance sheet - far from it.

When all is said and done, sometimes its easier to focus on companies that don't even need debt. Readers can access a list of growth stocks with zero net debt 100% free, right now.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.