Is There Now An Opportunity In Medical Properties Trust (MPW) After Tenant And Debt Concerns?

Medical Properties Trust, Inc. MPW | 0.00 |

- If you are wondering whether Medical Properties Trust is a bargain or a value trap at around US$5.11, it helps to step back and look at the full valuation picture rather than just the share price.

- The stock has had a mixed run, with a 1 year return of 17.3% alongside a 3 year return of 47.0% decline and a 5 year return of 64.4% decline, and it is roughly flat so far this year at 0.6% after a 1.7% decline over the last week and a 0.6% return over the last month.

- Recent news around Medical Properties Trust has focused heavily on its balance sheet flexibility, debt profile, and the health of key hospital tenants, which has kept attention on its ability to sustain operations and fund obligations. Commentary has also highlighted asset sales, operator restructurings, and portfolio adjustments as investors assess how these moves affect risk and potential value in the shares.

- On Simply Wall St’s 6 point valuation framework, Medical Properties Trust scores a 5/6 valuation score. This sets up a useful comparison between methods like discounted cash flow, multiples, and asset based measures. We will also look at an approach later that many investors find even more helpful for understanding whether the price really makes sense.

Approach 1: Medical Properties Trust Discounted Cash Flow (DCF) Analysis

The Discounted Cash Flow model estimates what Medical Properties Trust could be worth by projecting its adjusted funds from operations and then discounting those future cash flows back to today in dollar terms.

For Medical Properties Trust, the model used is a 2 stage Free Cash Flow to Equity approach based on adjusted funds from operations. The latest twelve month free cash flow is a loss of $1.4b, so the model relies heavily on how cash flows might look in future years rather than recent figures.

Analysts and extrapolations indicate free cash flow of $413 million in 2030, with a series of annual projections between 2026 and 2035 that gradually move higher, all converted into present values using a discount rate. Simply Wall St only uses explicit analyst estimates where available and then extends the series mechanically after that point.

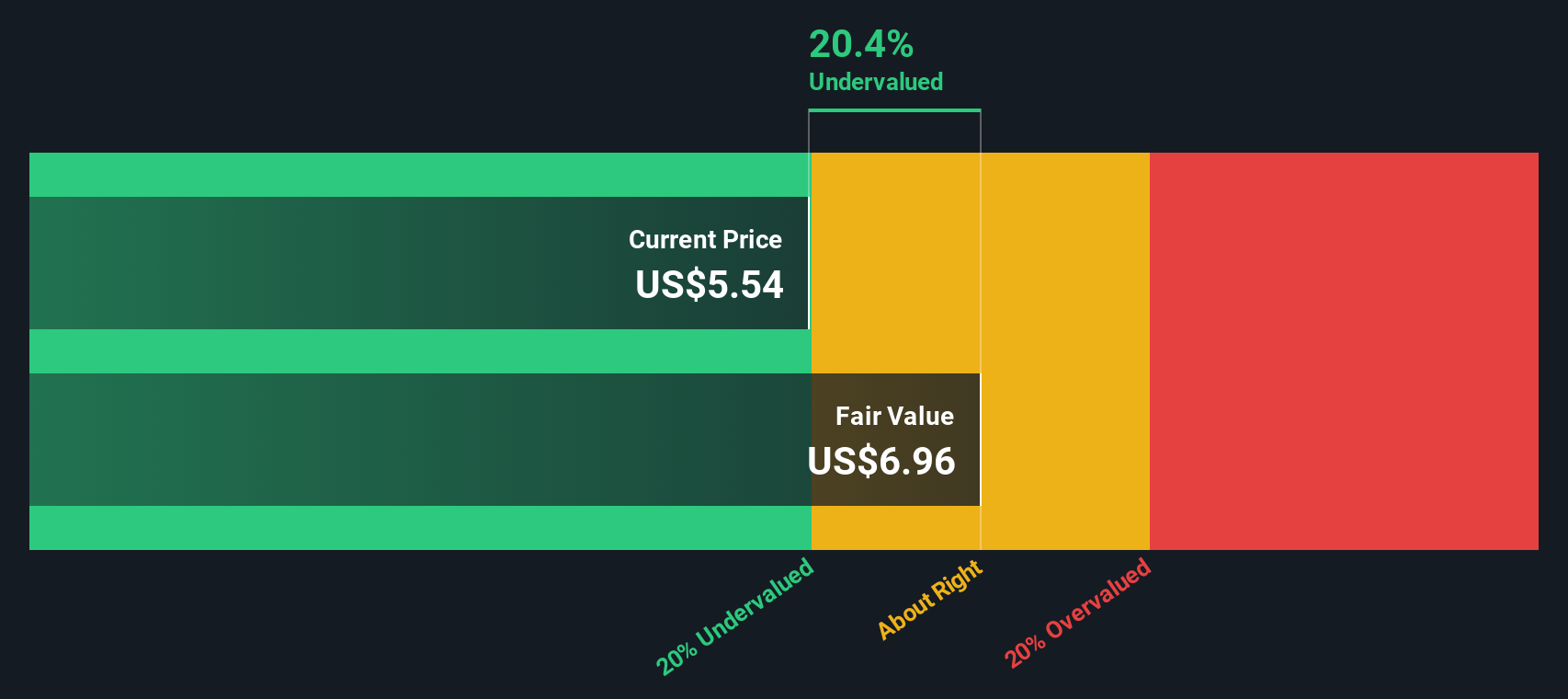

Putting those discounted cash flows together gives an estimated intrinsic value of about $6.91 per share. Compared with the recent share price of around $5.11, this DCF output suggests the stock is about 26.0% undervalued based on these assumptions.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Medical Properties Trust is undervalued by 26.0%. Track this in your watchlist or portfolio, or discover 867 more undervalued stocks based on cash flows.

Approach 2: Medical Properties Trust Price vs Sales

For companies that are not consistently profitable, the P/S ratio can be a useful way to compare what the market is paying for each dollar of revenue, rather than relying on earnings that may be volatile or negative.

Investors usually expect higher growth and lower risk to justify a higher “normal” or “fair” P/S multiple. Slower growth or higher risk tends to line up with a lower multiple, so the right range is rarely one size fits all across an industry.

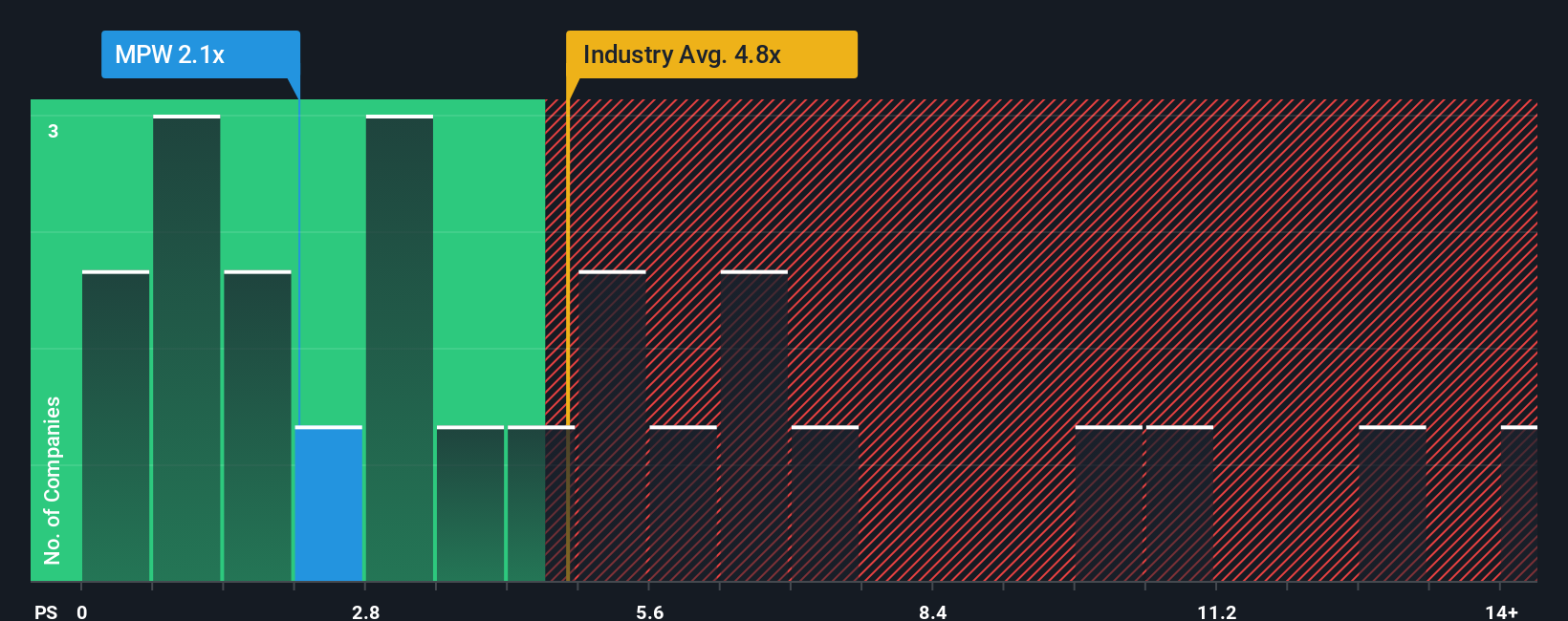

Medical Properties Trust is currently trading on a P/S of 3.05x. That sits below the Health Care REITs industry average P/S of 6.52x and the peer group average of 7.38x, which indicates the stock is priced at a discount compared with many similar names on a sales basis.

Simply Wall St’s Fair Ratio for Medical Properties Trust is 5.37x. This is a proprietary estimate of what the P/S might be, given factors such as its growth outlook, profit margins, industry, market value and risk profile. Because it is tailored to the company, it can be more informative than a simple comparison with broad industry or peer averages.

Comparing the Fair Ratio of 5.37x with the current P/S of 3.05x, Medical Properties Trust appears undervalued on this measure.

Result: UNDERVALUED

P/S ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1426 companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your Medical Properties Trust Narrative

Earlier we mentioned that there is an even better way to understand valuation, so let us introduce you to Narratives. These are simply your story about Medical Properties Trust, linked to your own forecasts for revenue, earnings and margins, and then translated into a fair value that you can easily compare with the current share price.

On Simply Wall St, Narratives sit inside the Community page, where millions of investors share their views. The platform connects each Narrative to a full financial model, so you can see how your expectations flow through to a fair value estimate and a clear buy or sell decision based on whether that value is above or below today’s price.

Narratives are updated automatically when new information arrives, such as fresh earnings or major news. This means your fair value view for Medical Properties Trust can stay aligned with the latest data rather than a static one off calculation.

For example, one investor might see Medical Properties Trust as deeply undervalued with a high fair value, while another might set a much lower fair value that is closer to the current price.

Do you think there's more to the story for Medical Properties Trust? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.