Is Twilio (TWLO) Fairly Priced After Recent Share Price Declines?

Twilio, Inc. Class A TWLO | 132.56 | +0.78% |

- If you are wondering whether Twilio's current share price reflects its underlying worth, this article will walk you through what the numbers may indicate about value.

- Twilio last closed at US$123.72, and the stock shows a mix of periods with a 2.1% decline over 7 days, a 14.2% decline over 30 days, a 10.6% decline year to date, a 16.6% decline over 1 year, an 89.0% gain over 3 years and a 69.0% decline over 5 years.

- Recent coverage around Twilio has focused on how the company is positioned within the software and communications platform space, as investors weigh its current scale against its long term ambitions. This context helps frame how the market might be reassessing the balance between potential growth and the risks that come with it.

- On Simply Wall St's valuation checks, Twilio scores 2 out of 6. Next we will look at what different valuation methods say about the stock, and then finish with a more complete way to think about valuation overall.

Twilio scores just 2/6 on our valuation checks. See what other red flags we found in the full valuation breakdown.

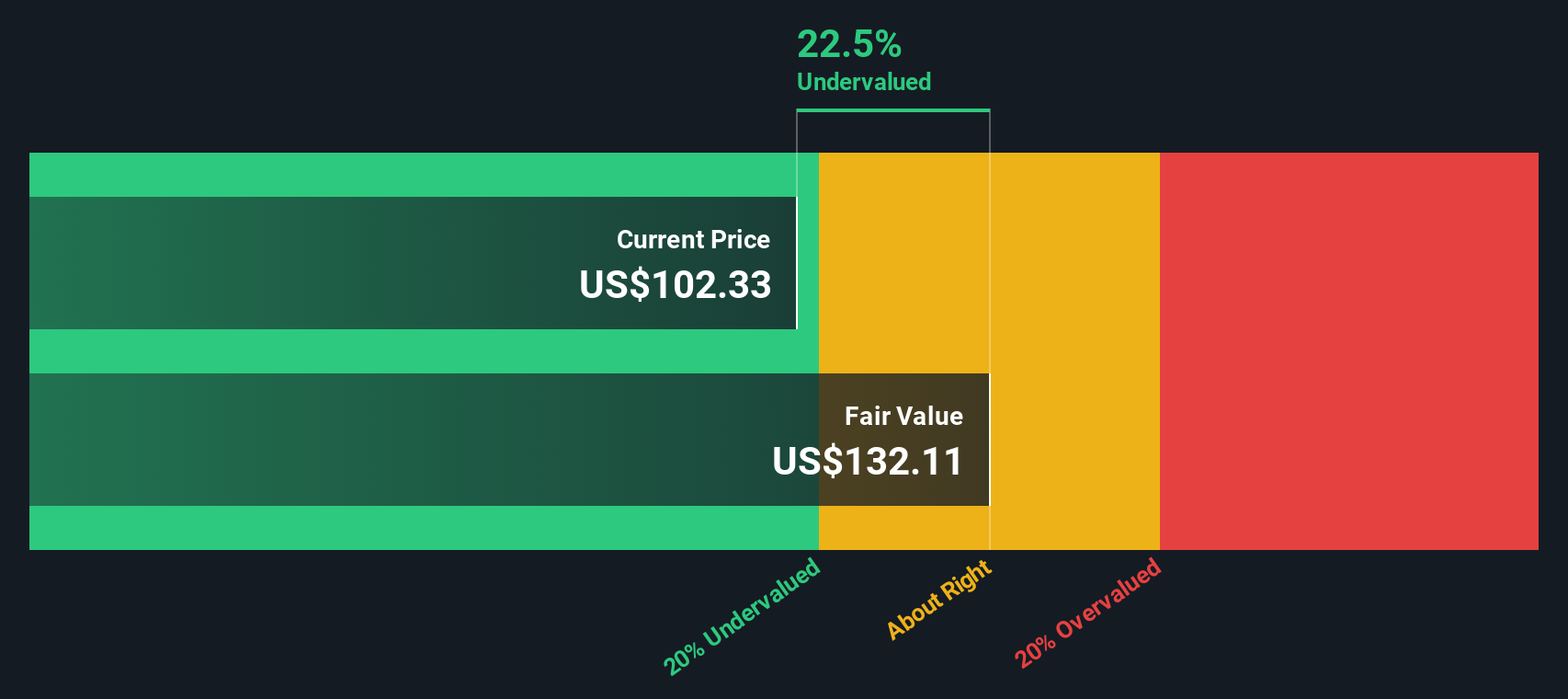

Approach 1: Twilio Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow, or DCF, model estimates what a business could be worth today by projecting its future cash flows and then discounting those back to a present value. It is essentially asking what Twilio’s future cash generation might be worth in today’s dollars.

Twilio’s latest twelve month free cash flow is reported at about $778.5 million. Using a 2 Stage Free Cash Flow to Equity model, analysts and Simply Wall St project free cash flow out over the next decade, with inputs such as $1,033.1 million in 2026 and $1,220 million in 2030, all in $. Beyond the explicit analyst years, later cash flows are extrapolated by Simply Wall St using modest growth assumptions.

When all these projected cash flows are discounted back, the model arrives at an estimated intrinsic value of about $119.81 per share. Compared with a recent share price of $123.72, this implies Twilio is about 3.3% overvalued, which is a relatively small gap and within a reasonable margin of error for any model based on projections.

Result: ABOUT RIGHT

Twilio is fairly valued according to our Discounted Cash Flow (DCF), but this can change at a moment's notice. Track the value in your watchlist or portfolio and be alerted on when to act.

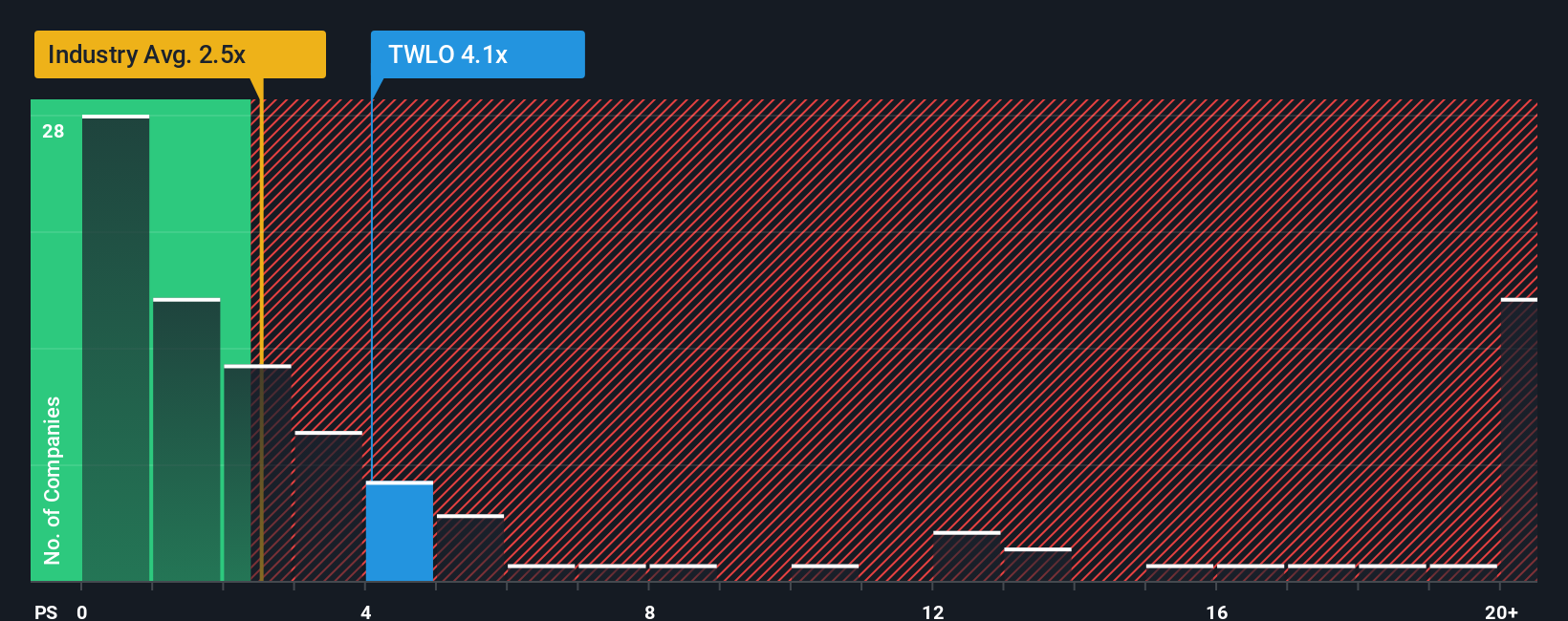

Approach 2: Twilio Price vs Sales

For a company like Twilio, where investors often focus on revenue scale and monetization potential, the P/S multiple can be a useful way to think about value. It links what you pay for the stock to the sales the business is already generating, which is especially relevant when earnings are less of a focus.

What counts as a “normal” P/S partly depends on how quickly investors expect revenue to grow and how much risk they see in those expectations. Higher growth or lower perceived risk can justify a higher multiple, while slower growth or higher uncertainty usually points to a lower one.

Twilio currently trades on a P/S of 3.83x. That sits above the broader IT industry average of 2.23x, but below the peer group average of 6.37x. Simply Wall St also calculates a “Fair Ratio” of 4.69x, which is its proprietary view of what P/S might be reasonable once you factor in Twilio’s growth profile, margins, size and risk characteristics. This Fair Ratio can be more informative than a plain industry or peer comparison because it is tailored to the company rather than a broad group.

With Twilio’s actual 3.83x P/S sitting below the 4.69x Fair Ratio, the stock appears undervalued on this metric.

Result: UNDERVALUED

P/S ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1414 companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your Twilio Narrative

Earlier we mentioned that there is an even better way to understand valuation, so let us introduce you to Narratives, which are simply your story about a company, linked directly to your own forecast for future revenue, earnings and margins, and then to your view of fair value.

On Simply Wall St, Narratives live in the Community page and are designed to be quick and accessible. You set a few key assumptions, the platform turns that into a financial forecast and fair value, then you can compare that fair value to the current price to help decide whether Twilio looks attractive, fairly priced or expensive to you.

Narratives are not static. They automatically refresh when new data arrives, such as earnings releases or major news, so your story and numbers stay aligned without you needing to rebuild a spreadsheet.

For Twilio, one investor might enter assumptions that lead to a much lower fair value, while another uses more optimistic revenue and margin estimates that support a much higher figure, and seeing these side by side can help you decide which story you find more reasonable.

Do you think there's more to the story for Twilio? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.