Please use a PC Browser to access Register-Tadawul

Get It

Knightscope (NASDAQ:KSCP) Has Debt But No Earnings; Should You Worry?

Knightscope, Inc. Class A KSCP | 3.32 | -0.60% |

Some say volatility, rather than debt, is the best way to think about risk as an investor, but Warren Buffett famously said that 'Volatility is far from synonymous with risk.' So it seems the smart money knows that debt - which is usually involved in bankruptcies - is a very important factor, when you assess how risky a company is. We note that Knightscope, Inc. (NASDAQ:KSCP) does have debt on its balance sheet. But is this debt a concern to shareholders?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. In the worst case scenario, a company can go bankrupt if it cannot pay its creditors. While that is not too common, we often do see indebted companies permanently diluting shareholders because lenders force them to raise capital at a distressed price. By replacing dilution, though, debt can be an extremely good tool for businesses that need capital to invest in growth at high rates of return. When we think about a company's use of debt, we first look at cash and debt together.

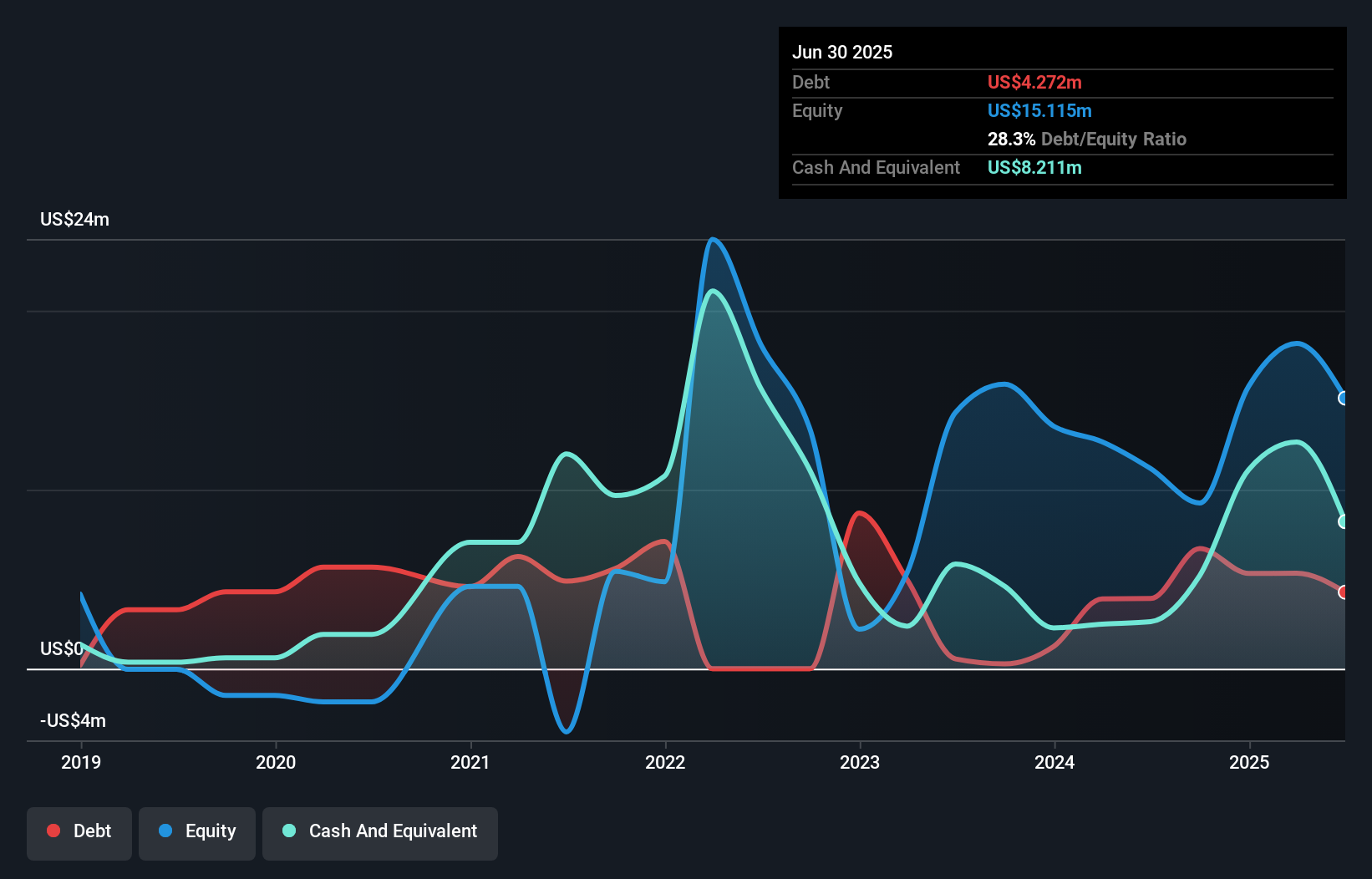

As you can see below, at the end of June 2025, Knightscope had US$4.27m of debt, up from US$3.92m a year ago. Click the image for more detail. But on the other hand it also has US$8.21m in cash, leading to a US$3.94m net cash position.

According to the last reported balance sheet, Knightscope had liabilities of US$7.01m due within 12 months, and liabilities of US$7.09m due beyond 12 months. On the other hand, it had cash of US$8.21m and US$2.49m worth of receivables due within a year. So its liabilities total US$3.40m more than the combination of its cash and short-term receivables.

Given Knightscope has a market capitalization of US$60.3m, it's hard to believe these liabilities pose much threat. However, we do think it is worth keeping an eye on its balance sheet strength, as it may change over time. While it does have liabilities worth noting, Knightscope also has more cash than debt, so we're pretty confident it can manage its debt safely. When analysing debt levels, the balance sheet is the obvious place to start. But it is future earnings, more than anything, that will determine Knightscope's ability to maintain a healthy balance sheet going forward. So if you want to see what the professionals think, you might find this free report on analyst profit forecasts to be interesting.

Over 12 months, Knightscope made a loss at the EBIT level, and saw its revenue drop to US$11m, which is a fall of 6.6%. We would much prefer see growth.

We have no doubt that loss making companies are, in general, riskier than profitable ones. And in the last year Knightscope had an earnings before interest and tax (EBIT) loss, truth be told. And over the same period it saw negative free cash outflow of US$24m and booked a US$31m accounting loss. With only US$3.94m on the balance sheet, it would appear that its going to need to raise capital again soon. Overall, we'd say the stock is a bit risky, and we're usually very cautious until we see positive free cash flow. The balance sheet is clearly the area to focus on when you are analysing debt. But ultimately, every company can contain risks that exist outside of the balance sheet. These risks can be hard to spot.

If, after all that, you're more interested in a fast growing company with a rock-solid balance sheet, then check out our list of net cash growth stocks without delay.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.