Please use a PC Browser to access Register-Tadawul

Get It

Liberty Energy (LBRT) Margin Compression To 3.7% Reinforces Bearish Earnings Narratives

Liberty Energy, Inc. Class A LBRT | 26.85 | -0.15% |

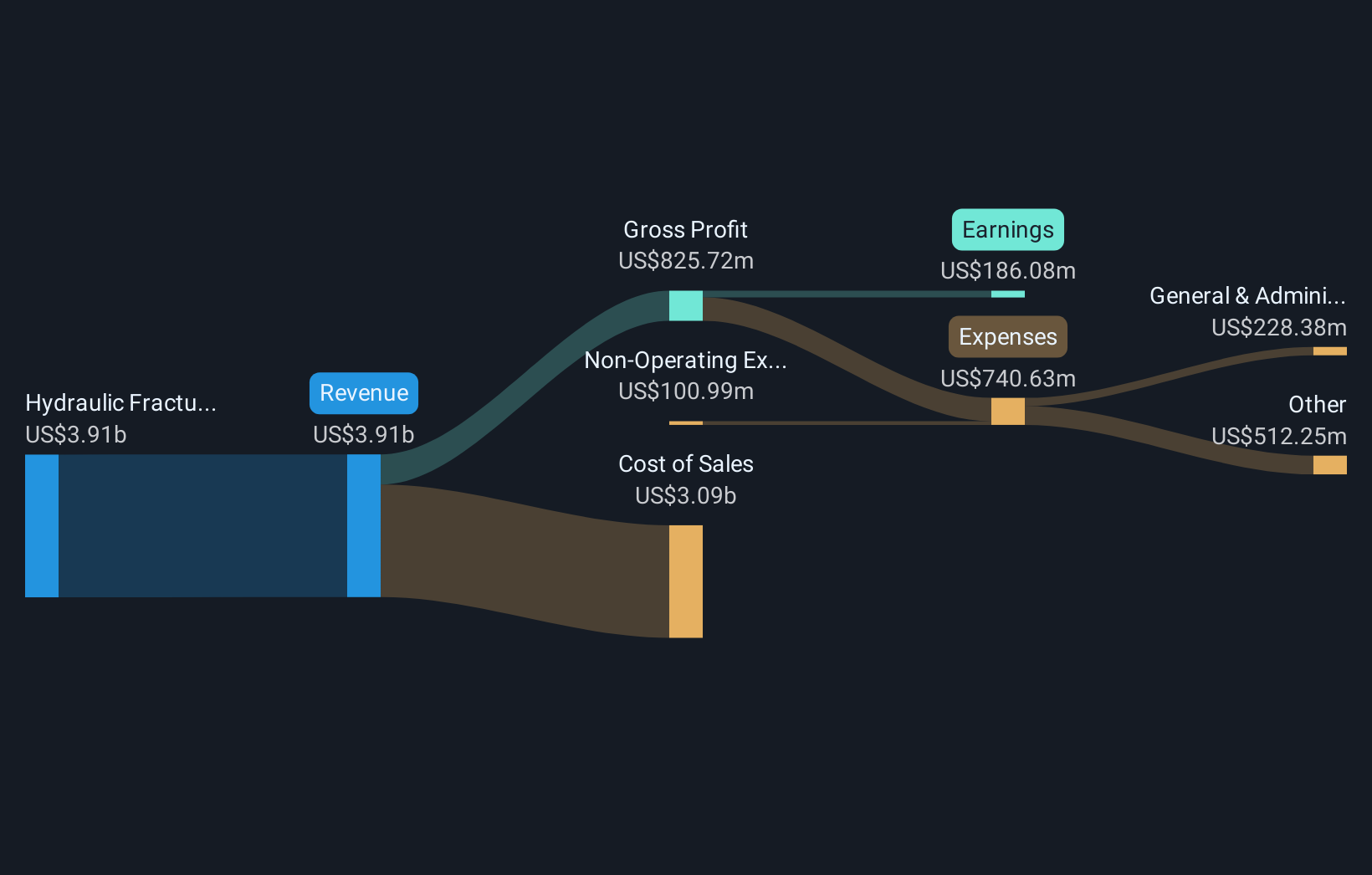

Liberty Energy (LBRT) closed out FY 2025 with Q4 revenue of US$1.0b and basic EPS of US$0.08, alongside net income of US$13.7m, while the trailing twelve months show EPS of US$0.91 on revenue of US$4.0b and net income of US$147.9m. Over recent quarters, revenue has moved between US$947.4m and US$1.0b, with quarterly EPS ranging from US$0.08 to US$0.44, giving investors a clear picture of how earnings have tracked against a relatively steady top line. With the shares at US$25.34, the focus now is on how these results fit with expectations around margins, cash generation, and the durability of the current profit profile.

See our full analysis for Liberty Energy.With the latest numbers on the table, the next step is to set them against the most followed narratives around Liberty Energy’s earnings power, margin resilience, and potential growth to see which views hold up and which might need rethinking.

Don't just look at this quarter; the real story is in the long-term trend. We've done an in-depth analysis on Liberty Energy's growth and its valuation to see if today's price is a bargain. Add the company to your watchlist or portfolio now so you don't miss the next big move.

Liberty Energy’s earnings story leans on a US$145.1m one off gain and thinner 3.7% margins, while consensus points to yearly earnings decline ahead.

If you want ideas with a clearer earnings path and fewer one offs, check out CTA_SCREENER_STABLE_GROWTH to focus on companies built around steadier growth profiles.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.