Please use a PC Browser to access Register-Tadawul

Get It

Moderna, Inc.'s (NASDAQ:MRNA) Price Is Right But Growth Is Lacking After Shares Rocket 26%

Moderna MRNA | 27.97 27.87 | +0.97% -0.35% Post |

Moderna, Inc. (NASDAQ:MRNA) shareholders have had their patience rewarded with a 26% share price jump in the last month. Still, the 30-day jump doesn't change the fact that longer term shareholders have seen their stock decimated by the 73% share price drop in the last twelve months.

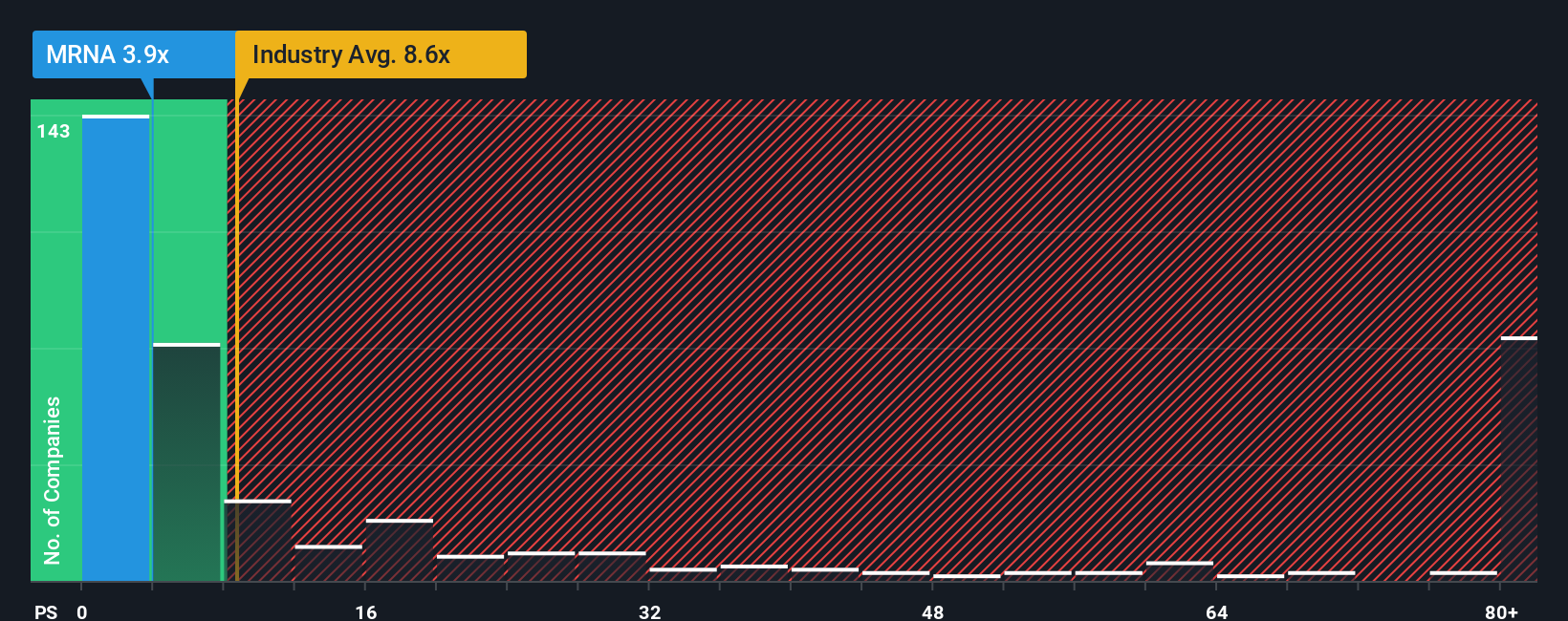

In spite of the firm bounce in price, Moderna may still look like a strong buying opportunity at present with its price-to-sales (or "P/S") ratio of 3.9x, considering almost half of all companies in the Biotechs industry in the United States have P/S ratios greater than 8.6x and even P/S higher than 61x aren't out of the ordinary. Nonetheless, we'd need to dig a little deeper to determine if there is a rational basis for the highly reduced P/S.

Moderna could be doing better as its revenue has been going backwards lately while most other companies have been seeing positive revenue growth. Perhaps the P/S remains low as investors think the prospects of strong revenue growth aren't on the horizon. If this is the case, then existing shareholders will probably struggle to get excited about the future direction of the share price.

Want the full picture on analyst estimates for the company? Then our free report on Moderna will help you uncover what's on the horizon.There's an inherent assumption that a company should far underperform the industry for P/S ratios like Moderna's to be considered reasonable.

Retrospectively, the last year delivered a frustrating 38% decrease to the company's top line. This means it has also seen a slide in revenue over the longer-term as revenue is down 86% in total over the last three years. Therefore, it's fair to say the revenue growth recently has been undesirable for the company.

Shifting to the future, estimates from the analysts covering the company suggest revenue should grow by 1.8% per year over the next three years. With the industry predicted to deliver 103% growth per annum, the company is positioned for a weaker revenue result.

With this information, we can see why Moderna is trading at a P/S lower than the industry. Apparently many shareholders weren't comfortable holding on while the company is potentially eyeing a less prosperous future.

Moderna's recent share price jump still sees fails to bring its P/S alongside the industry median. It's argued the price-to-sales ratio is an inferior measure of value within certain industries, but it can be a powerful business sentiment indicator.

We've established that Moderna maintains its low P/S on the weakness of its forecast growth being lower than the wider industry, as expected. Right now shareholders are accepting the low P/S as they concede future revenue probably won't provide any pleasant surprises. The company will need a change of fortune to justify the P/S rising higher in the future.

A lot of potential risks can sit within a company's balance sheet. Take a look at our free balance sheet analysis for Moderna with six simple checks on some of these key factors.

It's important to make sure you look for a great company, not just the first idea you come across. So if growing profitability aligns with your idea of a great company, take a peek at this free list of interesting companies with strong recent earnings growth (and a low P/E).

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.