Please use a PC Browser to access Register-Tadawul

Get It

Natural Resource Partners (NRP) Valuation Check After Recent Unit Price Gains And DCF Discount

Natural Resource Partners L.P. NRP | 124.20 | +0.52% |

Natural Resource Partners (NRP) has drawn attention after recent gains, with the unit price closing at US$123.04 and positive total returns over the past month, past 3 months, and year.

For investors following income oriented partnerships and mineral rights businesses, those returns, combined with reported revenue of US$218.701 million and net income of US$145.179 million, raise questions about how the market is currently valuing NRP’s portfolio.

NRP’s recent 1-day share price return of 2.20% and 30-day share price return of 12.50% sit alongside a 1-year total shareholder return of 24.90% and a very large 5-year total shareholder return. This combination suggests momentum has been building over multiple periods as investors reassess risk and income potential around its mineral rights portfolio.

If NRP’s run has you thinking about where else value might be hiding, it could be worth scanning our screener of 30 best rare earth metal stocks as another way to look at resource exposure.

With NRP trading at US$123.04 and an estimated intrinsic discount of about 47%, the key question for you is whether this mineral rights partnership still offers mispriced value, or if the market is already factoring in future growth.

On a P/E of 11.1x at a unit price of $123.04, Natural Resource Partners screens cheaper than both its US Oil and Gas industry group at 14.1x and its direct peer set at 22.5x.

The P/E ratio simply shows how much investors are paying today for each dollar of earnings. This is especially relevant for a partnership like NRP that already generates profits and royalty income rather than relying solely on undeveloped assets.

Here, the current P/E sits well below both the sector and peer averages. This suggests the market is valuing NRP’s earnings at a discount compared with similar companies, even though the business has high quality earnings and a Return on Equity of 24.2%.

Against peers on 22.5x and the wider US Oil and Gas industry at 14.1x, NRP’s 11.1x multiple is materially lower. In other words, the market is assigning a more conservative price tag to its earnings than it does to comparable businesses.

Result: Price-to-Earnings of 11.1x (UNDERVALUED)

However, you also need to weigh exposure to coal focused mineral rights and commodity price swings, which could quickly change how attractive today’s earnings multiple looks.

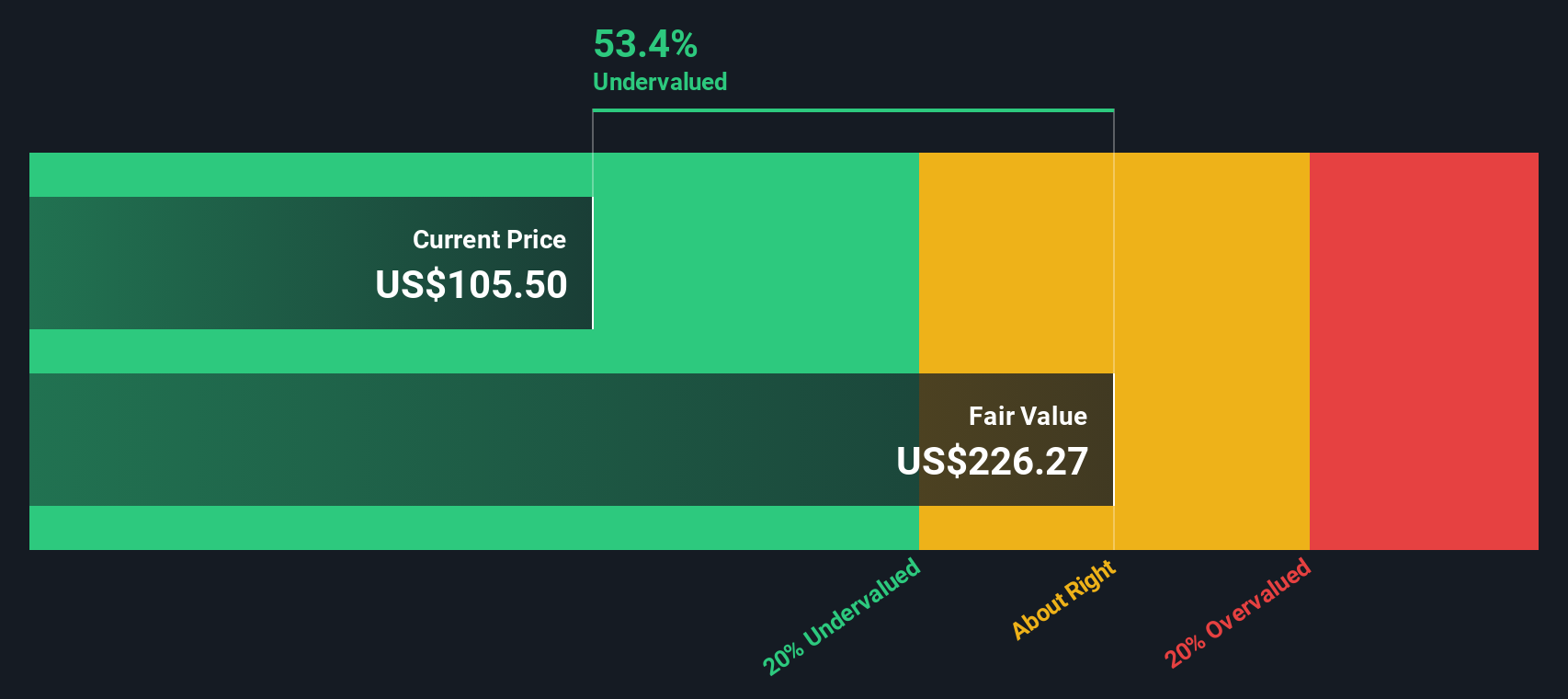

While the 11.1x P/E hints at a discount, our DCF model points to something more pronounced. With NRP at $123.04 and our future cash flow value estimate at $233.79, the units screen as undervalued using this second lens.

That gap raises a practical question for you: is the market being cautious about future cash flows, or is there a margin of safety that income focused investors might be overlooking?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Natural Resource Partners for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 52 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

If you see the numbers differently or prefer to test your own assumptions, you can quickly build a custom story around NRP, starting with Do it your way.

A great starting point for your Natural Resource Partners research is our analysis highlighting 1 key reward and 1 important warning sign that could impact your investment decision.

If NRP has sharpened your focus, do not stop here. Use the Simply Wall St screener to uncover other opportunities that could suit your portfolio.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.