Please use a PC Browser to access Register-Tadawul

Get It

Slowing Rates Of Return At Forrester Research (NASDAQ:FORR) Leave Little Room For Excitement

Forrester Research, Inc. FORR | 8.18 | -1.68% |

To find a multi-bagger stock, what are the underlying trends we should look for in a business? Ideally, a business will show two trends; firstly a growing return on capital employed (ROCE) and secondly, an increasing amount of capital employed. Put simply, these types of businesses are compounding machines, meaning they are continually reinvesting their earnings at ever-higher rates of return. Having said that, from a first glance at Forrester Research (NASDAQ:FORR) we aren't jumping out of our chairs at how returns are trending, but let's have a deeper look.

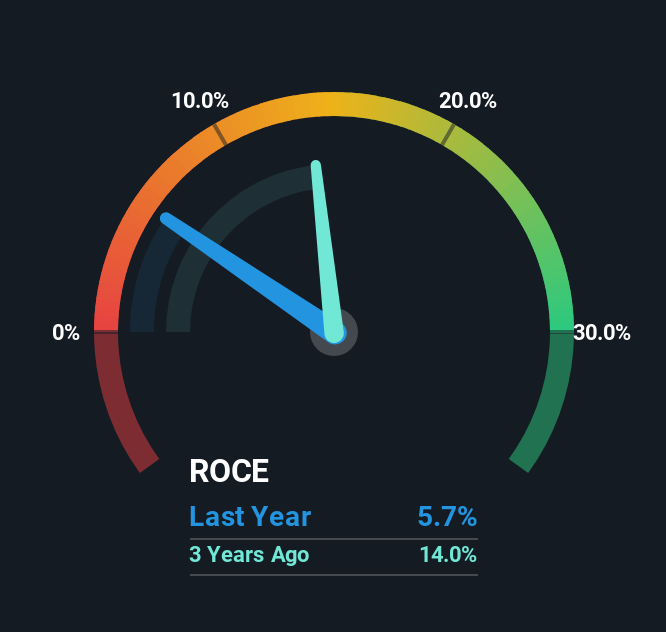

Just to clarify if you're unsure, ROCE is a metric for evaluating how much pre-tax income (in percentage terms) a company earns on the capital invested in its business. To calculate this metric for Forrester Research, this is the formula:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

0.057 = US$13m ÷ (US$414m - US$182m) (Based on the trailing twelve months to September 2025).

Therefore, Forrester Research has an ROCE of 5.7%. In absolute terms, that's a low return and it also under-performs the Professional Services industry average of 16%.

Above you can see how the current ROCE for Forrester Research compares to its prior returns on capital, but there's only so much you can tell from the past. If you're interested, you can view the analysts predictions in our free analyst report for Forrester Research .

We've noticed that although returns on capital are flat over the last five years, the amount of capital employed in the business has fallen 37% in that same period. When a company effectively decreases its assets base, it's not usually a sign to be optimistic on that company. Not only that, but the low returns on this capital mentioned earlier would leave most investors unimpressed.

On a side note, Forrester Research's current liabilities are still rather high at 44% of total assets. This can bring about some risks because the company is basically operating with a rather large reliance on its suppliers or other sorts of short-term creditors. Ideally we'd like to see this reduce as that would mean fewer obligations bearing risks.

In summary, Forrester Research isn't reinvesting funds back into the business and returns aren't growing. And investors may be expecting the fundamentals to get a lot worse because the stock has crashed 82% over the last five years. On the whole, we aren't too inspired by the underlying trends and we think there may be better chances of finding a multi-bagger elsewhere.

While Forrester Research doesn't shine too bright in this respect, it's still worth seeing if the company is trading at attractive prices. You can find that out with our FREE intrinsic value estimation for FORR on our platform.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.