Please use a PC Browser to access Register-Tadawul

Get It

The Returns On Capital At Weis Markets (NYSE:WMK) Don't Inspire Confidence

Weis Markets, Inc. WMK | 74.42 | +0.76% |

When it comes to investing, there are some useful financial metrics that can warn us when a business is potentially in trouble. A business that's potentially in decline often shows two trends, a return on capital employed (ROCE) that's declining, and a base of capital employed that's also declining. Trends like this ultimately mean the business is reducing its investments and also earning less on what it has invested. In light of that, from a first glance at Weis Markets (NYSE:WMK), we've spotted some signs that it could be struggling, so let's investigate.

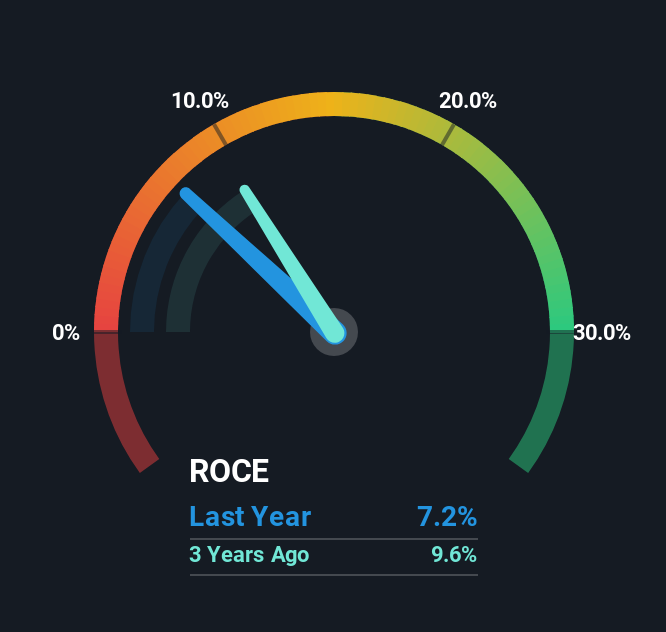

Just to clarify if you're unsure, ROCE is a metric for evaluating how much pre-tax income (in percentage terms) a company earns on the capital invested in its business. To calculate this metric for Weis Markets, this is the formula:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

0.072 = US$120m ÷ (US$2.0b - US$351m) (Based on the trailing twelve months to September 2025).

Thus, Weis Markets has an ROCE of 7.2%. Ultimately, that's a low return and it under-performs the Consumer Retailing industry average of 12%.

While the past is not representative of the future, it can be helpful to know how a company has performed historically, which is why we have this chart above. If you'd like to look at how Weis Markets has performed in the past in other metrics, you can view this free graph of Weis Markets' past earnings, revenue and cash flow.

There is reason to be cautious about Weis Markets, given the returns are trending downwards. Unfortunately the returns on capital have diminished from the 11% that they were earning five years ago. On top of that, it's worth noting that the amount of capital employed within the business has remained relatively steady. Since returns are falling and the business has the same amount of assets employed, this can suggest it's a mature business that hasn't had much growth in the last five years. If these trends continue, we wouldn't expect Weis Markets to turn into a multi-bagger.

In the end, the trend of lower returns on the same amount of capital isn't typically an indication that we're looking at a growth stock. Yet despite these concerning fundamentals, the stock has performed strongly with a 46% return over the last five years, so investors appear very optimistic. Regardless, we don't feel too comfortable with the fundamentals so we'd be steering clear of this stock for now.

If you'd like to know more about Weis Markets, we've spotted 2 warning signs, and 1 of them is a bit unpleasant.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.