Please use a PC Browser to access Register-Tadawul

Get It

There's No Escaping AVITA Medical, Inc.'s (NASDAQ:RCEL) Muted Revenues Despite A 26% Share Price Rise

AVITA Medical Inc RCEL | 4.79 | +9.36% |

AVITA Medical, Inc. (NASDAQ:RCEL) shareholders would be excited to see that the share price has had a great month, posting a 26% gain and recovering from prior weakness. Still, the 30-day jump doesn't change the fact that longer term shareholders have seen their stock decimated by the 52% share price drop in the last twelve months.

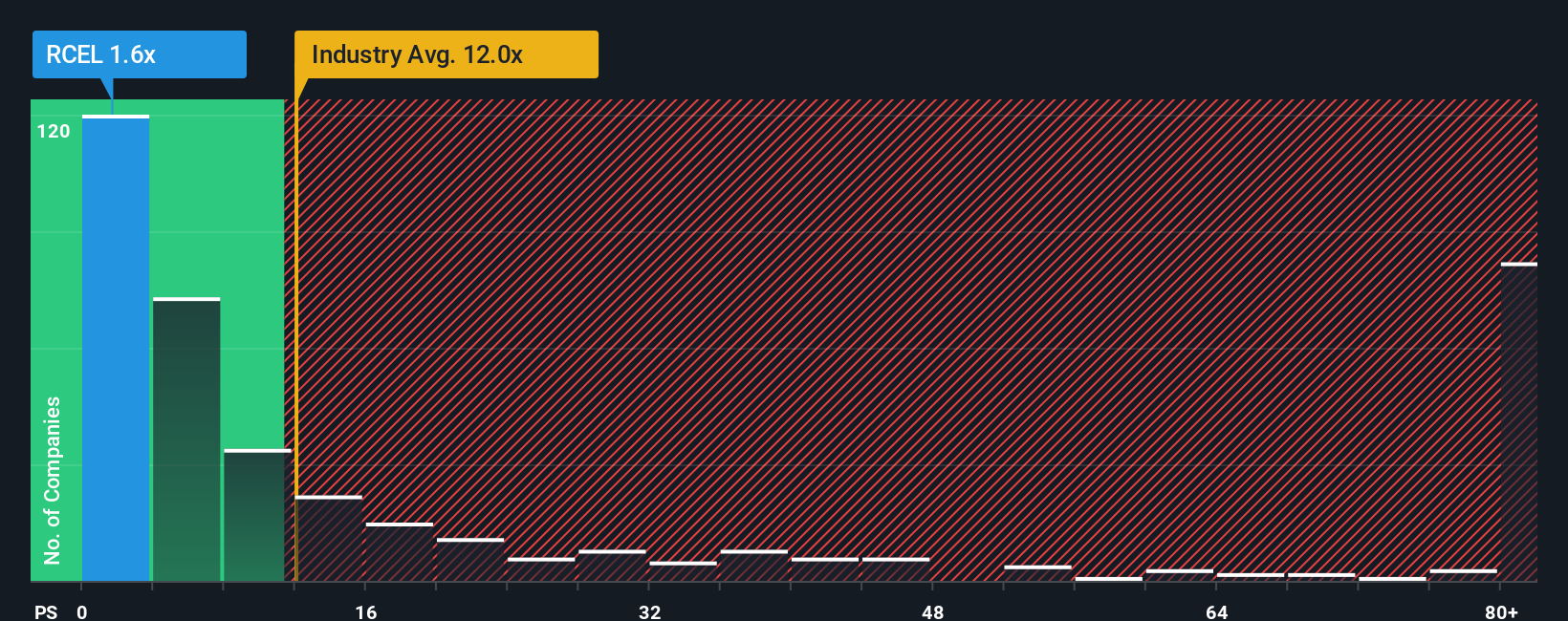

Although its price has surged higher, AVITA Medical may still be sending very bullish signals at the moment with its price-to-sales (or "P/S") ratio of 1.9x, since almost half of all companies in the Biotechs industry in the United States have P/S ratios greater than 11.9x and even P/S higher than 78x are not unusual. Although, it's not wise to just take the P/S at face value as there may be an explanation why it's so limited.

Recent times haven't been great for AVITA Medical as its revenue has been rising slower than most other companies. Perhaps the market is expecting the current trend of poor revenue growth to continue, which has kept the P/S suppressed. If you still like the company, you'd be hoping revenue doesn't get any worse and that you could pick up some stock while it's out of favour.

Keen to find out how analysts think AVITA Medical's future stacks up against the industry? In that case, our free report is a great place to start.The only time you'd be truly comfortable seeing a P/S as depressed as AVITA Medical's is when the company's growth is on track to lag the industry decidedly.

Retrospectively, the last year delivered an exceptional 21% gain to the company's top line. The strong recent performance means it was also able to grow revenue by 127% in total over the last three years. So we can start by confirming that the company has done a great job of growing revenue over that time.

Looking ahead now, revenue is anticipated to climb by 43% per year during the coming three years according to the ten analysts following the company. Meanwhile, the rest of the industry is forecast to expand by 132% per year, which is noticeably more attractive.

With this information, we can see why AVITA Medical is trading at a P/S lower than the industry. It seems most investors are expecting to see limited future growth and are only willing to pay a reduced amount for the stock.

Shares in AVITA Medical have risen appreciably however, its P/S is still subdued. While the price-to-sales ratio shouldn't be the defining factor in whether you buy a stock or not, it's quite a capable barometer of revenue expectations.

As we suspected, our examination of AVITA Medical's analyst forecasts revealed that its inferior revenue outlook is contributing to its low P/S. At this stage investors feel the potential for an improvement in revenue isn't great enough to justify a higher P/S ratio. The company will need a change of fortune to justify the P/S rising higher in the future.

If these risks are making you reconsider your opinion on AVITA Medical, explore our interactive list of high quality stocks to get an idea of what else is out there.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.