Please use a PC Browser to access Register-Tadawul

Get It

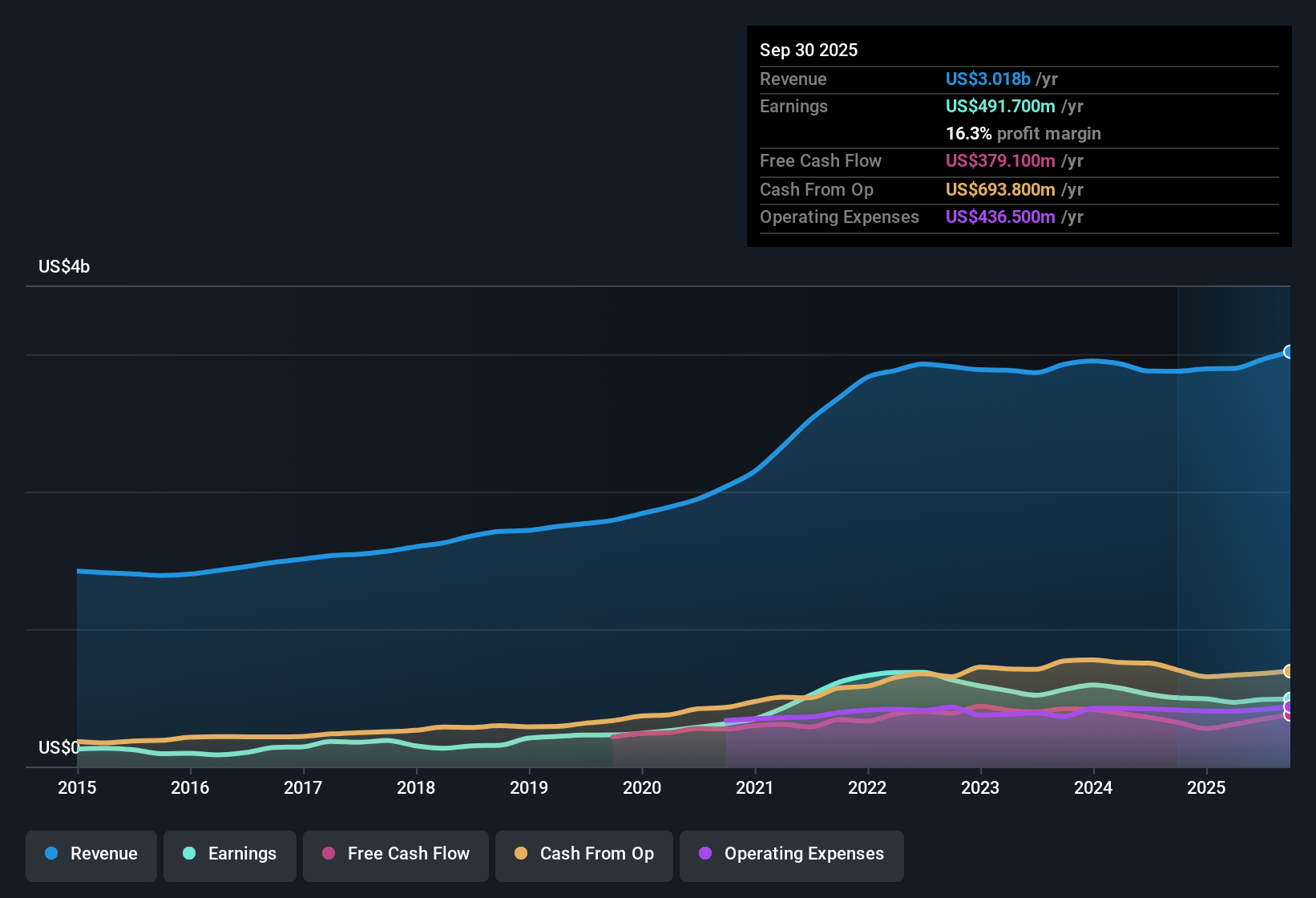

West Pharmaceutical Services Margins Slip To 16.3% Raising Questions Around Bullish Growth Narratives

West Pharmaceutical Services, Inc. WST | 245.86 | +0.62% |

West Pharmaceutical Services (WST) just posted its FY 2025 third quarter scorecard, with revenue of US$804.6 million and basic EPS of US$1.94 setting the tone for the latest update. The company has seen revenue move from US$702.1 million in Q2 2024 to US$804.6 million in Q3 2025, while basic EPS has ranged from US$1.52 in Q2 2024 to US$1.94 in the latest quarter. This gives investors a clearer view of how the top line and per share earnings have tracked through the last six reported periods as they weigh the outlook for margins and potential future growth drivers.

See our full analysis for West Pharmaceutical Services.With the headline numbers on the table, the next step is to see how this earnings print lines up with the widely followed narratives about West Pharmaceutical Services, highlighting where the data supports the story and where it challenges it.

To see how these results tie into long-term growth, risks, and valuation, check out the full range of community narratives for West Pharmaceutical Services on Simply Wall St. Add the company to your watchlist or portfolio so you'll be alerted when the story evolves.

See the numbers differently? Take a couple of minutes to test your own view against the figures and turn that into a clear narrative of your own, Do it your way.

A good starting point is our analysis highlighting 2 key rewards investors are optimistic about regarding West Pharmaceutical Services.

West Pharmaceutical Services is contending with softer margins, modest 6% revenue growth versus the broader market, and a rich 35.6x P/E that sits well above its DCF fair value.

If that mix of slower growth and a valuation gap worries you, shift your focus toward companies trading closer to their fundamentals using our 55 high quality undervalued stocks today.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.