We Value Your Feedback! Help us shape better content and experiences by participating in our survey. Join the Survey Now!

Company Overview:

United Carton Industries (UCIC), a prominent Saudi-based provider of corrugated paper packaging solutions, positions itself as a “one-stop service” manufacturer. It is deeply involved in Saudi Arabia’s “Vision 2030” and benefits from the expansion of local manufacturing and the trend of import substitution.

UCIC boasts core strengths, including vertically integrated production capacity, diversified customer coverage (across various industries such as food, electronics, and pharmaceuticals), and a commitment to sustainable packaging. However, as a private company, its financial transparency is somewhat limited. It also faces risks, such as fluctuations in raw material prices and intensifying regional competition. In terms of business overview, UCIC’s core business lies in the design, production, and sale of high-quality corrugated cardboard and packaging solutions (including boxes, display stands, and custom designs). Its key assets include advanced manufacturing facilities (with emphasis on automation and production capacity on its official website), an integrated production chain (from cardboard to finished packaging), and strong R&D and design capabilities (providing customized solutions).

The company mainly focuses on the domestic Saudi market, with potential to expand to the Gulf Cooperation Council (GCC) region. Its end customers cover key economic sectors such as food and beverage, home appliances, pharmaceuticals, e-commerce logistics and industrial products. In terms of industry analysis and market positioning, several growth drivers are present. Saudi Arabia’s “Vision 2030” stimulates packaging demand through localizing manufacturing, constructing logistics hubs and developing non - oil economy. The booming e - e-commerce sector in Saudi Arabia and the Middle East is driving the growth of transportation packaging. The consumption upgrade is increasing demand from brand owners for high-quality, branded, and shelf-appealing retail display packaging. The sustainable transformation, with stricter environmental regulations and brand commitments, is boosting the demand for recyclable packaging (with corrugated paper as the core).

Industry analysis:

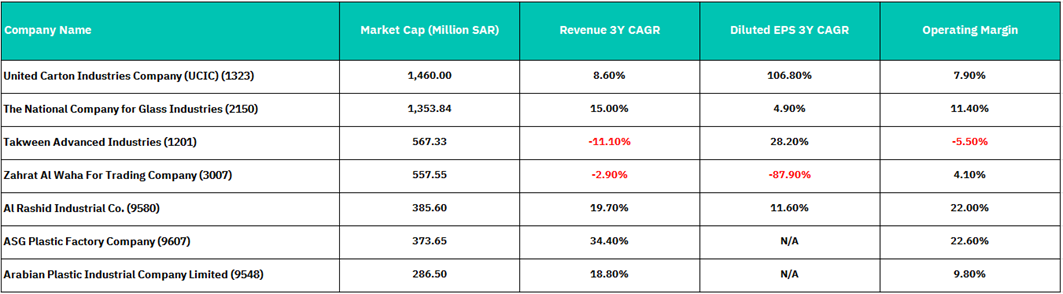

UCIC maintains a dominant market position within the Saudi Arabian packaging and industrial materials sector, evidenced by its leading market capitalization of SAR 1,460 million. This prominence signifies robust investor confidence and provides significant advantages in terms of financial stability, access to capital markets, and enhanced bargaining power with suppliers and customers. While the competitive landscape includes specialized packaging firms (glass, plastic, carton) and diversified industrial manufacturers, UCIC's scale positions it as the benchmark entity. The industry benefits from inherent resilience due to consistent demand drivers across consumer goods, pharmaceuticals, and e-commerce logistics, partially insulating players from economic cyclicality. UCIC's core focus on carton packaging leverages essential goods demand and the structural growth of e-commerce fulfillment.

UCIC exhibits a performance profile characterized by solid, steady revenue expansion but exceptional profit conversion. Its 3-year revenue CAGR of 8.60% reflects consistent top-line growth; however, this pace is notably exceeded by several competitors, particularly within the plastic packaging segment (e.g., ASG Plastic at 34.40%, Al Rashid Industrial at 19.70%, Arabian Plastic at 18.80%, National Glass at 15.00%). The defining strength of UCIC lies in its remarkable profitability trajectory. A diluted EPS 3-year CAGR of 106.80% vastly outpaces its revenue growth and industry peers, signaling extraordinary operational efficiency improvements, effective cost management, and strong pricing power. This profit surge occurs despite UCIC's operating margin (7.90%) being moderate within the peer group, positioned above Zahrat Al Waha (4.10%) and Takween Advanced Industries (-5.50%), but below higher-margin plastic players like ASG Plastic (22.60%) and Al Rashid Industrial (22.00%).

UCIC's key competitive advantages stem from its market leadership, significant scale, and demonstrated ability to translate revenue into exceptional earnings growth. Its strong financial profile provides stability and flexibility absent in weaker competitors experiencing volatility or decline. Strategically, UCIC faces the imperative to accelerate revenue growth to match its stellar profitability performance. Opportunities exist in emulating successful strategies from faster-growing plastic packaging competitors, potentially through organic expansion into adjacent high-growth plastic segments or targeted acquisitions. Further margin enhancement towards the levels achieved by leading plastic manufacturers (20%+) represents another key lever, achievable through continued operational optimization, product mix enrichment, or vertical integration. UCIC's robust balance sheet and market position uniquely equip it to pursue industry consolidation, acquiring specialized capabilities or market share from underperforming peers like Takween or Zahrat Al Waha, thereby strengthening its overall market position and diversifying its revenue streams across packaging substrates.

Valuation:

Balance Sheet Analysis

Current Assets Analysis:

Current assets showed volatility, peaking at 488M Saudi Riyal in FY2022, dropping to 447M Saudi Riyal in FY2023, then recovering to 500M Saudi Riyal in FY2024. This 12% recovery in FY2024 suggests improved working capital management and potentially a stronger cash position. The current asset composition likely includes cash, accounts receivable, and inventory, and the recovery because of either improved collections, better inventory turnover, or stronger cash generation.

Non-Current Assets Growth:

Steady growth from 386M Saudi Riyal to 497M (+28.9%) because of significant capital investments in property. This suggests UCIC is investing in future growth capacity, which is positive for long-term value creation but requires monitoring of the return on these investments.

Liability Structure Evolution:

Current liabilities remained relatively stable around 340-400M Saudi Riyal range, but the 88% increase in non-current liabilities from 59M Saudi Riyal to 110M Saudi Riyal is significant. This could indicate new long-term debt financing for expansion projects, which need to be evaluated against the returns generated from these investments.

Capital Structure Optimization:

The debt-to-equity ratio of 0.83x in FY2024 is within reasonable bounds for most industries, but the trend from 1.06x in FY2021 to 0.83x shows improving capital structure. The company is building equity faster than taking on debt, which is positive for financial stability.

Income Statement Analysis

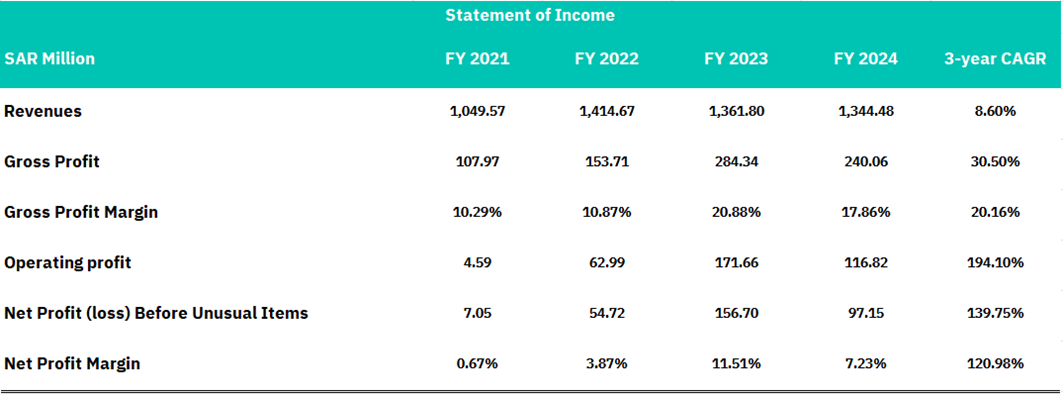

United Carton Industries (UCIC) demonstrates a robust fundamental transformation, evidenced by exceptional multi-year profitability expansion. Revenue grew at a solid 8.6% 3-year CAGR, reaching SAR 1.34 billion in FY2024, while exhibiting significant operational leverage: Gross Profit surged at a 30.5% CAGR, Operating Profit at 194.1% CAGR, and Net Profit Before Unusual Items at 139.75% CAGR. This translated into substantial margin expansion, with Gross Margin rising 751 basis points (bps), Operating Margin increasing 825 bps, and Net Margin improving 656 bps from FY2021-FY2024, peaking notably in FY2023. The company successfully transitioned from low-margin operations to achieving profitability metrics that exceeded industry averages.

UCIC has established itself as a regional leader in the sector, leveraging scale benefits, demonstrated pricing power, and superior cost management to achieve above-industry margins. Its operational excellence is underpinned by exceptional execution, yielding high operating leverage (22.5x) and strong free cash flow generation. However, the investment thesis must account for inherent cyclicality and emerging headwinds. Recent revenue stagnation (-1.3% YoY FY2024, following -3.7% in FY2023) and margin normalization from FY2023 peaks raise questions about sustainability.

The investment case rests on its proven operational excellence, sustainable above-peer profitability (FY2024 Gross Margin: 17.86%, Operating Margin: 8.69%, Net Margin: 7.23%), regional market leadership, and attractive valuation relative to growth (trading below target multiples of 15- 18x P/E and 8-10x EV/EBITDA). Catalysts include resumption of quarterly revenue growth, sustained gross margins above 17%, and new regional infrastructure project awards. UCIC warrants inclusion as a core holding for regional industrial exposure, with a 12–18-month investment horizon, balancing its outstanding fundamental improvement against manageable sector cyclicality.

Cashflow Statement Analysis

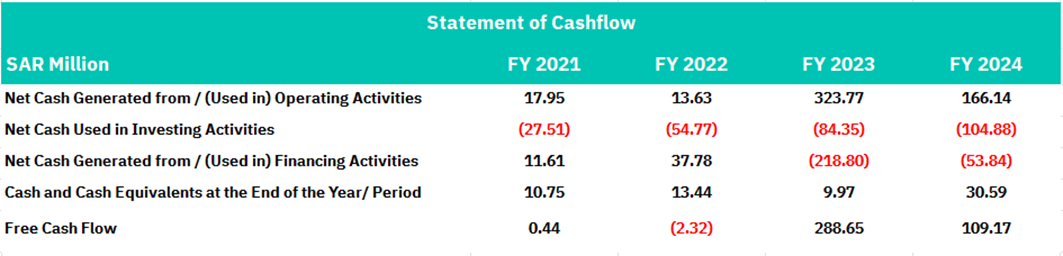

United Carton Industries (UCIC) has demonstrated a powerful operational turnaround, as evidenced by a surge in operating cash flow (OCF). From a low base of 17.95M Saudi Riyal in FY2021, OCF peaked at 323.77M (+2,276% YoY) Saudi Riyal in FY2023 and remained robust at 166.14M (+48.5% YoY) Saudi Riyal in FY2024, yielding a remarkable 4-year OCF CAGR of 107.8%. This underscores the significant improvement in core business fundamentals. Concurrently, the company is aggressively deploying capital into growth, with investing cash outflows accelerating year-over-year (104.88M Saudi Riyal in FY2024, 84.35M Saudi Riyal in FY2023). This sustained and increasing investment intensity (271.51M Saudi Riyal total over 4 years) signals a clear strategic focus on expansion and modernization, positioning UCIC for future scale.

Despite heavy investment, UCIC maintains sound financial discipline. Significant financing cash outflows in FY2023 (218.80M Saudi Riyal) and FY2024 (53.84M Saudi Riyal), following a likely capital raise in FY2022 (37.78M Saudi Riyal inflow), indicate active deleveraging and/or shareholder returns, reflecting a conservative approach to capital structure. This financial prudence is enabled by exceptional free cash flow (FCF) generation. FCF swung dramatically from negative 2.32M Saudi Riyal in FY2022 to highly positive levels of 288.65M (FY2023) Saudi Riyal and 109.17M (FY2024) Saudi Riyal, showcasing the company's enhanced capacity to self-fund growth initiatives and service financial obligations while building liquidity (FY2024 cash balance: 30.59M Saudi Riyal, +207% YoY).

UCIC's core cash generation and financial strategy are positive, citing strong underlying operations, strategic growth investment, and conservative financial management leading to high FCF and improved liquidity. The primary positive hinges on sustained operational excellence and the strategic flexibility afforded by robust cash flow. However, material concerns persist regarding the high volatility in OCF and FCF (notably the normalization from the FY2023 peak), raising questions about earnings consistency and sustainability. Additionally, the significant and accelerating capital expenditure necessitates validated returns on investment (ROI) to justify the outlays and ensure long-term value creation. Regional market exposure and scale remain neutral factors requiring monitoring. Overall, UCIC exhibits strong cash flow fundamentals but must demonstrate greater operational consistency and deliver tangible returns on its growth investments.

Conclusion

United Carton Industries Company is underpinned by exceptional operational transformation and sustainable competitive advantages. The company's remarkable profitability trajectory—evidenced by a 106.8% diluted EPS CAGR over three years and substantial margin expansion (gross margins up 751 bps, operating margins up 825 bps). Despite revenue deceleration in recent periods, UCIC's market-leading position in Saudi Arabia's SAR 1.46 billion packaging sector, coupled with structural tailwinds from Vision 2030 and e-commerce expansion, positions the company to capitalize on long-term secular growth drivers. The firm's vertically integrated operations, diversified end-market exposure, and demonstrated pricing power provide defensive characteristics while maintaining upside optionality.

From a financial perspective, UCIC exhibits the hallmarks of a quality compounder with improving capital efficiency and robust cash generation capabilities. Operating cash flow surged from SAR 18M to SAR 166M, while free cash flow generation of SAR 109M in FY2024 provides ample flexibility for growth investments and potential shareholder returns. The company's conservative debt-to-equity ratio of 0.83x and strategic capital deployment into capacity expansion (SAR 272M invested over four years) reflect disciplined financial management while positioning for future market share gains. However, the recent volatility in cash flows and margin normalization from the 2023 peaks warrant close monitoring of operational consistency.

UCIC as a core regional industrial holding with a 12–18-month investment horizon, targeting entry at current valuations below our fair value estimates of 15-18x P/E and 8-10x EV/EBITDA multiples. Key catalysts include resumption of quarterly revenue growth, sustained gross margins above 17%, and new infrastructure project awards aligned with Saudi Arabia's economic diversification initiatives.

Disclaimer:

Sahm is subject to the supervision and control of the CMA, pursuant to its license no. 22251-25 issued by CMA.

The Information presented above is for information purposes only, which shall not be intended as and does not constitute an offer to sell or solicitation for an offer to buy any securities or financial instrument or any advice or recommendation with respect to such securities or other financial instruments or investments. When making a decision about your investments, you should seek the advice of a professional financial adviser and carefully consider whether such investments are suitable for you in light of your own experience, financial position and investment objectives. The firm and its analysts do not have any material interests or conflicts of interest in any companies mentioned in this report.

Performance data provided is accurate and sourced from reliable platforms, including Argaam, Markwideresearch.

IN NO EVENT SHALL SAHM CAPITAL FINANCIAL COMPANY BE LIABLE FOR ANY DAMAGES, LOSSES OR LIABILITIES INCLUDING WITHOUT LIMITATION, DIRECT OR INDIRECT, SPECIAL, INCIDENTAL, CONSEQUENTIAL DAMAGES, LOSSES OR LIABILITIES, IN CONNECTION WITH YOUR RELIANCE ON OR USE OR INABILITY TO USE THE INFORMATION PRESENTED ABOVE, EVEN IF YOU ADVISE US OF THE POSSIBILITY OF SUCH DAMAGES, LOSSES OR EXPENSES.