3 Bank Stocks Built For Tighter Credit Standards

Southside Bancshares, Inc. SBSI | 0.00 |

When a major lender like HSBC pulls back from riskier private credit, it sends a clear signal about how banks are thinking about risk, capital and funding costs. For you as an investor, that shift can affect where the steadier opportunities and pressure points show up across large, established financial stocks. This article looks at how tightening underwriting standards and rising regulatory attention around private credit might filter through to more conservative banking stocks. It will walk through 3 stocks from our Conservative Banking Stocks screener that appear positively exposed to this news and explain what that could mean for your portfolio decisions.

Southside Bancshares (SBSI)

Overview: Southside Bancshares is a Texas based regional bank that offers a broad range of deposit, lending, wealth management, brokerage, and digital banking services to individuals, businesses, municipalities, and nonprofits through a network of branches, drive thrus, loan offices, ATMs, and interactive teller machines.

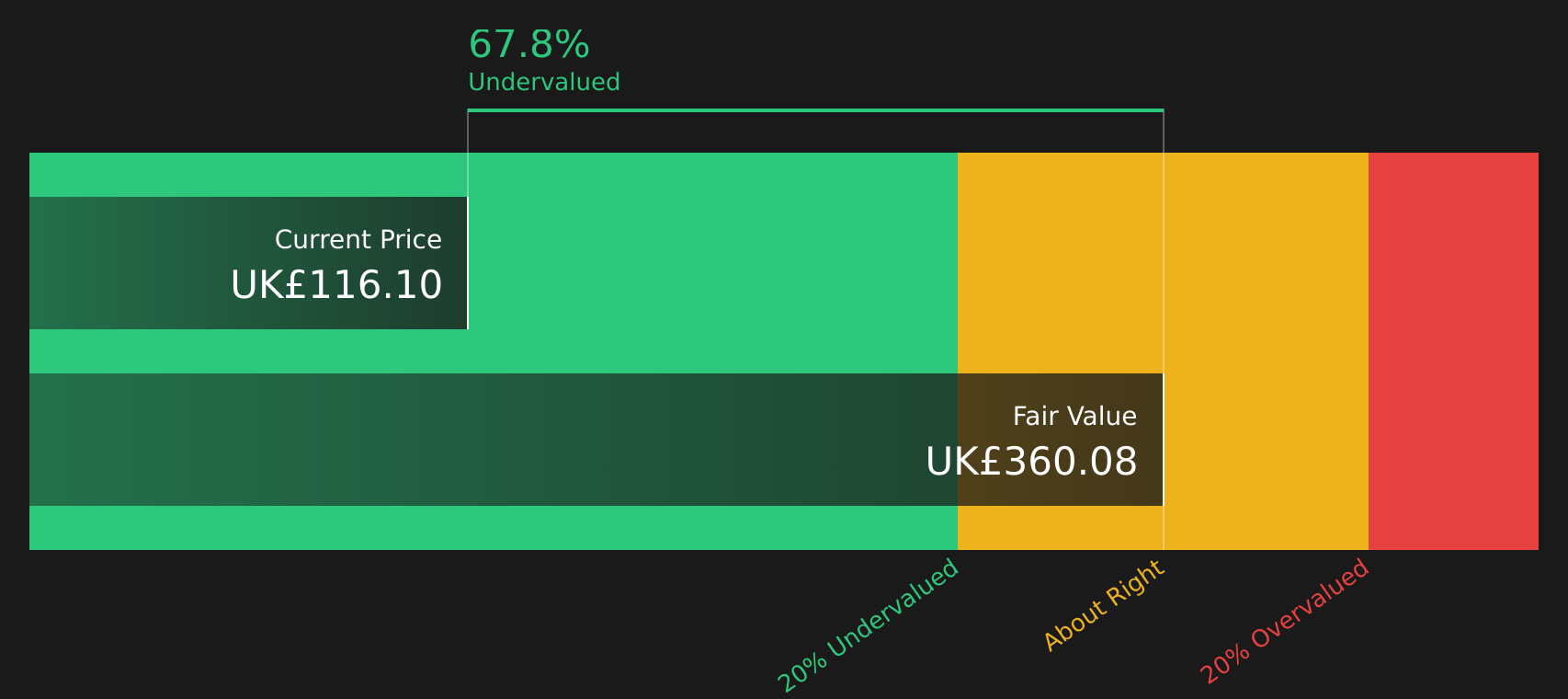

Operations: Southside Bancshares generates all of its approximately US$239.5 million in revenue from banking activities in the United States.

Market Cap: US$1.0b

Southside Bancshares stands out in the Conservative Banking Stocks screener because it leans into traditional, collateral backed lending and wealth services rather than higher risk private credit, which aligns neatly with the recent pullback by global lenders like HSBC. Some investors may focus on its 4.16% dividend, its credit performance, and its independent, experienced board, while also noting that return on equity of 8.3% and a slightly rich P/E raise questions about earnings power. With its Texas market positioning, index inclusions, and consolidation activity in regional banking, the key consideration is how this mix of caution and growth ambition affects the risk reward profile for Southside Bancshares.

Southside Bancshares’ steady 4.16% yield and traditional lending focus might be masking a deeper story about its earnings power and capital strength. See how the Southside Bancshares financial health report could shift your view.

Lion Finance Group (LSE:BGEO)

Overview: Lion Finance Group is a London headquartered banking group that runs one of Georgia's leading banks and a growing Armenian franchise, offering retail, SME and corporate banking, investment banking, and a range of digital and payment services, alongside smaller operations in Belarus and various fintech and business service platforms.

Market Cap: £5.0b

Lion Finance Group appears in the Conservative Banking Stocks screener as a dominant lender in underpenetrated markets that is tightly focused on data driven risk controls, digital distribution and high capital returns, at a time when some global giants such as HSBC are pulling back from riskier private credit. Earnings have grown strongly in recent years, profitability and return on equity are robust, and analysts see scope for further growth, yet the stock still trades below some estimates of fair value. Against this, investors need to weigh an unstable dividend record, elevated bad loans of 2.1% with relatively low loss allowances, and recent insider selling. For investors who can accept those risks, the combination of disciplined risk culture and growth in Georgia and Armenia may make Lion Finance Group a notable option to consider.

Growth in underpenetrated markets with strong profitability makes Lion Finance Group look like a story that is only half told. See how the analyst forecasts for Lion Finance Group reframes the upside and the risks investors often miss.

Beacon Financial (BBT)

Overview: Beacon Financial is a Boston headquartered bank holding company that gathers deposits from commercial, municipal and retail clients and channels them into mortgage, commercial and equipment loans, while also offering cash management, trust, wealth management and advisory services in the United States and abroad.

Operations: Beacon Financial generates US$632.9 million in revenue entirely from its core banking activities in the United States.

Market Cap: US$2.5b

Beacon Financial sits squarely in the conservative banking camp, with a long history, a focus on traditional lending and deposits, and a reputation for disciplined underwriting that looks particularly relevant as global lenders such as HSBC retreat from riskier private credit. Analysts expect strong revenue and earnings growth alongside buybacks, while index additions and a regular dividend support visibility and capital return. Set against that are real pressure points, including a recent US$73.8 million one off loss, elevated charge offs and a relatively inexperienced board, which could matter if credit trends worsen. For investors who want a conservatively run bank that may benefit as funding tightens for higher risk players, the key question is whether Beacon’s growth outlook and balance sheet justify looking past those bumps in the road.

Beacon Financial’s growth story, regular dividend and recent one off loss create a tension many investors might be underestimating. The analysis report for Beacon Financial pulls these threads together and surfaces a twist most overlook.

The three stocks covered here are just a snapshot of what this idea surfaces. The full Conservative Banking Stocks screener uncovers 33 more conservative banking companies that pair solid fundamentals with equally compelling narratives. Use Simply Wall St to identify the specific catalysts, underwriting profiles and dividend characteristics that matter most to you, and analyze those stories side by side so you can focus on the highest conviction opportunities.

Take Control of Your Investment Journey

If Southside Bancshares or any of these companies sound like a great opportunity, register for FREE with Simply Wall St and add your companies to a Watchlist to monitor the share price against the fair value the ideal entry point. Once you've made your move, manage your holdings with our Portfolio Command Center that filters out the noise to deliver only the most critical, actionable updates. Throughout your journey, our Community allows you to filter the best ideas from thousands of investor perspectives. By uncovering hidden catalysts and risks early, you'll accelerate your decision-making and stay one step ahead of the market.

Seeking Fresh Alternatives Beyond Banks?

Fresh stock ideas do not stay under the radar for long. Before the next breakout gathers momentum and gets caught by the crowd, review these focused screeners and act now.

- Spot companies quietly building momentum before prices start flying by reviewing the curated 18 high quality undiscovered gems while they are still under the radar for now.

- Capture potential income opportunities that other investors may overlook by scanning our hand picked 8 dividend fortresses while yields and fundamentals still line up.

- Position ahead of possible infrastructure spending waves by checking the targeted 35 power grid technology and infrastructure stocks while these businesses are still dropping clues, not headlines.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.