3 Clinical-Stage Biotech Stocks Worth Watching In Parkinson's Research

Gain Therapeutics, Inc. GANX | 0.00 |

Clinical stage biotech stocks linked to Parkinson's research sit at the crossroads of medical science and market attention, especially as global growth signals remain mixed and central banks keep policy in flux. While inflation trends, energy prices and PMIs shape overall risk appetite, many investors are looking for focused themes that cut through the noise. This Parkinson's screener does exactly that by zeroing in on companies with treatments already in human trials, where clinical milestones can become key share price catalysts. Below, the article highlights 3 of the most closely watched stocks from this screener that may merit a closer look.

Gain Therapeutics (GANX)

Overview: Gain Therapeutics is a clinical stage biotech developing small molecule drugs that aim to treat the root cause of diseases like Parkinson's, dementia with Lewy bodies, Alzheimer's and Gaucher's by using its Magellan platform to find new binding sites on misfolded or dysfunctional proteins. Its lead pill, GT-02287, is in a Phase 1b study for Parkinson's disease with or without a GBA1 mutation and is designed to improve function of the GCase enzyme pathway that is implicated in disease progression.

Market Cap: US$80.2m

Investors watching Parkinson's research closely may find Gain Therapeutics interesting because GT-02287 has early human data linking an 81% drop in a toxic brain biomarker with measurable improvement in motor scores, supported by patients choosing to stay in long term extension treatment.

At the same time, this is a small, loss making biotech with no current revenue, a cash runway of less than one year, a going concern flag from auditors and a history of shareholder dilution, so future funding and clinical results are critical swing factors. For readers who can tolerate higher risk, the mix of a potentially disease modifying oral therapy, a broader Magellan powered pipeline and a modest market value makes the trade off between upside and dilution risk an important question to focus on.

The most followed Simply Wall St Community Narrative on Gain Therapeutics, published on 2 April 2026, takes a notably more bullish read. Its author places fair value at US$7.60 per share against the current US$1.72, a gap of roughly 77 percent that rests on the view the market is underpricing the early clinical signal from GT-02287 in a US Parkinson's market with no approved disease modifying therapies. The narrative leans on the Phase 2a trial expected in the third quarter of 2026 as the key inflection point and anchors its valuation against prior deals in the space, including Eli Lilly's roughly US$1 billion acquisition of Prevail Therapeutics, while still acknowledging the financing strain and the limits of small, open label data. For readers genuinely interested in how that case is built, the full narrative is worth reading alongside the warning signs.

Gain Therapeutics has an oral Parkinson's pill with early human signals that many investors may be underestimating, yet its funding strain could be just as important, so review the 4 warning signs (3 are major!).

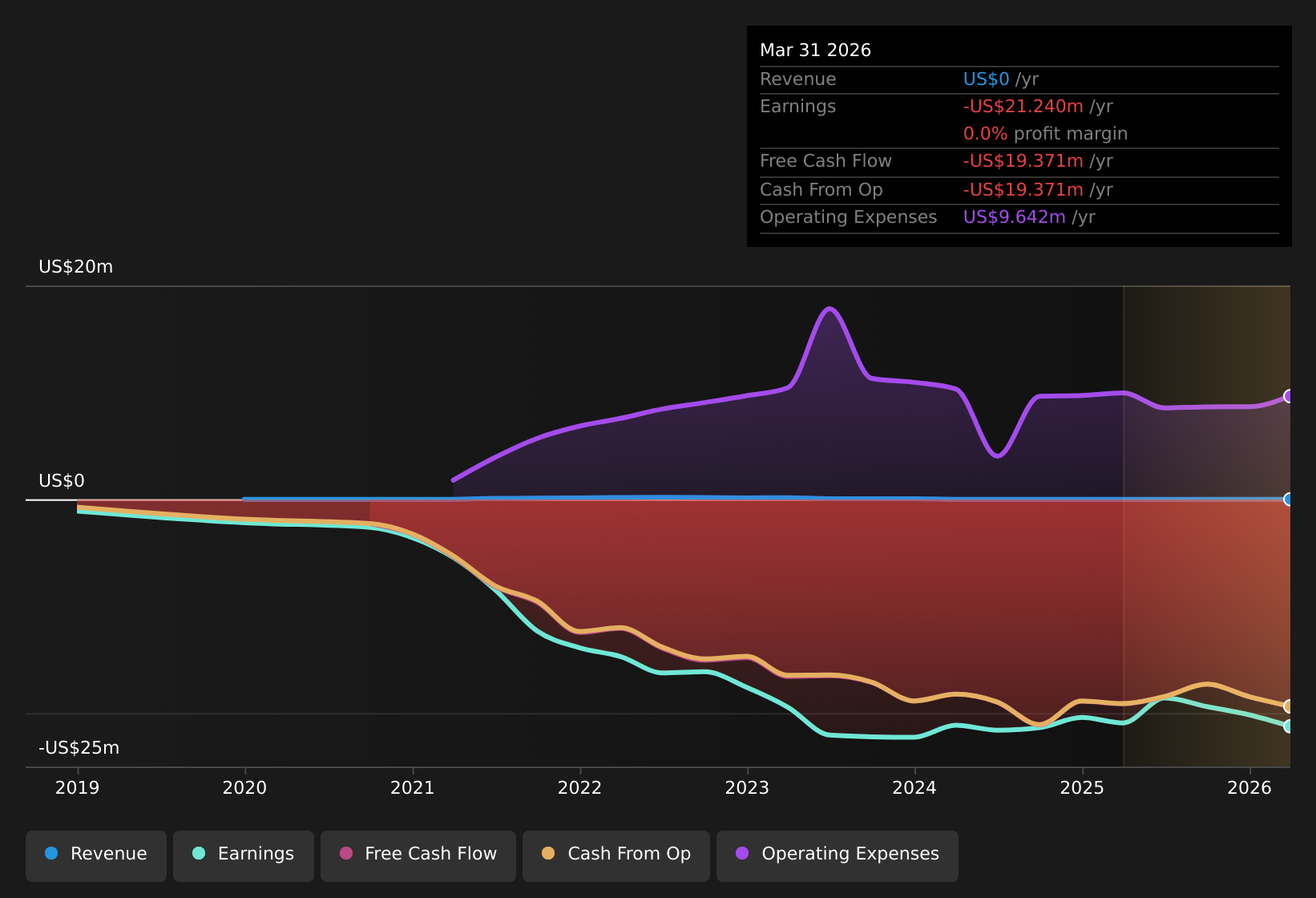

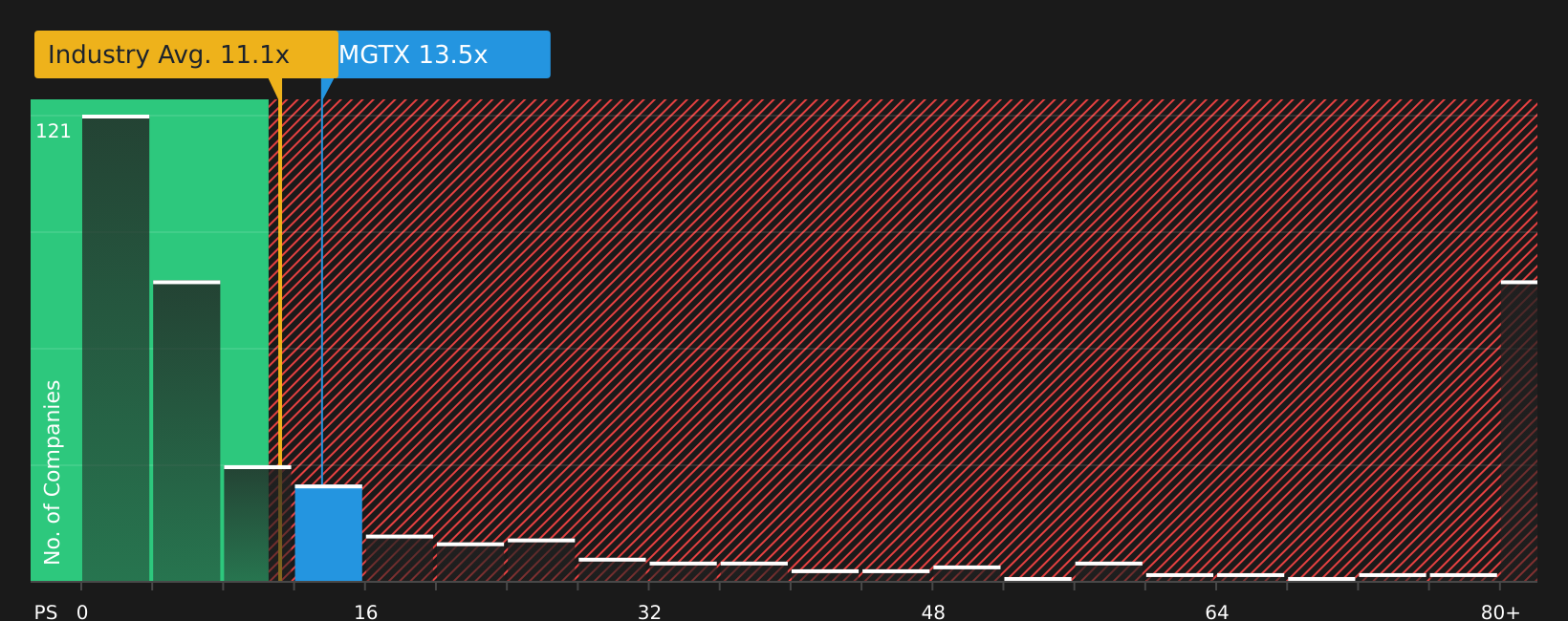

MeiraGTx Holdings (MGTX)

Overview: MeiraGTx Holdings is a clinical stage genetic medicines company developing gene therapies for serious conditions, with a focus on eye diseases, neurodegenerative disorders such as Parkinson's, and glandular conditions like radiation induced dry mouth.

Operations: MeiraGTx generates US$79.8 million in revenue from the development and manufacturing of genetic medicines, with all reported revenue currently coming from the United Kingdom.

Market Cap: US$1.07b

MeiraGTx fits this Parkinson's focused screener well, with its AAV GAD Parkinson's program and AAV2 hAQP1 dry mouth therapy both carrying FDA RMAT designations and one already holding Breakthrough Therapy status. Forecast revenue growth is strong; however, the company remains loss making, carries negative equity and relies on external funding, so this is not a low risk balance sheet.

At the same time, board independence is high, tenure is long, and analysts see scope for upside even as the stock trades on a rich P/S multiple. The key consideration is how these fast moving clinical and funding developments compare when viewed side by side.

MeiraGTx looks like a Parkinson's contender with big potential, but the funding gap and rich P/S raise questions about what the market is really pricing in, so review the 1 key reward and 3 important warning signs (1 is major!).

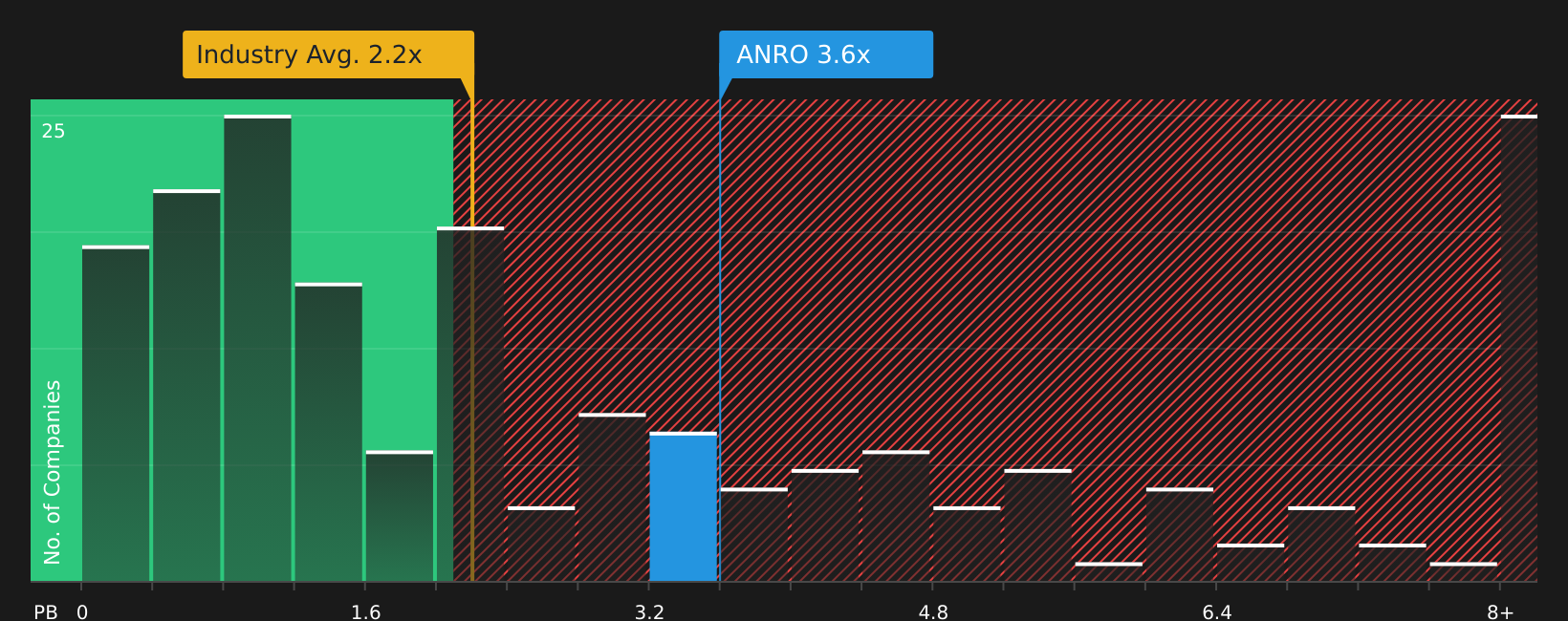

Alto Neuroscience (ANRO)

Overview: Alto Neuroscience is a clinical stage biopharmaceutical company focused on treating mental health conditions such as major depressive disorder, bipolar depression, cognitive impairment in schizophrenia and anhedonia, using a pipeline of oral small molecule drugs guided by neuroscience data.

Market Cap: US$857.7m

Alto Neuroscience may interest investors who want exposure to next generation neuroscience, as its ALTO-207 program is moving into a Phase 2b trial in treatment resistant depression on the back of Phase 2a data showing significant improvement on the MADRS scale versus placebo. A Nature Medicine publication on pramipexole based therapy adds scientific support for its approach.

Still, Alto is loss making with widening quarterly losses, minimal near term revenue, high reliance on external borrowing and a P/B multiple above peers, so funding and execution risk are central issues. With new board expertise in neuropsychiatric drug development and a focused push behind ALTO-207, the key issue for investors is how this risk reward profile compares with other Parkinson's and depression focused biotechs in the same space.

Alto Neuroscience is pushing ahead in treatment resistant depression while its losses, borrowing and P/B premium keep many investors cautious, so review the analyst forecasts for Alto Neuroscience to see what expectations might be missing.

The three Parkinson's focused stocks covered here are only a starting point, with the full screener surfacing 11 more clinical stage biotechs that each bring their own pipeline story and potential clinical catalysts to the table in the Clinical-Stage Biotech Stocks Worth Watching In Parkinson's Research Clinical-Stage Biotech Stocks Worth Watching In Parkinson's Research screener. Identify and analyze the catalysts that matter most to you by using Simply Wall St to filter for active human trials, upcoming readouts and narrative flags so you can focus on the highest conviction Parkinson's opportunities for your watchlist.

Take Control of Your Investment Journey

If Gain Therapeutics or any of these companies have caught your attention, register for FREE with Simply Wall St and add your companies to a Watchlist to monitor the share price against the fair value and track any new developments as they happen. Once you've made your move, manage your holdings with our Portfolio Command Center that filters out the noise to deliver only the most critical, actionable updates. Throughout your journey, our Community allows you to filter the best ideas from thousands of investor perspectives. By uncovering hidden catalysts and risks early, you'll accelerate your decision-making and stay one step ahead of the market.

Seeking Alternatives Beyond Parkinson's Stocks?

Fresh ideas move first when momentum builds, and the best entries can be gone before the crowd even notices. Scan these curated stock lists while it still matters and consider them while they are still timely.

- Spot resilient opportunities that aim to keep capital at work through volatility by checking out a curated group of 69 resilient stocks with low risk scores that may hold up when sentiment turns.

- Capture potential yield while prices are still adjusting by reviewing carefully filtered 7 dividend fortresses aiming to combine strong payouts with balance sheets that support ongoing distributions.

- Target future facing infrastructure as demand for computing power accelerates by assessing a focused mix of 49 AI infrastructure stocks positioned around the build out of AI capacity.

Simply Wall St analyst Mitch Lawler and Simply Wall St have no position in any of the companies mentioned. This article is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.