3 Growth Companies With High Insider Ownership And 27% Revenue Growth

Hesai Group HSAI | 0.00 |

The United States market remained flat over the last week but has seen a 25% increase over the past year, with earnings forecasted to grow by 17% annually. In such an environment, growth companies with high insider ownership can be particularly attractive as they often signal strong confidence from those closest to the business and potential alignment of interests between management and shareholders.

Top 10 Growth Companies With High Insider Ownership In The United States

| Name | Insider Ownership | Earnings Growth |

| Uxin (UXIN) | 35.7% | 74.1% |

| Upstart Holdings (UPST) | 12.8% | 58.5% |

| Strive Asset Management (ASST) | 16% | 72.2% |

| SharonAI Holdings (SHAZ) | 29.9% | 97.4% |

| Precigen (PGEN) | 11.9% | 68.4% |

| Laird Superfood (LSF) | 16.1% | 93.8% |

| Corcept Therapeutics (CORT) | 11.8% | 48.7% |

| Clene (CLNN) | 10.9% | 61.7% |

| Astera Labs (ALAB) | 10.7% | 31.5% |

| AppLovin (APP) | 27.4% | 21.5% |

Let's uncover some gems from our specialized screener.

Hesai Group (HSAI)

Simply Wall St Growth Rating: ★★★★★☆

Overview: Hesai Group develops, manufactures, and sells three-dimensional LiDAR solutions across Mainland China, Europe, North America, and internationally with a market cap of $3.35 billion.

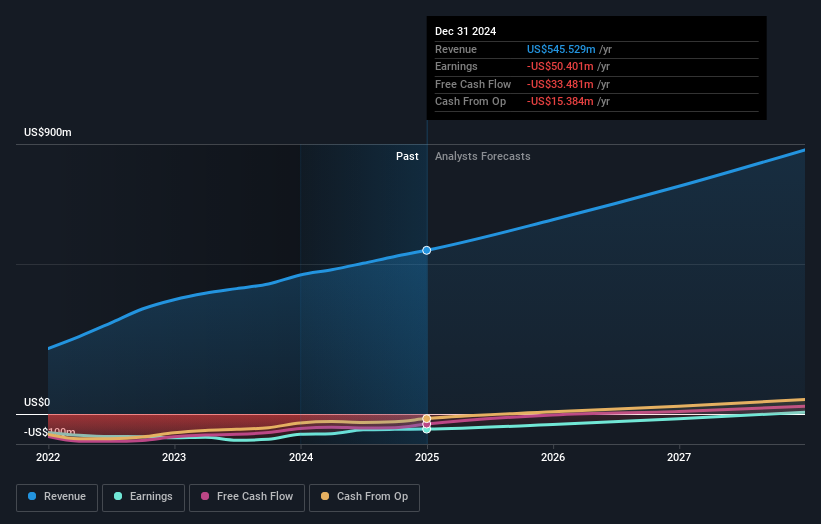

Operations: The company's revenue from its LiDAR product development, manufacturing, and delivery amounts to CN¥3.03 billion.

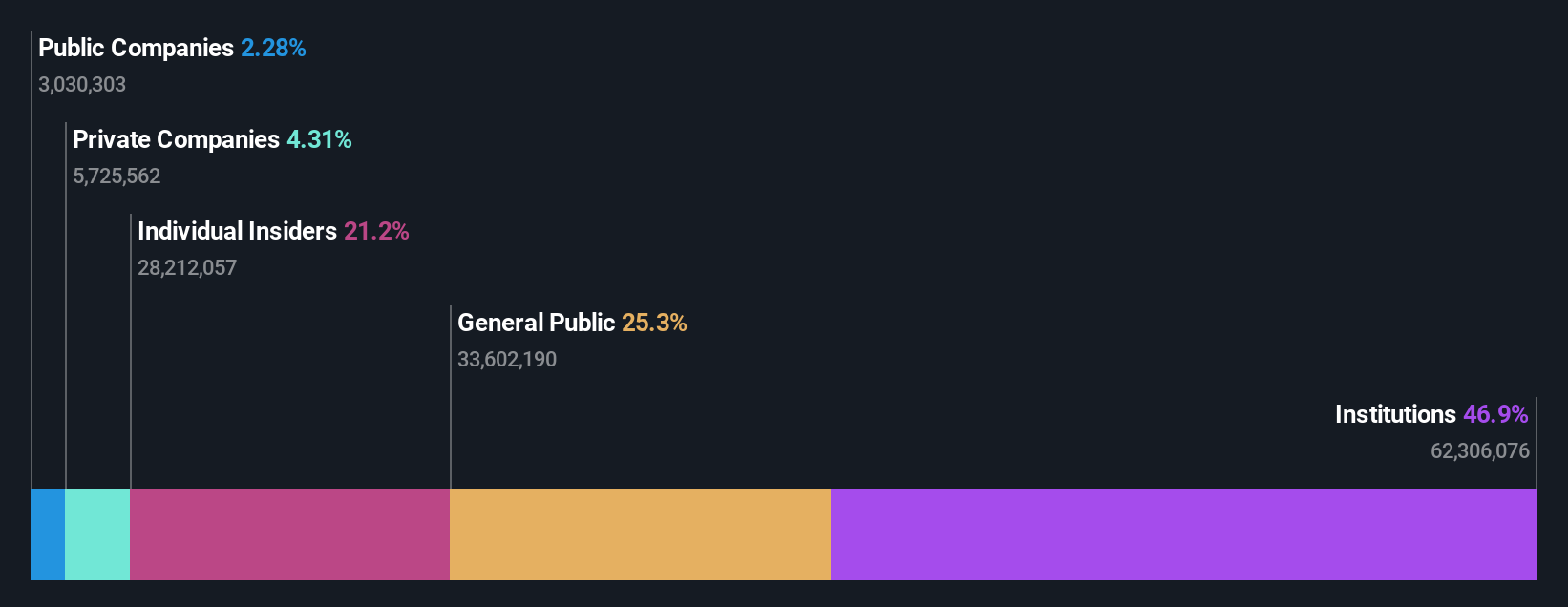

Insider Ownership: 17.5%

Revenue Growth Forecast: 25.5% p.a.

Hesai Group is experiencing significant growth, with revenue forecasted to increase by 25.5% annually, outpacing the US market average. The company's strategic shift towards spatial intelligence and innovative lidar technologies like the Picasso platform supports its growth trajectory. Despite past shareholder dilution, Hesai's earnings are expected to grow at 27.1% per year, surpassing market averages. Recent collaborations and product launches further solidify its position in autonomous systems and robotics sectors.

Xometry (XMTR)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Xometry, Inc. operates an AI-powered online manufacturing marketplace serving both the United States and international markets, with a market cap of $4.41 billion.

Operations: The company's revenue primarily comes from its Internet Software & Services segment, totaling $740.80 million.

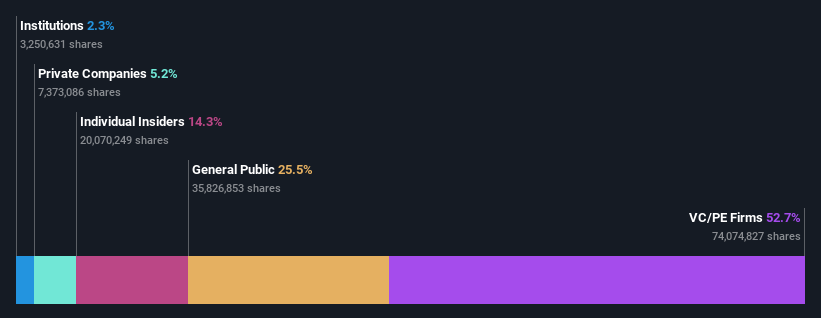

Insider Ownership: 12.4%

Revenue Growth Forecast: 17.9% p.a.

Xometry is poised for significant growth, with earnings expected to grow 109.3% annually and profitability anticipated within three years, surpassing market averages. Despite a volatile share price, recent strategic partnerships like the one with Siemens enhance its AI-native manufacturing capabilities and market reach. Insider activity shows more buying than selling recently, indicating confidence in the company's trajectory. Recent earnings reveal improved financial performance with sales reaching US$205.14 million for Q1 2026.

Karman Holdings (KRMN)

Simply Wall St Growth Rating: ★★★★★☆

Overview: Karman Holdings Inc., with a market cap of $8.27 billion, operates in the United States through its subsidiary to design, test, manufacture, and sell mission-critical systems.

Operations: Revenue Segments (in millions of $):

Insider Ownership: 17%

Revenue Growth Forecast: 27.7% p.a.

Karman Holdings is set for robust growth, with revenue projected to rise 27.7% annually, outpacing the US market. Earnings are expected to grow significantly at 51.9% per year. Recent strategic moves include seeking acquisitions and securing contingent commitments worth over US$1 billion from key customers, indicating strong demand in space and defense sectors. However, interest payments remain a concern as they are not well covered by earnings despite improved Q1 financial results with sales of US$151.21 million.

Turning Ideas Into Actions

- Unlock our comprehensive list of 187 Fast Growing US Companies With High Insider Ownership by clicking here.

- Seeking Other Investments? Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.