3 High Dividend Stocks With Margins And Balance Sheet Risk

Gaming and Leisure Properties, Inc. GLPI | 0.00 |

With bond vigilantes back in focus, Treasury yields climbing and markets suddenly pricing in a 42% chance of a Fed rate hike by year end, income investors face a tougher test of which dividends might hold up if borrowing costs stay higher for longer. This article looks at how that backdrop, along with expectations that incoming Fed Chair Kevin Warsh may still lean dovish even as the Fed shifts to a tightening bias, could affect a group of high dividend stocks exposed to these rate signals. Below, you will see 3 stocks from the screener that could stand out for income focused portfolios.

Grainger (LSE:GRI)

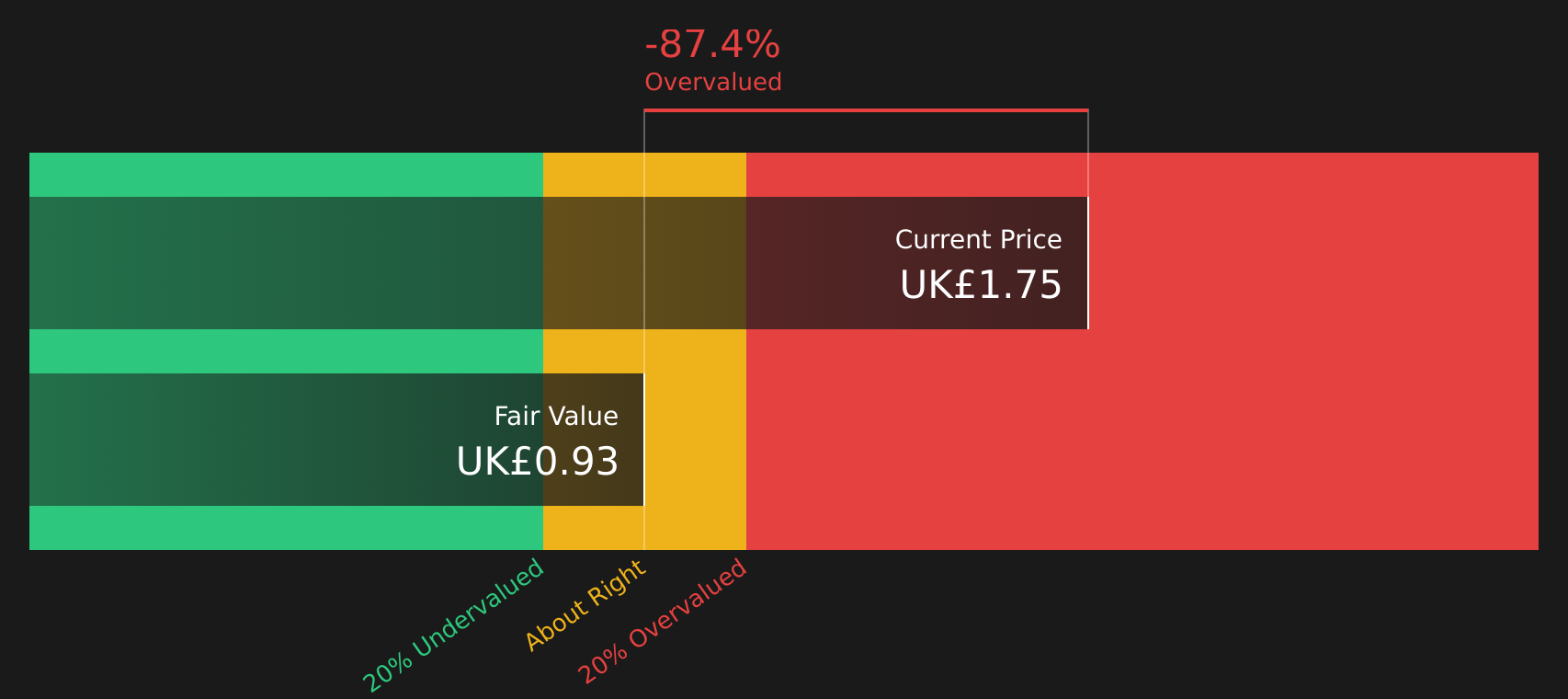

Overview: Grainger is a long established UK landlord that designs, develops, owns and manages rental homes, mainly through its Private Rented Sector portfolio, alongside a book of regulated tenancies and a smaller legacy land and mortgage business.

Operations: Grainger generates most of its revenue from the Private Rented Sector (£164.3m) and Reversionary (£73.6m) segments, with a small contribution from Other (£2.1m), all in the United Kingdom (£240m).

Market Cap: £1.24b

Income investors looking at Grainger are weighing a high dividend track record and UK residential rental exposure against funding risks that matter more as rates stay elevated. The stock trades on a P/E that is well below both the wider UK market and its Residential REIT peers, yet the current share price sits above the Simply Wall St cash flow estimate, which suggests potential valuation tension. Recent refinancing has pushed £540m of bank facilities out to 2033 and trimmed finance costs, but debt is still not well covered by operating cash flow and there have been sizeable one off items and a recent net loss. The key consideration is whether a 54.8% net margin and forecast earnings growth are sufficient to balance the risk profile while bond markets remain in focus.

Grainger looks like a puzzle, with a low P/E and high net margin sitting alongside stretched cash flow cover and recent losses. Get the full context in the 5 key rewards and 2 important warning signs (1 is major!)

Gaming and Leisure Properties (GLPI)

Overview: Gaming and Leisure Properties is a US real estate investment trust that owns casino and gaming properties and leases them out under triple net agreements, where tenants cover maintenance, insurance, taxes and utilities. This structure aims to give the company relatively predictable rental income while leaving day to day operational risk with the casino operators.

Operations: Gaming and Leisure Properties generates all of its US$1.6b in revenue from investments in real estate within the United States.

Market Cap: US$12.6b

Income investors looking at Gaming and Leisure Properties are weighing a high yielding, triple net lease model against the reality that debt is not well covered by operating cash flow and all liabilities rely on external funding. The stock screens as good value on earnings, trades well below the Simply Wall St cash flow estimate and sits on a net profit margin of about 55%. However, its dividend track record is flagged as unstable and recent share price performance has lagged the broader US market and specialized REIT peers. With bond markets pressuring the Fed toward a tighter stance and investors rethinking rate cut hopes, GLPI’s combination of relatively predictable rental streams, disciplined capital allocation comments on recent calls and balance sheet trade offs may warrant closer consideration for those who want equity income as an alternative to volatile bonds.

Gaming and Leisure Properties’ high margin rent streams and low P/E are easy to see, but the real tension sits in its funding mix and payout profile. Weigh that trade off properly with the 5 key rewards and 2 important warning signs (1 is major!)

Chemtrade Logistics Income Fund (TSX:CHE.UN)

Overview: Chemtrade Logistics Income Fund is a Toronto based chemicals producer that supplies sulphur and water treatment products, electrochemicals and specialty chemicals used in industries such as semiconductors, pulp and paper, food and beverage, agriculture, mining and oil and gas across North and South America.

Operations: Chemtrade generates most of its CA$1.30b business revenue from the Electrochemicals (EC) segment at CA$752.0m, with additional contributions from Segment Adjustment at CA$1.30b and Corporate Items and Eliminations at CA$12.9m, while geographically revenue is spread across the United States (CA$1.30b), Canada (CA$632.1m) and Brazil (CA$98.0m).

Market Cap: CA$1.72b

Chemtrade Logistics Income Fund is drawing attention from income investors because it pairs an income trust structure and high distributions with a chemicals portfolio tied to water treatment, domestic semiconductor build out and other essential uses. This combination can be appealing as rates stay higher for longer and investors search for defensive yield. The units trade well below the Simply Wall St cash flow estimate, analysts see room for earnings to grow and management is cleaning up the balance sheet, redeeming 7.00% convertible debentures and actively buying back units. Set against that are high leverage, an unstable dividend history, a large recent one off loss and thinner margins. The key issue is how sustainable this income stream looks if funding costs stay elevated and acquisitions continue.

Chemtrade’s income story may look straightforward, but the mix of high distributions, balance sheet cleanup and unit buybacks raises bigger questions about risk and resilience. Get the full picture in the 4 key rewards and 3 important warning signs

The three dividend stocks in this article are just a starting point, and the full High-Dividend Yield Equity screener surfaces 19 more companies with similarly income focused stories that may be worth a closer look. Use Simply Wall St to identify and analyze the specific catalysts, payout records and financial narratives that matter to you so you can focus on the highest conviction ideas for your portfolio.

Take Control of Your Investment Journey

If Grainger or any of these companies sound like a great opportunity, register for FREE with Simply Wall St and add your companies to a Watchlist to monitor the share price against the fair value the ideal entry point. Once you've made your move, manage your holdings with our Portfolio Command Center that filters out the noise to deliver only the most critical, actionable updates. Throughout your journey, our Community allows you to filter the best ideas from thousands of investor perspectives. By uncovering hidden catalysts and risks early, you'll accelerate your decision-making and stay one step ahead of the market.

Seeking Alternatives Before Everyone Else?

Fresh ideas move fast, and stocks flying under the radar can change once momentum builds. Review these curated lists before the wider market focuses on them.

- Target potential income streams by reviewing a curated group of payout heavyweights using the 5 dividend fortresses while yields remain available and attention is elsewhere.

- Identify potential turnaround candidates by scanning the 6 high quality undervalued stocks, which pairs quality fundamentals with compressed valuations before sentiment and prices change.

- Focus on companies with sturdier balance sheets by assessing the list of solid balance sheet and fundamentals (18 results) to see which businesses may be better positioned to handle higher funding costs.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.