3 High Dividend Yield Stocks With Staying Power

T. Rowe Price Group, Inc. TROW | 0.00 |

Choppy signals on interest rates, growth, and energy markets are pushing more investors to look at high dividend yield stocks as potential anchors for their portfolios. With central banks watching inflation and employment data closely, income from dividends can feel more tangible than trying to second guess the next policy move. This article focuses on companies with larger market caps and relatively high dividend yields, where dividend and financial health scores look solid and payout ratios appear manageable. Below, you will see 3 stocks from this screener that are currently exposed to these macro shifts in different ways.

T. Rowe Price Group (TROW)

Overview: T. Rowe Price Group is a Baltimore based asset manager that runs mutual funds, ETFs and other investment products for individuals, retirement plans and institutions around the world. It uses in house research and a mix of fundamental and quantitative analysis, including ESG focused strategies.

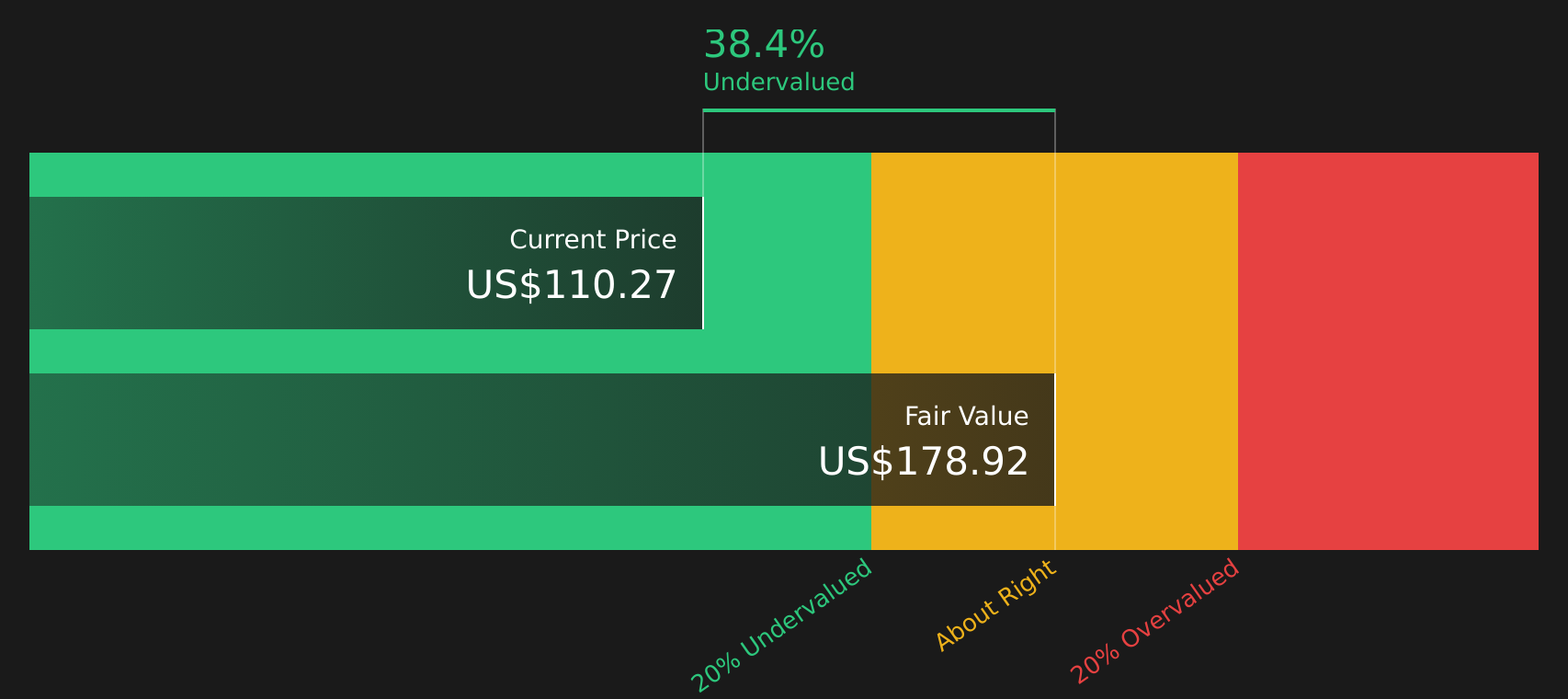

Operations: T. Rowe Price Group generates about US$7.4b in revenue from Investment Management Services, reflecting fees earned on assets it manages for clients.

Market Cap: US$22.8b

Investors looking at high dividend yield stocks may find T. Rowe Price Group interesting because it combines a 4.72% dividend yield with a long history in retirement focused investing. This comes at a time when central banks and rate expectations are keeping markets on edge. The stock trades on a P/E of 11.6x compared with much higher averages in the US capital markets sector. Analysts see fair value materially above the current price based on discounted cash flows. At the same time, T. Rowe Price is contending with fee pressure, competition from low cost products and earnings forecasts that point to modest decline. This makes it important to understand how its new ETFs, alternatives and expense discipline could influence the story from here.

T. Rowe Price Group’s modest P/E and 4.72% yield suggest that the market may be missing something in this asset manager’s transition. Get the full story, including valuation assumptions, in the DCF valuation analysis for T. Rowe Price Group

Canadian Natural Resources (TSX:CNQ)

Overview: Canadian Natural Resources is a Calgary based oil and gas producer that acquires, develops, and operates crude oil, oil sands, natural gas, and natural gas liquids assets across Western Canada, the UK North Sea, and offshore Africa, selling a mix of synthetic crude, conventional crude, heavy oil, bitumen, and NGLs.

Operations: Canadian Natural Resources generates most of its revenue from Exploration and Production in North America at about CA$19.1b and Oil Sands Mining and Upgrading at about CA$17.4b, with smaller contributions from Midstream and Refining at about CA$0.8b and the North Sea at about CA$0.2b.

Market Cap: CA$116.9b

Canadian Natural Resources gives dividend focused investors exposure to income from a large producer with a wide resource base at a time when energy prices can swing sharply on geopolitics and supply headlines. Earnings and margins are currently strong, and the dividend yield is about 4.46%. At the same time, the business is tied to higher cost oil sands, is exposed to carbon policy and pipeline constraints, and recently booked a CA$5.1b one off gain that can make headline results look stronger than underlying trends. A key consideration for investors is how its cost discipline, buybacks, and infrastructure access might shape returns if energy markets stay volatile and inflation remains a risk for many portfolios.

Canadian Natural Resources’ strong margins and 4.46% yield may look straightforward, but the real story could sit in how its asset mix and capital returns line up against future energy swings, which is unpacked in the analysis report for Canadian Natural Resources

ICG (LSE:ICG)

Overview: ICG is a London based private equity and credit investor that raises capital from institutions and then lends to or invests in mid sized companies globally through private debt, secondaries and other alternative strategies, aiming to generate income and capital growth from these portfolios.

Operations: ICG generates about £897.7m of revenue from its Fund Management Company activities, with smaller contributions from Investment Company at £42.5m and Consolidated Entities at £33.8m.

Market Cap: £4.6b

ICG may appeal to income focused investors because it pairs exposure to private credit and private equity with a long record of dividend per share growth, now in its 16th year, and a total payout of 87p for 2026. Management fee income and transaction activity are closely tied to assets under management, so any slowdown in fundraising or more intense competition in private markets could weigh on growth. At the same time, experienced management, broad sector coverage across Europe, North America and Asia Pacific, and quality earnings give ICG a different risk return profile compared with traditional banks or listed asset managers. A key question for investors is how that mix, together with its funding structure and valuation signals, compares with other high yield options in this screener.

ICG’s mix of private credit income and long running dividend growth often looks straightforward, yet its valuation signals and earnings quality suggest a more complex story that comes through in the full narrative for ICG

The three high dividend ideas here are just a starting point, with the full High Dividend Yield Stocks screener surfacing 21 more companies that pair sizeable market caps with income potential and detailed narratives that might not be obvious at first glance through the High Dividend Yield Stocks screener. Use Simply Wall St to identify, analyze, and filter for the specific catalysts, balance sheet strength, payout ratios, and dividend profiles that match your highest conviction income ideas.

Take Control of Your Investment Journey

If ICG or any of these companies sound like a great opportunity, register for FREE with Simply Wall St and add your companies to a Watchlist to monitor the share price against the fair value the ideal entry point. Once you've made your move, manage your holdings with our Portfolio Command Center that filters out the noise to deliver only the most critical, actionable updates. Throughout your journey, our Community allows you to filter the best ideas from thousands of investor perspectives. By uncovering hidden catalysts and risks early, you'll accelerate your decision-making and stay one step ahead of the market.

Seeking Fresh Alternatives Beyond Dividends

Some of the most interesting ideas can move from quiet to flying on fresh catalysts before the crowd catches on, so use these curated lists while it matters and act now.

- Spot companies pushing for breakout consistency by scanning a curated group of strong operators in the list of solid balance sheet and fundamentals (48 results) and see which ones still look under the radar.

- Ride potential momentum in future critical materials by tracking the curated 29 best rare earth metal stocks list before capital flows make entry points harder to catch.

- Zero in on resilience with income potential by working through a hand picked set of 71 resilient stocks with low risk scores that aim to balance stability with room for fresh catalysts.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.