3 Insider-Owned Growth Companies To Watch Now

Estee Lauder Companies Inc. Class A EL | 0.00 |

Over the last 7 days, the United States market has remained flat, yet it is up 18% over the past year with earnings forecasted to grow by 18% annually. In this environment, growth companies with high insider ownership can be appealing as they often indicate strong confidence from those closest to the business and potential alignment of interests with shareholders.

Top 10 Growth Companies With High Insider Ownership In The United States

| Name | Insider Ownership | Earnings Growth |

| Uxin (UXIN) | 34.3% | 69.4% |

| Upstart Holdings (UPST) | 14.1% | 58.9% |

| QT Imaging Holdings (QTI) | 23.9% | 104.2% |

| OS Therapies (OSTX) | 12.4% | 72.1% |

| Karman Holdings (KRMN) | 15.6% | 52.6% |

| IREN (IREN) | 13.7% | 38.7% |

| ERock (EROC) | 20.1% | 56.3% |

| Corcept Therapeutics (CORT) | 10.9% | 48.9% |

| Astera Labs (ALAB) | 10.1% | 30.9% |

| AppLovin (APP) | 23.2% | 21.7% |

Here we highlight a subset of our preferred stocks from the screener.

EquipmentShare.com (EQPT)

Simply Wall St Growth Rating: ★★★★★☆

Overview: EquipmentShare.com Inc. offers integrated, full-service construction solutions through equipment rental, sales, and technology, with a market cap of $4.54 billion.

Operations: The company's revenue is primarily derived from equipment rental and service operations at $2.93 billion, followed by equipment sales totaling $1.58 billion.

Insider Ownership: 15.1%

Earnings Growth Forecast: 48.2% p.a.

EquipmentShare.com, a growth company with significant insider ownership, is experiencing robust earnings growth forecasted at 48.2% annually, outpacing the US market. Despite this strong earnings trajectory and recent profitability, its revenue growth of 17.4% per year lags behind the ideal threshold for high-growth companies. The company's financial position is challenged by interest payments not being well covered by earnings. Recent substantial insider buying suggests confidence in future prospects despite volatility and financing activities involving $1.35 billion in new notes due 2034 at a 7.125% interest rate to manage debt obligations and fund operations.

PDF Solutions (PDFS)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: PDF Solutions, Inc. offers proprietary software, intellectual property for integrated circuit designs, measurement hardware tools, methodologies, and professional services globally with a market cap of $2.16 billion.

Operations: The company's revenue is primarily derived from its Software & Programming segment, which generated $231.38 million.

Insider Ownership: 10.6%

Earnings Growth Forecast: 71.8% p.a.

PDF Solutions is experiencing significant earnings growth, forecasted at 71.8% annually, surpassing the US market's growth rate. Recent financial results show a positive turnaround with Q1 net income of US$4.79 million compared to a loss previously. Revenue growth is expected at 16.8% annually, slightly below high-growth benchmarks but above the market average. A recent follow-on equity offering raised approximately US$201 million, supporting further expansion despite share price volatility and no substantial insider trading activity recently noted.

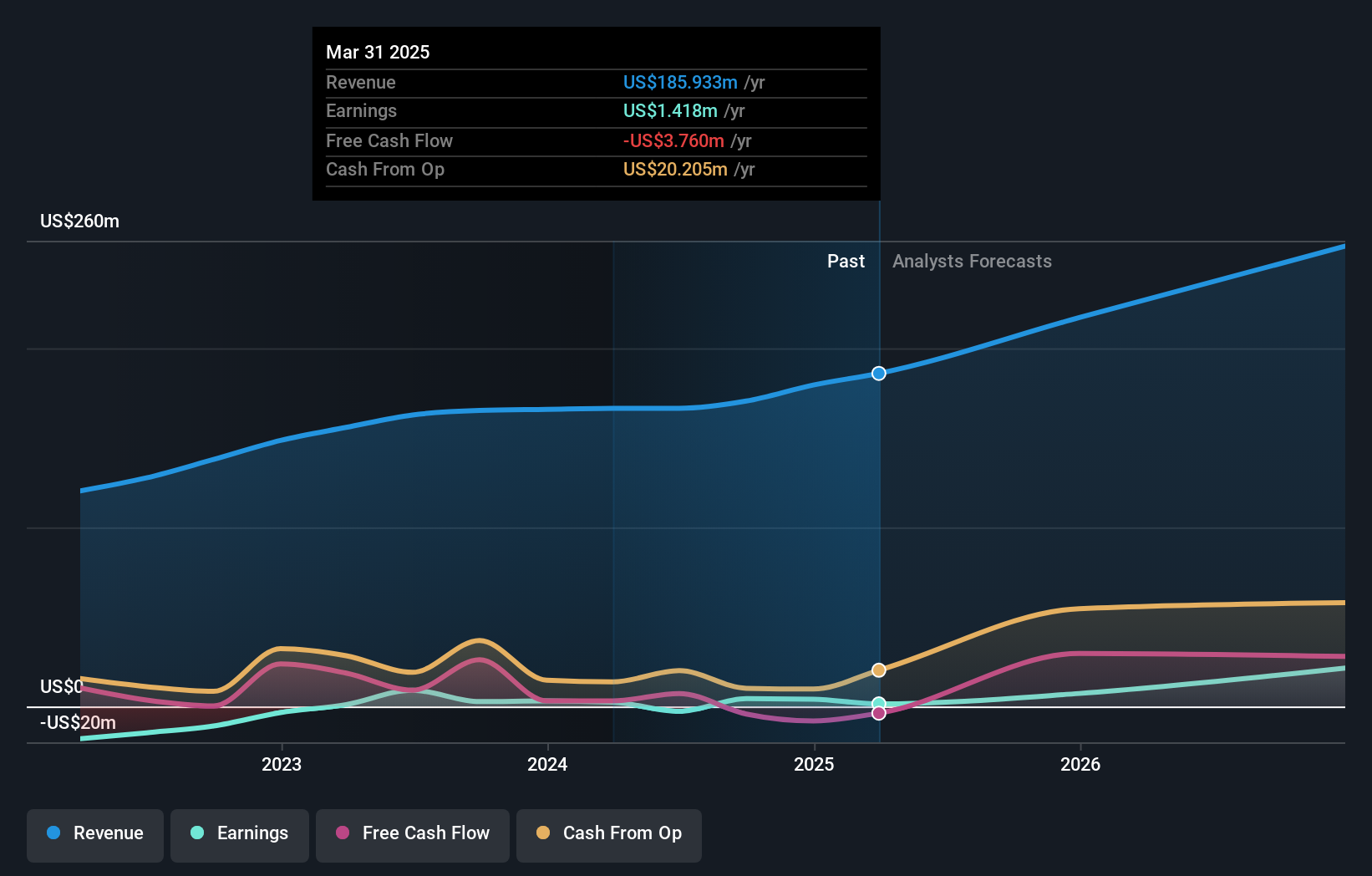

Estée Lauder Companies (EL)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: The Estée Lauder Companies Inc. is a global manufacturer and marketer of skincare, makeup, fragrance, and hair care products with a market cap of approximately $30.55 billion.

Operations: The company's revenue is primarily derived from skin care at $7.19 billion, followed by makeup at $4.25 billion, fragrance at $2.72 billion, and hair care products contributing $566 million.

Insider Ownership: 11.3%

Earnings Growth Forecast: 34.4% p.a.

Estée Lauder is forecasted to achieve profitability within three years, with earnings expected to grow by 34.37% per year, indicating robust growth potential. However, its revenue growth of 3.4% annually lags behind the market average. The company trades at a significant discount to its estimated fair value and has been added to several Russell Growth Benchmarks, highlighting its market relevance despite high debt levels and a dividend not fully covered by earnings. Recent merger talks with Puig ended due to valuation disagreements, underscoring Estée Lauder's strategic focus on maintaining financial discipline in acquisitions.

Where To Now?

- Explore the 172 names from our Fast Growing US Companies With High Insider Ownership screener here.

- Seeking Other Investments? Uncover the next big thing with financially sound penny stocks that balance risk and reward.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.