3 Large Cap Dividend Stocks Built For Higher Interest Rates

Progressive Corporation PGR | 0.00 |

With the Federal Reserve signaling that interest rates could stay higher for longer, income focused investors are rethinking where they look for dependable cash flow. At the same time, solid corporate earnings reports and ongoing U.S. China trade tensions are pulling the market in different directions. In this article, the spotlight is on large-cap dividend stocks that may be positioned to handle elevated borrowing costs and global supply chain friction. Below, you will find 3 dividend payers from our Large-Cap Dividend Stocks screener that appear more directly exposed to these crosscurrents, and why that may matter for your portfolio decisions.

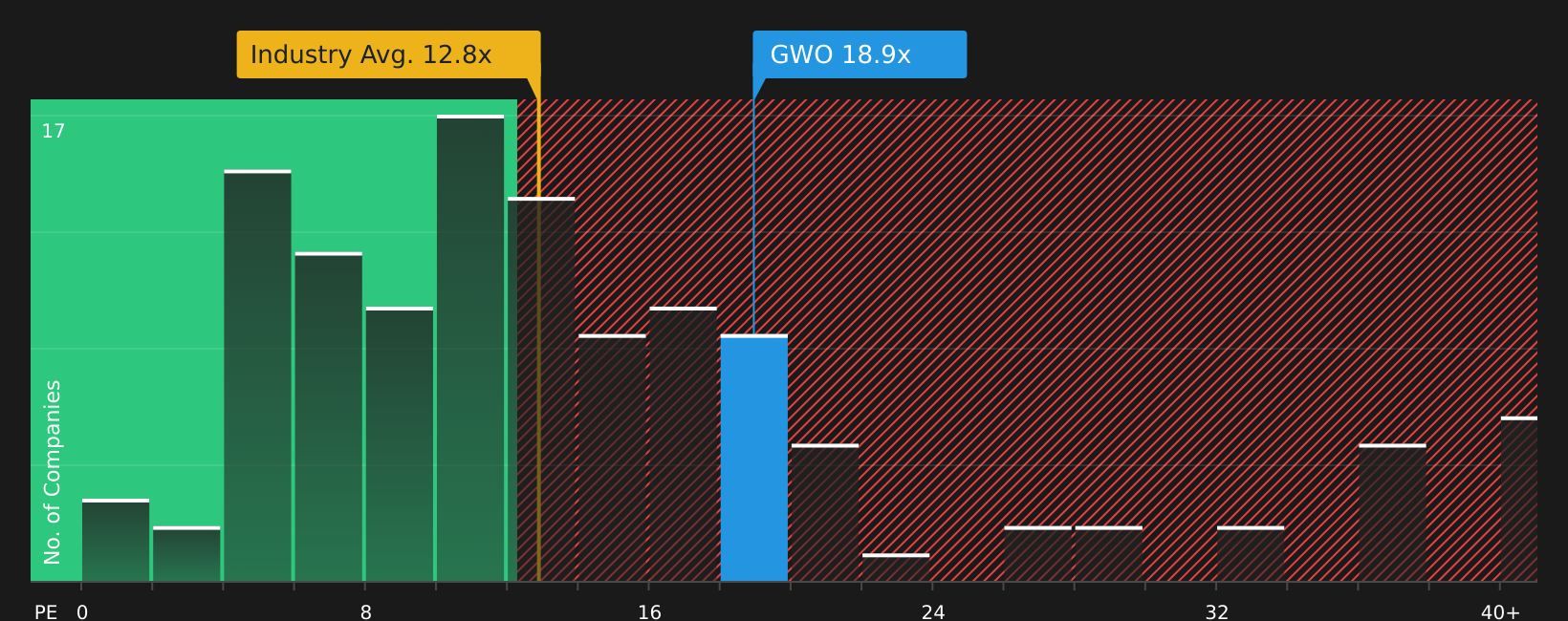

Great-West Lifeco (TSX:GWO)

Overview: Great-West Lifeco is a Canadian financial group that provides life and health insurance, retirement savings products, wealth and asset management, and reinsurance services across Canada, the United States, and Europe under brands such as Empower, Canada Life, and Irish Life.

Operations: Great-West Lifeco generates most of its revenue from Canada (CA$12.3b), followed by Europe (CA$8.5b), the United States (CA$6.0b), and its Capital and Risk Solutions segment (CA$5.5b), with a smaller Corporate contribution (CA$0.5b).

Market Cap: CA$79.4b

Income focused investors may want to pay attention to Great-West Lifeco because it combines a long established dividend record and a diversified earnings base with exposure to higher interest rates through its large fixed income portfolios. The company is leaning into fee based retirement and wealth management businesses that can provide steadier cash flow. In addition, share buybacks and preferred share issuance show active capital management. At the same time, a premium P/E relative to many insurance peers, reliance on external borrowings, and pressure from fee competition in retirement products are important watchpoints. For investors weighing higher for longer rates and trade related uncertainty, Great-West Lifeco offers a mix of income, scale, and risk factors that deserves a closer look.

Great-West Lifeco’s mix of long running dividends, fee based retirement income, and fixed income exposure could be masking a more interesting story about where returns really come from. Review the analysis report for Great-West Lifeco to see what might be hiding in plain sight.

Progressive (PGR)

Overview: Progressive is one of the largest U.S. insurers, focused on auto, specialty vehicles, and personal residential policies, selling coverage directly to consumers and through independent agents, with roots dating back to 1937.

Operations: Progressive generates most of its revenue from Personal Lines including property at about US$73.5b, with roughly US$10.9b from Commercial Lines and a US$5.0b segment adjustment, all from U.S. customers.

Market Cap: US$131.1b

Investors looking at large cap dividend stocks may find Progressive interesting because it sits at the intersection of higher-for-longer interest rates and data driven underwriting. The company benefits from sizable investment income in a rising rate setting, a high 36.1% ROE, and a long history of using analytics and telematics to adjust pricing quickly as inflation, tariffs, or supply chain shifts affect claim costs. At the same time, earnings are forecast to decline over the next few years, the dividend track record is uneven, and there has been meaningful insider selling alongside a funding model that relies on external borrowing. For investors weighing these trade offs, Progressive’s combination of earnings power, technology driven efficiency, and risk factors warrants a closer look before making a decision.

Progressive’s mix of high 36.1% ROE and data driven pricing is impressive, but the real story may sit in how those strengths stack up against uneven dividends and borrowing reliance in the 2 key rewards and 3 important warning signs (1 is major!)

Sun Life Financial (TSX:SLF)

Overview: Sun Life Financial is a global financial services company founded in 1871 that offers life and health insurance, retirement savings, wealth management, and asset management solutions for individuals and institutions across North America, Asia, and several other international markets.

Operations: Sun Life Financial generates revenue primarily from the U.S. at CA$13.7b, Canada at CA$11.9b, Sun Life Asset Management at CA$6.9b, Asia at CA$2.7b, with CA$0.4b from Corporate and a CA$0.7b consolidation adjustment.

Market Cap: CA$61.2b

Sun Life Financial operates in a higher rate setting and combines a long running dividend, exposure to benefit from elevated interest rates, and expanding fee based businesses in Asia and asset management. This comes at a time when investors are focusing on steady income rather than quick gains. Management highlights a diversified mix that can help handle inflation through pricing actions and cost controls. However, recent earnings have declined, margins are under pressure, and U.S. Dental and Medicaid exposure, funding risk from reliance on external borrowing, and a premium P/E relative to insurance peers all require careful attention. For investors weighing income, valuation signals, and the trade off between growth ambitions and balance sheet risk, there is more to Sun Life’s story than the headline dividend suggests.

Sun Life Financial’s mix of higher rate exposure, Asia and asset management growth, and recent margin pressure hints at a story investors have not fully pieced together yet. Walk through the full narrative for Sun Life Financial and see what could change the script next.

The 3 stocks in this article are just a starting point, as the full Large-Cap Dividend Stocks screener on Simply Wall St surfaces 32 more companies with similarly detailed income narratives and risk reward profiles through the Large-Cap Dividend Stocks screener. Use the Simply Wall St platform to identify, analyze, and filter for the specific catalysts, dividend histories, balance sheet strength, and volatility profiles that match your highest conviction ideas.

Take Control of Your Investment Journey

If Progressive or any of these companies sound like a great opportunity, register for FREE with Simply Wall St and add your companies to a Watchlist to monitor the share price against the fair value the ideal entry point. Once you've made your move, manage your holdings with our Portfolio Command Center that filters out the noise to deliver only the most critical, actionable updates. Throughout your journey, our Community allows you to filter the best ideas from thousands of investor perspectives. By uncovering hidden catalysts and risks early, you'll accelerate your decision-making and stay one step ahead of the market.

Seeking Fresh Alternatives Before Others Catch On?

Markets move fast, and the next breakout ideas rarely stay under the radar for long. Scan these fresh stock sets before momentum is fully caught and consider your options.

- Explore income opportunities that continue working while rates stay elevated by scanning a curated set of higher yielding companies through the 6 dividend fortresses.

- Look for early movers in artificial intelligence infrastructure by tracking hand picked enablers of data centers and compute demand inside the 52 AI infrastructure stocks.

- Review select miners and producers screened in the 33 elite gold producer stocks if you are evaluating potential exposure to commodity-related strategies.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.