3 Penny Stocks With Strong Balance Sheets Worth A Closer Look

Grab Holdings GRAB | 0.00 |

Global markets are wrestling with higher oil prices, sticky inflation signals, and rising bond yields, which puts real pressure on weaker companies that rely heavily on cheap money to survive. That is exactly why the Elite Penny Stocks screener focuses on balance sheet strength, not just hype. By filtering for smaller stocks that still have the cash and financial resilience to pursue their growth plans, this approach narrows the field to companies that can keep investing even as borrowing costs remain elevated. In this article, you will see 3 stocks from that Elite Penny Stocks list.

Yatsen Holding (YSG)

Overview: Yatsen Holding is a Guangzhou based beauty company that develops and sells color cosmetics, skincare, and related beauty tools across China through both online channels and physical stores, using brands such as Perfect Diary, Little Ondine, Pink Bear, Galénic, DR.WU, Eve Lom, and EANTiM.

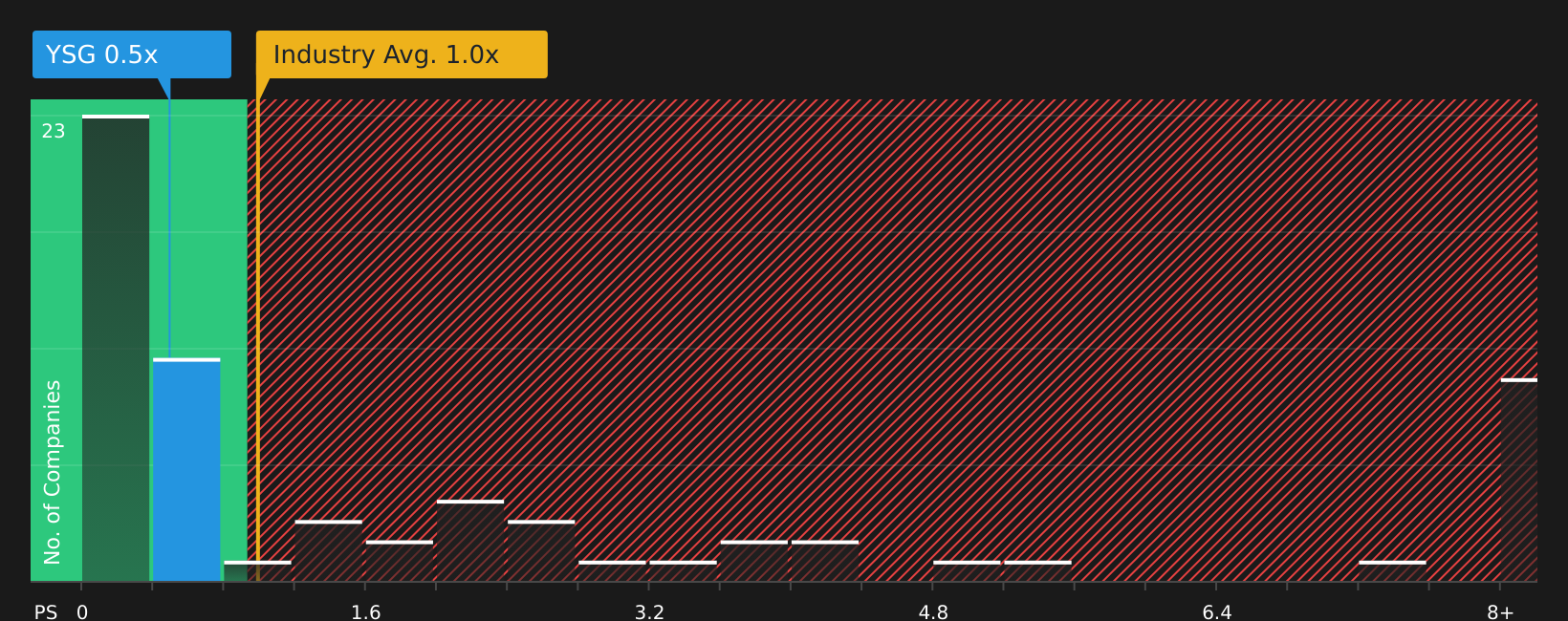

Operations: Yatsen generates all of its reported CN¥4.5b in revenue in the People’s Republic of China.

Market Cap: US$0.33b

Yatsen Holding provides exposure to China's beauty market through a mix of fast moving color cosmetics and higher margin skincare, supported by digital sales growth, omni channel distribution, and ongoing product development. Analysts have highlighted earnings growth potential, and the current P/S of around 0.5x indicates the stock is priced more cautiously than many US personal products peers. At the same time, the company is still loss making, with Q1 2026 net loss widening to CN¥60.5m, and it relies on external funding, while competition and high marketing spend pose clear risks. That combination of evolving fundamentals, active share buybacks, and execution challenges makes Yatsen a stock that some investors may choose to monitor closely within a quality focused penny stock shortlist.

Yatsen Holding’s cautious P/S and active buybacks hint at a story investors might be underestimating, so walk through the 3 key rewards and 1 important warning sign that could explain whether the widened loss is a setback or a reset

Grab Holdings (GRAB)

Overview: Grab Holdings runs a superapp across eight Southeast Asian countries that brings together ride hailing, food and parcel delivery, digital payments, lending, insurance, and banking services for tens of millions of users and merchants. By combining everyday transport and food orders with GrabPay, GrabFin, and digital bank products, the company aims to be a daily utility for both consumers and small businesses.

Operations: Grab generates most of its revenue from Deliveries at about US$1.9b and Mobility at about US$1.3b, with smaller contributions from Financial Services at about US$0.4b and Other revenue of about US$4m.

Market Cap: US$15.7b

Grab Holdings gives you direct exposure to Southeast Asia’s digital economy through a business that is already profitable, with recent net profit margins around 10.7% and quarterly net income of US$136m on US$955m of revenue. The superapp model, expanding into areas like digital banking with Superbank and higher margin advertising, sits alongside a sizeable cash position and analyst expectations for earnings growth. The current P/E of 42.3x means you are paying a relatively high multiple for that story. On the risk side, heavy use of external borrowing, thin GAAP margins, and an evolving board track record mean execution quality is important. What investors do not see at a glance is how all of these moving parts interact with regulatory questions and potential consolidation across the region.

Grab Holdings has an accelerating superapp story, but the real tension is whether current profits and a 42.3x P/E are justified by what comes next, so walk through the full analyst forecasts for Grab Holdings before one crucial piece of the puzzle comes into focus

Clover Health Investments (CLOV)

Overview: Clover Health Investments runs Medicare Advantage plans for eligible US seniors and offers PPO and HMO products supported by Clover Assistant, a clinical software platform that helps doctors spot and manage chronic conditions. Together, the insurance business and technology platform aim to improve care quality while keeping medical costs in check.

Operations: Clover Health Investments generates about US$2.2b in revenue from its Insurance segment, all from customers in the United States.

Market Cap: US$2.7b

Clover Health Investments stands out on the Elite Penny Stocks screener because it combines a technology led Medicare Advantage model, a 4.5 star CMS rating that supports higher reimbursements, and recent membership and revenue momentum with a valuation signal that screens as undervalued on Simply Wall St’s estimate of fair value. At the same time, the company is still reporting GAAP losses, carries funding risk from reliance on external borrowing, and faces pressure from rising medical costs and powerful national competitors. That mix of revenue growth, changing operating metrics, and ongoing profitability and policy risk is one reason some investors are watching Clover closely rather than writing it off or assuming the recent share price strength will automatically continue.

Clover Health Investments appears to be a Medicare growth story hiding inside a loss-making insurer, so walk through the analyst forecasts for Clover Health Investments to see how its 4.5 star rating could collide with policy and cost pressures next

The 3 stocks in this article are just a sample of what the full Elite Penny Stocks idea turns up, with the screener pinpointing 17 more companies that pair strong balance sheets with equally compelling growth narratives inside the Elite Penny Stocks screener. Use Simply Wall St to identify and analyze the specific catalysts, cash runways, and business narratives that matter to you so you can focus on the highest conviction opportunities in this corner of the market.

Take Control of Your Investment Journey

If Clover Health Investments or any of these companies have caught your attention, register for FREE with Simply Wall St and add your companies to a Watchlist to monitor the share price against the fair value and track any new developments as they happen. Once you've made your move, manage your holdings with our Portfolio Command Center that filters out the noise to deliver only the most critical, actionable updates. Throughout your journey, our Community allows you to filter the best ideas from thousands of investor perspectives. By uncovering hidden catalysts and risks early, you'll accelerate your decision-making and stay one step ahead of the market.

Seeking Alternatives Before Momentum Flies Past?

Fresh stock ideas can move from quiet to breakout quickly, and once momentum is flying, the most accessible entry window may be limited. Consider these under the radar picks before potential opportunities become harder to reach.

- Explore resilient compounding by scanning a curated 74 resilient stocks with low risk scores that prioritizes stronger balance sheets so you are not caught holding more fragile stocks if conditions tighten.

- Identify early leaders in wealth building with a focused 9 dividend fortresses that highlights companies offering higher yields while prices may still be lower or attracting less attention.

- Monitor the backbone of future electrification through a targeted 36 power grid technology and infrastructure stocks to find businesses involved in grid upgrades before they draw broader market attention.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.