3 Promising Growth Companies With Insider Ownership Up To 20%

Upstart UPST | 33.36 34.08 | +12.97% +2.16% Pre |

The United States market has shown robust performance, with a 3.0% rise over the last week and a 26% increase over the past year, while earnings are anticipated to grow by 16% annually in the coming years. In this thriving environment, growth companies with significant insider ownership can be particularly appealing as they often reflect strong confidence from those closest to the business.

Top 10 Growth Companies With High Insider Ownership In The United States

| Name | Insider Ownership | Earnings Growth |

| Upstart Holdings (UPST) | 13% | 53.5% |

| Precigen (PGEN) | 11.9% | 68.4% |

| Karman Holdings (KRMN) | 17.2% | 53.2% |

| GBank Financial Holdings (GBFH) | 27.3% | 42.2% |

| Clene (CLNN) | 13.2% | 62.2% |

| Caledonia Mining (CMCL) | 14.3% | 28.4% |

| Better Home & Finance Holding (BETR) | 20.6% | 97.4% |

| AST SpaceMobile (ASTS) | 27.9% | 109.4% |

| Astera Labs (ALAB) | 10.3% | 29.0% |

| AppLovin (APP) | 27.3% | 21.4% |

Here we highlight a subset of our preferred stocks from the screener.

Webull (BULL)

Simply Wall St Growth Rating: ★★★★★☆

Overview: Webull Corporation operates as a digital investment platform with a market cap of $2.59 billion.

Operations: The company generates revenue primarily from its brokerage segment, amounting to $571 million.

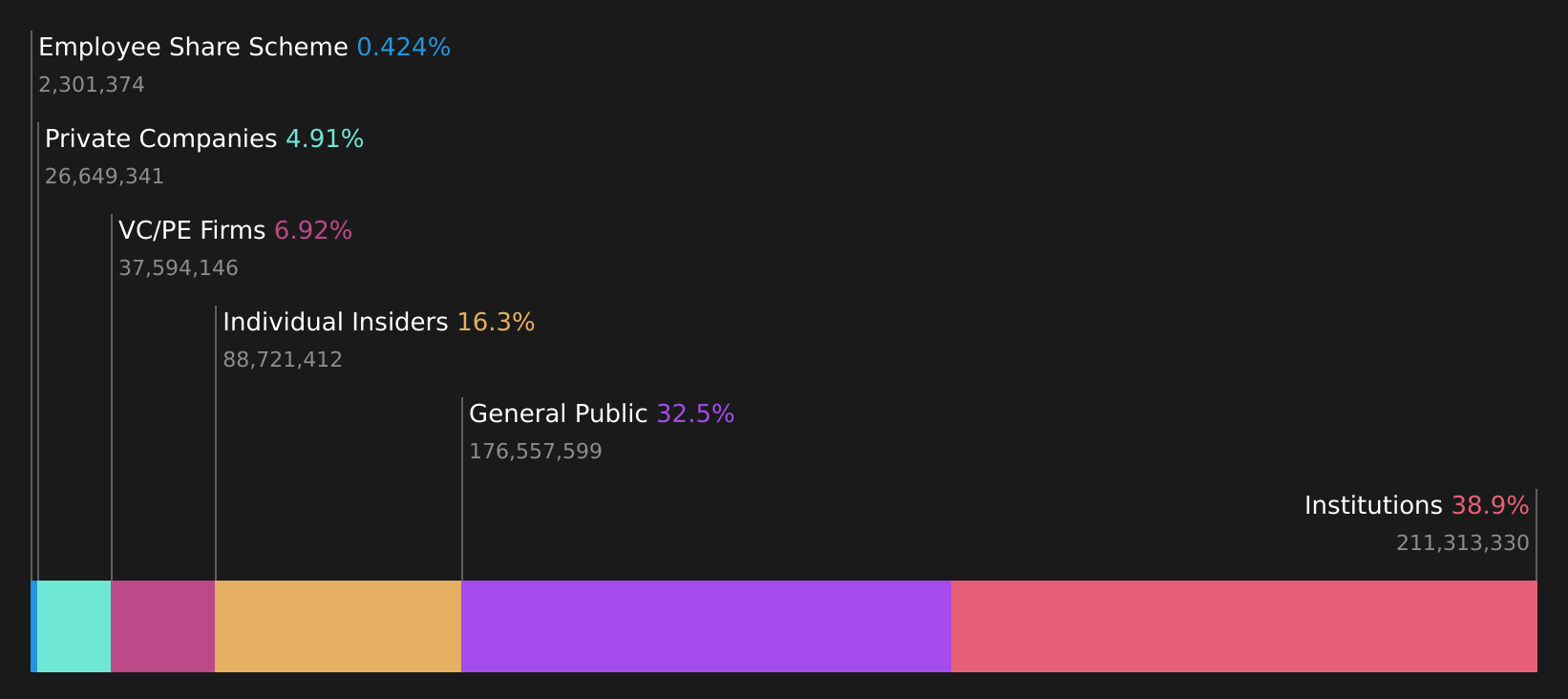

Insider Ownership: 20.1%

Webull's focus on digital asset trade surveillance through its partnership with Solidus Labs aligns with its rapid global expansion, serving over 26 million users. Despite significant revenue growth of US$571 million in 2025, net income decreased to US$3.04 million in Q4. The company's innovative offerings like prediction markets and automated trading tools strengthen its retail platform. Forecasts indicate strong revenue growth at 21.1% annually, outpacing the broader US market's expected growth rate.

PDF Solutions (PDFS)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: PDF Solutions, Inc. offers proprietary software, physical intellectual property for integrated circuit designs, electrical measurement hardware tools, methodologies, and professional services globally with a market cap of $1.37 billion.

Operations: The company's revenue primarily comes from its Software & Programming segment, which generated $219.02 million.

Insider Ownership: 11%

PDF Solutions, Inc. demonstrates strong growth potential with insider ownership aligning interests between management and shareholders. Despite a net loss of US$0.64 million for 2025, the company reported significant revenue growth to US$219.02 million from US$179.47 million the previous year. Forecasts suggest an annual profit growth above market averages as PDF Solutions aims for profitability within three years, supported by expected revenue increases faster than the broader US market's 10.4% annual rate.

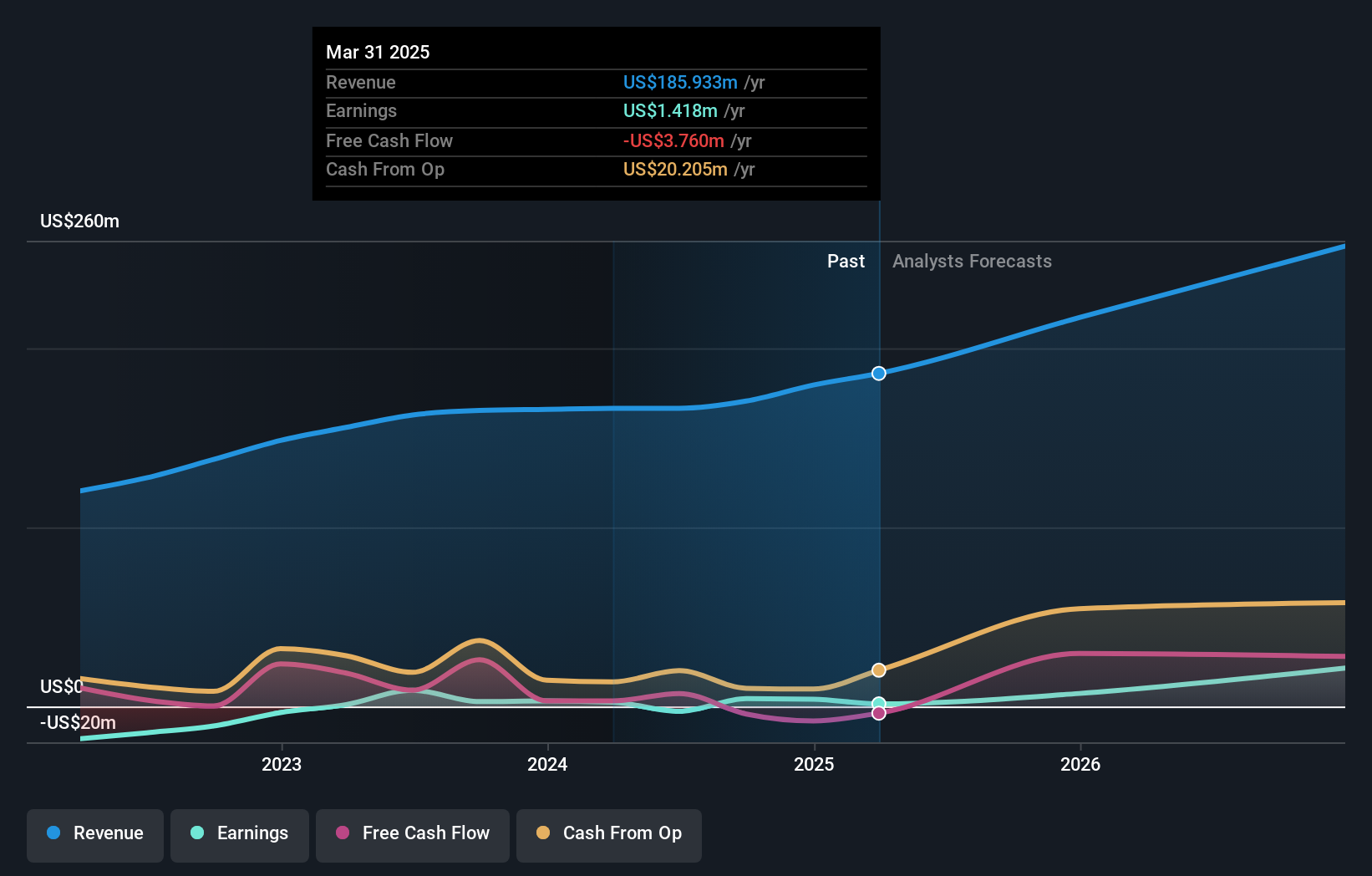

Upstart Holdings (UPST)

Simply Wall St Growth Rating: ★★★★★★

Overview: Upstart Holdings, Inc. operates a cloud-based AI lending platform in the United States and has a market capitalization of approximately $2.51 billion.

Operations: The company's revenue is primarily generated from its personal lending segment, which amounts to $929.22 million.

Insider Ownership: 13%

Upstart Holdings, despite facing legal challenges and insider selling, shows strong growth potential with forecasted revenue and earnings growth significantly outpacing the US market. The company's AI-driven lending platform continues to expand with new partnerships like DuPage Credit Union. However, recent lawsuits allege misleading statements about their AI model's performance, impacting revenue forecasts. Upstart is also pursuing a national bank charter to streamline operations and reduce costs while maintaining substantial insider ownership aligning management interests with shareholders.

Taking Advantage

- Click this link to deep-dive into the 209 companies within our Fast Growing US Companies With High Insider Ownership screener.

- Contemplating Other Strategies? Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.