3 Stocks That May Be Trading Below Their Estimated Value By Up To 49.7%

Waters Corporation WAT | 0.00 |

The United States market has shown positive momentum, rising 1.6% over the last week and 19% over the past year, with earnings projected to grow by 18% annually. In such a robust environment, identifying stocks that may be trading below their estimated value can offer investors potential opportunities for growth and value appreciation.

Top 10 Undervalued Stocks Based On Cash Flows In The United States

| Name | Current Price | Fair Value (Est) | Discount (Est) |

| Rayonier (RYN) | $21.49 | $42.86 | 49.9% |

| Q2 Holdings (QTWO) | $52.63 | $103.09 | 48.9% |

| Procore Technologies (PCOR) | $43.97 | $86.98 | 49.4% |

| Natera (NTRA) | $279.32 | $554.60 | 49.6% |

| Klaviyo (KVYO) | $16.90 | $33.62 | 49.7% |

| Janus Living (JAN) | $29.12 | $57.58 | 49.4% |

| Gold Royalty (GROY) | $2.86 | $5.69 | 49.7% |

| Esquire Financial Holdings (ESQ) | $120.34 | $238.84 | 49.6% |

| Beacon Financial (BBT) | $30.22 | $60.42 | 50% |

| Amaroq (AMRQ.F) | $1.112 | $2.21 | 49.8% |

We'll examine a selection from our screener results.

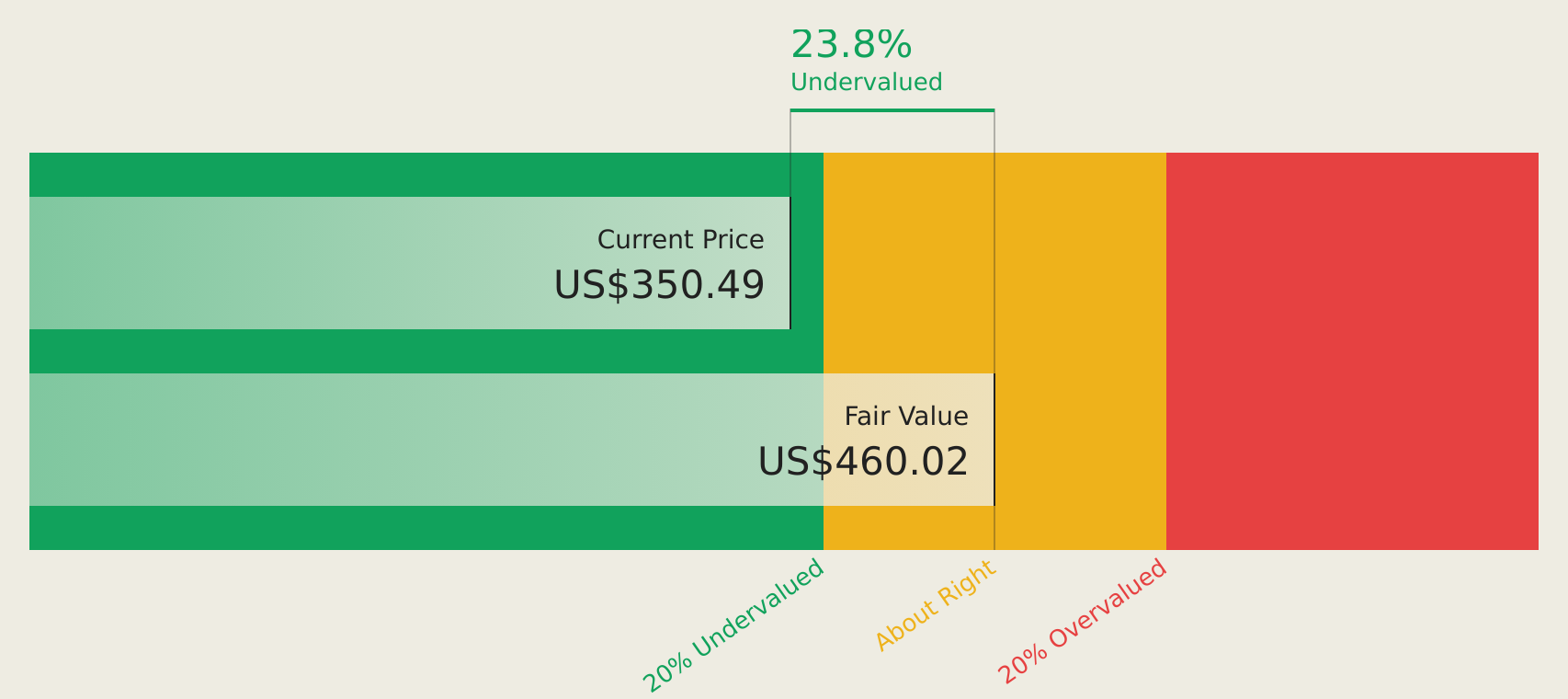

Li Auto (LI)

Overview: Li Auto Inc. operates in the energy vehicle market in the People’s Republic of China with a market cap of approximately $12.07 billion.

Operations: The company generates revenue from its Auto Manufacturers segment, which amounted to CN¥109.37 billion.

Estimated Discount To Fair Value: 13.7%

Li Auto, trading at US$12.02, is considered undervalued based on its discounted cash flow analysis with an estimated value of US$13.93. Despite a current net loss of CNY 2.29 billion in Q1 2026, Li Auto's earnings are projected to grow significantly at 61.74% annually and become profitable within three years, outpacing average market growth. Recent vehicle deliveries reached nearly 1.73 million units year-to-date by June-end, supporting future revenue expansion forecasts of 13% annually.

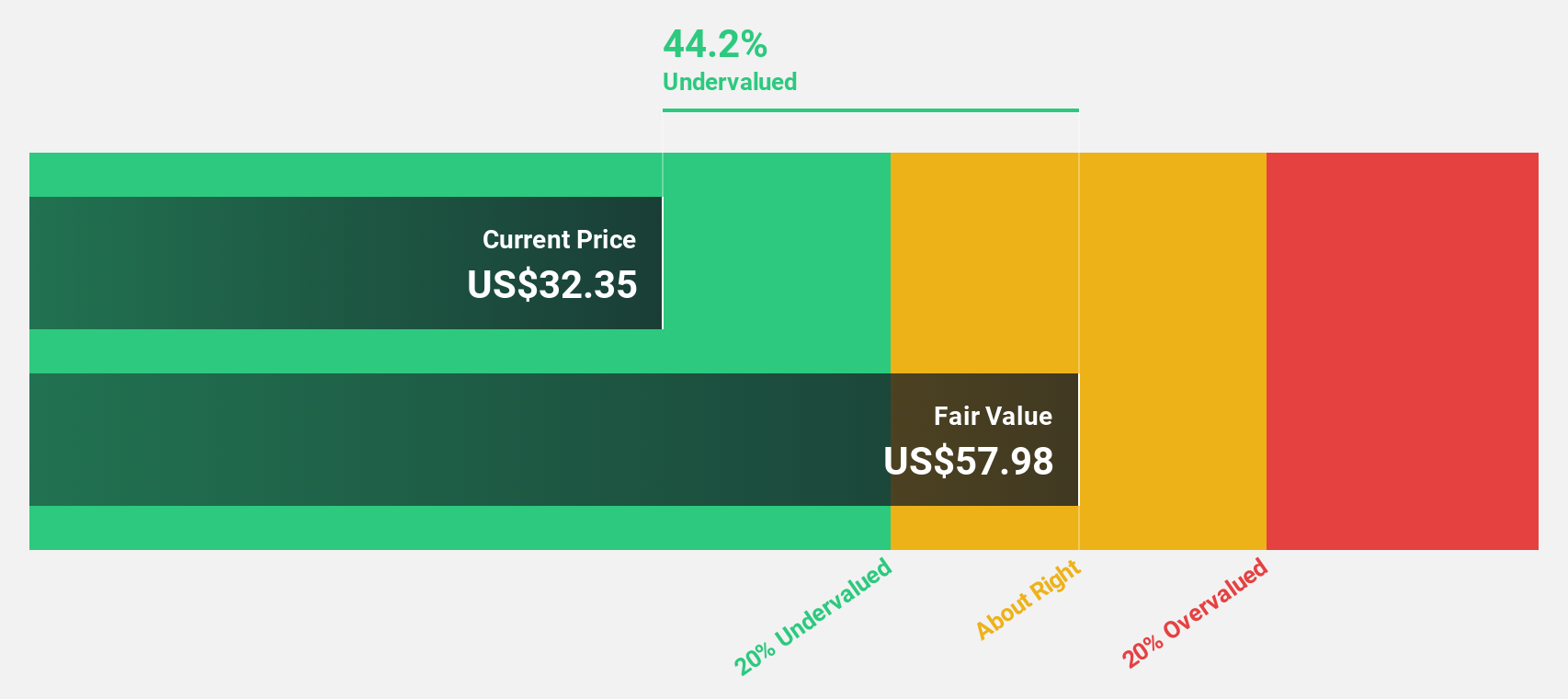

Klaviyo (KVYO)

Overview: Klaviyo, Inc. offers a cloud-based software-as-a-service platform across various regions including the Americas, Asia-Pacific, Europe, the Middle East, and Africa with a market cap of approximately $5.06 billion.

Operations: The company's revenue is primarily derived from its Internet Software segment, which generated $1.31 billion.

Estimated Discount To Fair Value: 49.7%

Klaviyo, trading at US$16.90, appears undervalued with its discounted cash flow value estimated at US$33.62. The company reported Q1 2026 sales of US$358 million and net income of US$9.04 million, marking a turnaround from the previous year's loss. Recent strategic partnerships and AI advancements enhance its CRM capabilities, supporting future growth prospects despite high share price volatility over the past three months and revenue growth forecasted below 20% annually.

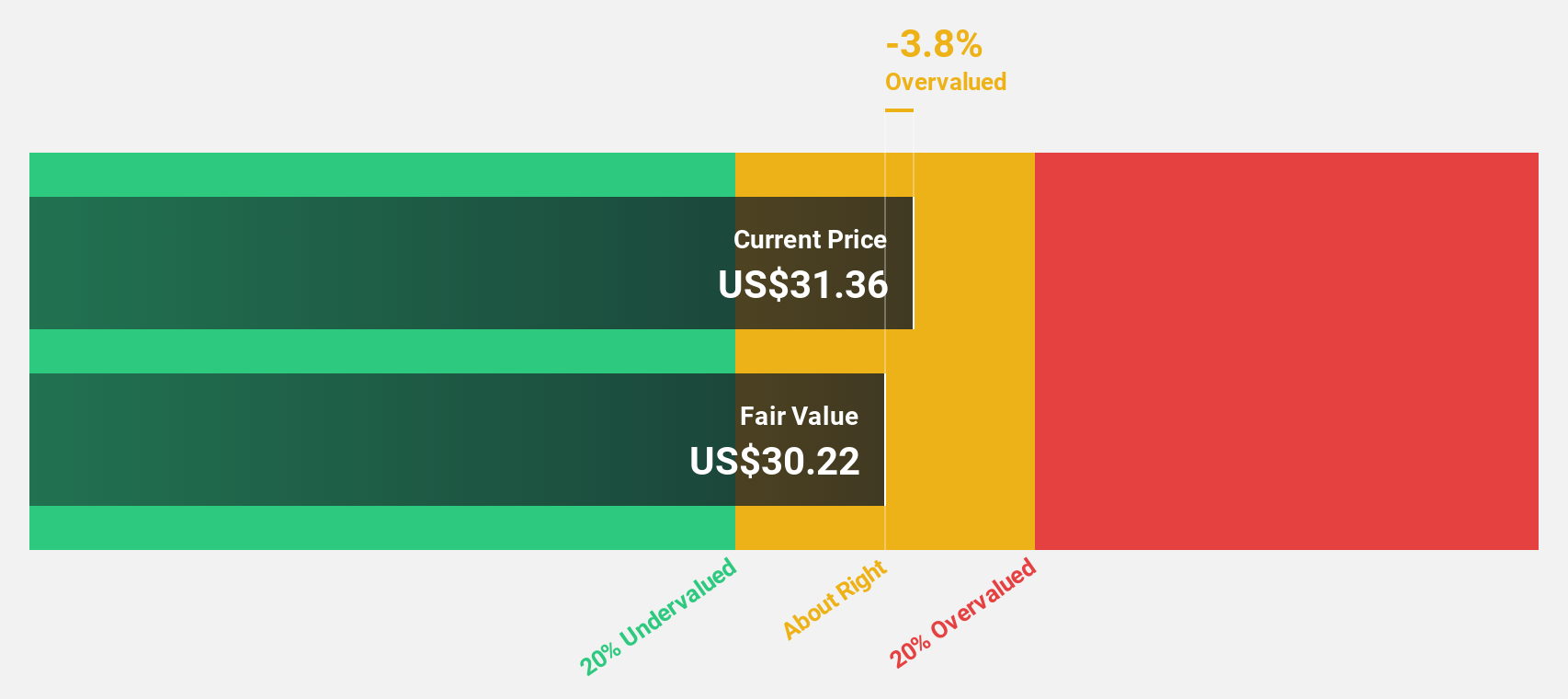

Waters (WAT)

Overview: Waters Corporation offers analytical workflow solutions across Asia, the Americas, and Europe with a market cap of approximately $37.24 billion.

Operations: The company's revenue segments include Waters Division with $2.59 billion and TA Instruments with $0.31 billion.

Estimated Discount To Fair Value: 23.2%

Waters, priced at US$379.29, is trading below its estimated future cash flow value of US$493.69 and 23.2% under its fair value estimate. Despite recent index exclusions and shareholder dilution, Waters' earnings are forecast to grow significantly at 25.3% annually, outpacing the US market's growth rate. Recent strategic acquisitions and partnerships in diagnostics and AI-powered platforms bolster its revenue growth prospects, although profit margins have declined from last year’s figures.

Summing It All Up

- Delve into our full catalog of 149 Undervalued US Stocks Based On Cash Flows here.

- Got skin in the game with these stocks? Elevate how you manage them by using Simply Wall St's portfolio, where intuitive tools await to help optimize your investment outcomes.

- Join a community of smart investors by using Simply Wall St. It's free and delivers expert-level analysis on worldwide markets.

Ready For A Different Approach?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.