3 Undervalued Small Caps With Notable Insider Buying Activity

Azenta, Inc. AZTA | 0.00 |

Over the last 7 days, the United States market has risen by 1.3%, contributing to a notable 28% climb over the past year, with earnings expected to grow by 17% annually. In this context of robust market performance, identifying stocks that are both undervalued and have significant insider buying can be an effective strategy for investors seeking opportunities in small-cap companies.

Top 10 Undervalued Small Caps With Insider Buying In The United States

| Name | PE | PS | Discount to Fair Value | Value Rating |

|---|---|---|---|---|

| First United | 9.8x | 2.8x | 45.84% | ★★★★★☆ |

| Financial Institutions | 9.1x | 3.0x | 29.99% | ★★★★★☆ |

| Angel Oak Mortgage REIT | 13.0x | 5.9x | 25.24% | ★★★★★☆ |

| AVITA Medical | NA | 1.8x | 49.12% | ★★★★★☆ |

| First Bancorp | 9.0x | 3.4x | 30.35% | ★★★★☆☆ |

| New Peoples Bankshares | 8.8x | 2.3x | 37.32% | ★★★★☆☆ |

| German American Bancorp | 12.1x | 4.4x | 44.56% | ★★★☆☆☆ |

| Bank of the James Financial Group | 9.5x | 2.1x | 40.48% | ★★★☆☆☆ |

| Union Bankshares | 9.4x | 2.0x | 19.78% | ★★★☆☆☆ |

| Angel Studios | NA | 1.3x | -44.18% | ★★★☆☆☆ |

Let's take a closer look at a couple of our picks from the screened companies.

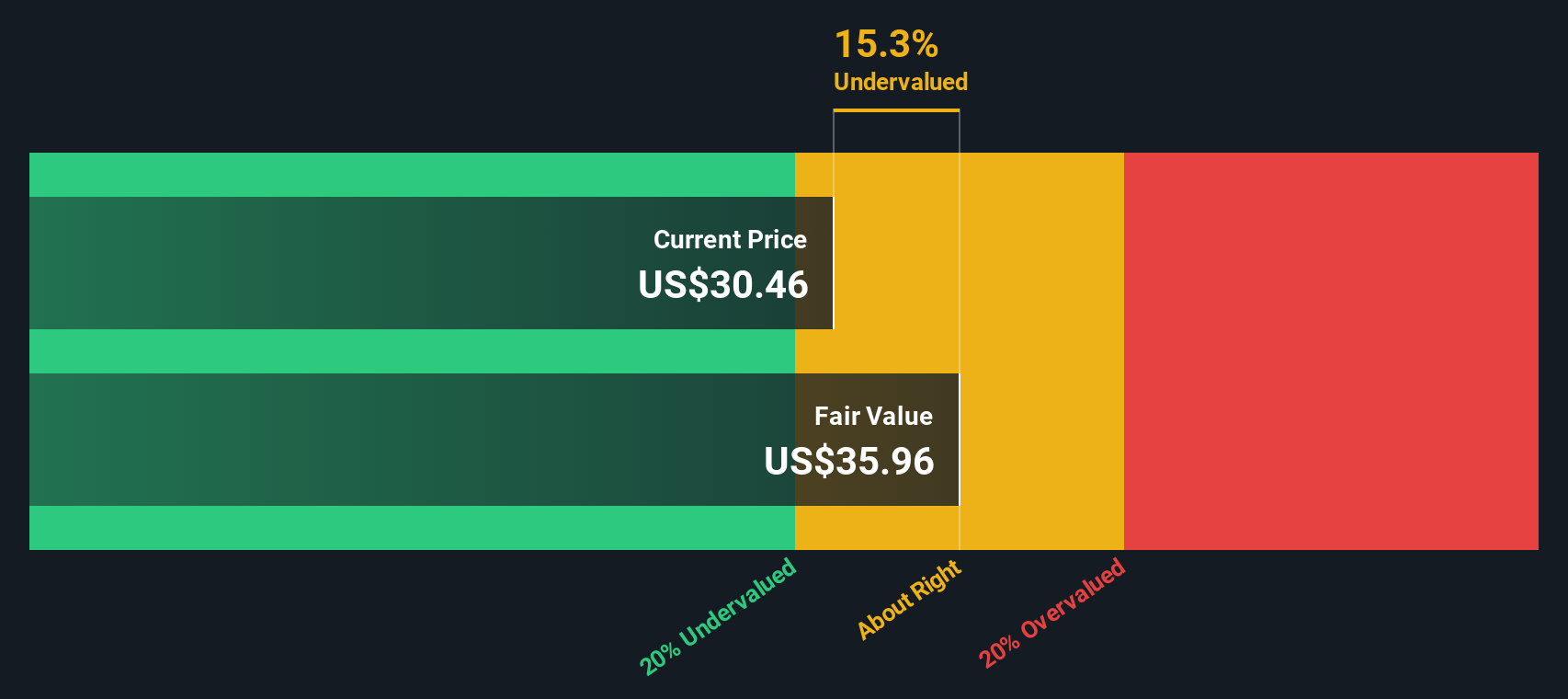

Azenta (AZTA)

Simply Wall St Value Rating: ★★★★★☆

Overview: Azenta is a company specializing in multiomics and sample management solutions, with a market cap of approximately $4.51 billion.

Operations: Azenta generates revenue primarily through its Multiomics and Sample Management Solutions segments, with recent revenues of $270.33 million and $326.15 million respectively. The company's gross profit margin has shown variation, reaching 45.52% in the latest quarter ending September 2025, before decreasing to 44.33% by March 2026. Operating expenses are a significant component of costs, with General & Administrative expenses consistently being the largest portion within this category over time.

PE: -8.9x

Azenta, a company with a focus on scaling global synthesis capabilities, has recently filed a US$51.07 million Shelf Registration for common stock. Despite reporting Q2 revenue of US$144.8 million, Azenta faced significant impairment charges of US$149.08 million and net losses of US$160.8 million for the quarter ending March 31, 2026. With no recent share repurchases, insider confidence is not currently highlighted by purchases in this period. The appointment of Trey Martin as President aims to drive growth in their Multiomics business amidst expectations of revenue between US$603-621 million for fiscal year ending September 30, 2026.

Kronos Worldwide (KRO)

Simply Wall St Value Rating: ★★★☆☆☆

Overview: Kronos Worldwide operates in the production and sale of titanium dioxide pigments, with a market capitalization of approximately $1.33 billion.

Operations: The company's revenue primarily stems from the production and sale of titanium dioxide pigments, with recent quarterly revenues reaching approximately $1.88 billion. Over time, gross profit margins have shown fluctuations, most recently recorded at 10.29% for the quarter ending March 31, 2026. The cost of goods sold consistently represents a significant portion of expenses, impacting profitability metrics such as net income margin which was -7.12% in the same period.

PE: -6.3x

Kronos Worldwide, a company with sales of US$509.8 million in Q1 2026, faces challenges with a net loss of US$4.8 million compared to last year's profit. Despite these hurdles, insider confidence is shown by Bart Reichert's purchase of 20,000 shares for US$99,200 in March 2026. The firm declared a quarterly dividend of $0.05 per share and has completed share repurchases worth US$10.21 million since December 2010, highlighting strategic financial maneuvers amidst earnings pressure and reliance on external borrowing for funding needs.

TriNet Group (TNET)

Simply Wall St Value Rating: ★★★☆☆☆

Overview: TriNet Group provides staffing and outsourcing services, with a market cap of approximately $5.37 billion.

Operations: TriNet Group's primary revenue stream is derived from its Staffing & Outsourcing Services, generating $4.88 billion as of the latest period. The company experienced fluctuations in its gross profit margin, reaching a peak of 22.93% in June 2020 before declining to 17.29% by March 2026. Operating expenses have varied over time, with significant allocations towards sales and marketing and general and administrative costs.

PE: 12.6x

TriNet Group, a key player in HR solutions, shows potential as an undervalued stock. Despite a slight dip in Q1 2026 revenue to US$1.23 billion from US$1.29 billion the previous year, net income rose to US$89 million. The company forecasts steady earnings growth of 6.46% annually and has reiterated its revenue guidance for 2026 between US$4.75 billion and US$4.90 billion, with diluted EPS ranging from $2.15 to $3.05, indicating confidence in future performance despite reliance on external borrowing for funding needs.

Where To Now?

- Discover the full array of 71 Undervalued US Small Caps With Insider Buying right here.

- Shareholder in one or more of these companies? Ensure you're never caught off-guard by adding your portfolio in Simply Wall St for timely alerts on significant stock developments.

- Simply Wall St is your key to unlocking global market trends, a free user-friendly app for forward-thinking investors.

Curious About Other Options?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.