3 US Banking Stocks With Low P E Ratios And Buybacks

Banc of California, Inc. BANC | 0.00 |

The Federal Reserve’s latest policy shift puts borrowing costs and inflation expectations back at the center of every financial stock discussion. When rates and credit conditions move, banks and diversified financial firms often feel the impact quickly through lending margins, funding costs, and balance sheet valuations. This article looks at how that policy update might affect a select group of financial sector stocks with solid scores for value, health, and performance. You will see 3 stocks that appear positively exposed to this news event, along with practical context to help decide whether they deserve a closer look in your portfolio research.

CNB Financial (CCNE)

Overview: CNB Financial is a regional US banking group that offers everyday banking, mortgages, commercial lending, and consumer finance, alongside private banking and wealth management services for individuals, businesses, and institutions. Through CNB Bank, it also distributes annuities and insurance products, and manages trusts, estates, and retirement plans.

Operations: CNB Financial generates about US$300.3 million in revenue from its core banking activities, all within the United States.

Market Cap: US$942.9 million

CNB Financial stands out in this screener because its core business is tightly linked to US interest rates, so changes in Federal Reserve policy flow quickly through to lending margins, deposit costs, and earnings. Recent results show strong earnings growth and a net profit margin of 25.6%. The stock trades on a P/E below peers and at a large discount to some fair value estimates, which will catch the eye of value focused investors. In addition, the bank offers a 2.36% dividend yield, a recently announced buyback program, and has reduced subordinated debt, which together indicate a shareholder friendly stance. The flip side is a history of shareholder dilution and a modest 9.2% ROE, which are important to weigh against the apparent upside potential.

CNB Financial’s low P/E, 25.6% net margin and 2.36% yield suggest the market may be missing something, yet past dilution and a modest 9.2% ROE leave questions that the 4 key rewards and 1 important major warning sign

Midland States Bancorp (MSBI)

Overview: Midland States Bancorp is a US financial holding company that, through Midland States Bank, provides a wide range of banking, lending, equipment leasing, and wealth management services to individuals, businesses, and municipalities, with roots dating back to 1881 in Effingham, Illinois.

Operations: Midland States Bancorp generates about US$254.7 million from Banking and US$31.8 million from Wealth Management, with all US$274.5 million of revenue coming from customers in the United States.

Market Cap: US$610.1 million

Midland States Bancorp sits in a sweet spot for Fed driven shifts in borrowing costs, because its net interest margins and loan pricing are closely tied to policy moves, while it also earns fee income from wealth management. Recent results show a move back into profit after a large prior year loss, supported by higher average loan yields, tighter capital management and lower net charge offs. However, earnings have declined 45.4% per year over the past 5 years and ROE is a modest 6.3%. The stock screens as cheaper than many peers on P/E, offers a 4.35% dividend yield that is not fully covered by earnings, and is actively returning cash through buybacks. These factors may encourage income oriented investors to look more closely at the trade offs involved.

Midland States Bancorp’s mix of a 4.35% yield, buybacks, and a recent swing back to profit suggests that the headline numbers may not tell the full story, particularly when you also consider the 3 key rewards and 1 important warning sign

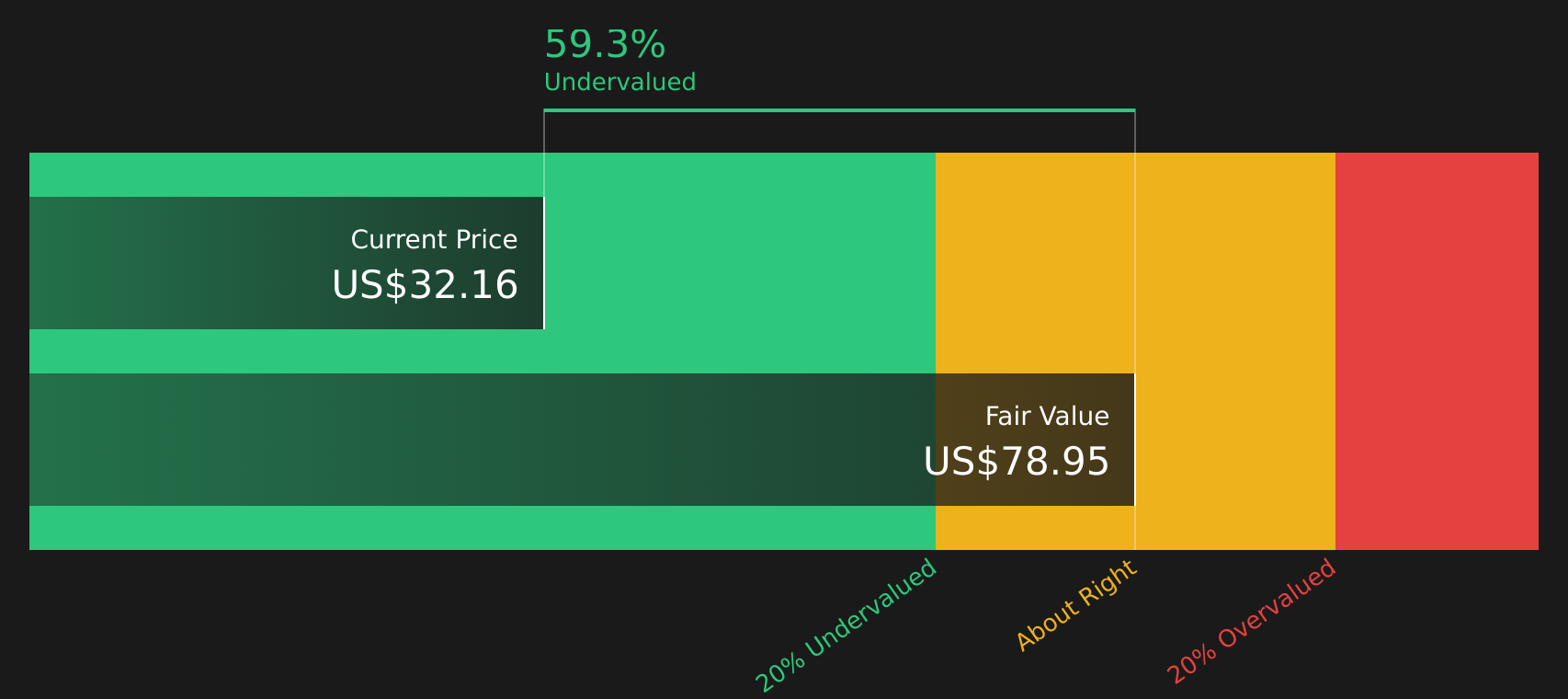

Banc of California (BANC)

Overview: Banc of California is a regional US bank that provides everyday banking, business lending, and treasury management services, with a focus on small and mid-sized businesses, private equity and venture firms, non-profits, and high net worth clients across California and selected US markets.

Operations: Banc of California generates about US$1.1b in revenue from Commercial Banking activities, entirely from customers in the United States.

Market Cap: US$3.1b

Banc of California gives you a way to consider Federal Reserve policy through a bank whose earnings are closely linked to loan pricing, deposit costs, and commercial activity in California, while also working through a large merger integration and an extended buyback plan. The combination of improving profitability, an active share repurchase program, and plans to redeem US$385m of subordinated notes shows a strong focus on capital management. However, investors still need to weigh heavy exposure to regional commercial real estate, integration risk from acquisitions, and an unstable dividend record. For investors tracking how the Fed’s latest shift could ripple through regional lenders, Banc of California is a stock that may merit closer attention.

Accelerating merger integration, a large buyback and plans to redeem US$385m of subordinated notes could be reshaping Banc of California’s risk reward profile in ways the headline story misses. Start with the 3 key rewards and 2 important warning signs.

The three financial stocks in this article are only a starting point, as the full Financial Sector Stocks screener surfaces 35 more companies with equally compelling narratives tied to interest rate exposure, balance sheet strength, and income potential. Use Simply Wall St to identify, filter, and analyze the specific catalysts that matter to you so you can focus on the highest conviction financial sector opportunities with clear, data driven narratives.

Take Control of Your Investment Journey

If CNB Financial or any of these companies sound like a great opportunity, register for FREE with Simply Wall St and add your companies to a Watchlist to monitor the share price against the fair value the ideal entry point. Once you've made your move, manage your holdings with our Portfolio Command Center that filters out the noise to deliver only the most critical, actionable updates. Throughout your journey, our Community allows you to filter the best ideas from thousands of investor perspectives. By uncovering hidden catalysts and risks early, you'll accelerate your decision-making and stay one step ahead of the market.

Seeking Fresh Alternatives Beyond Banks?

Some of the most interesting opportunities can move from quiet to breakout quickly, and by the time momentum is flying, the early entry point is gone, act now.

- Spot potential turnaround stories before they get caught in the hype cycle by scanning 19 high quality undiscovered gems, built around strong balance sheets and quietly improving fundamentals.

- Target resilient cash generators while prices are still under the radar for now by running the 45 high quality undervalued stocks, which filters for quality, cash flow and solid financial footing.

- Stack your income ideas with companies aiming to keep payments flowing by checking the 8 dividend fortresses, focused on stability, coverage and durable payout histories.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.