3 U.S. Manufacturing Stocks Built For Tariff Pressure

BorgWarner Inc. BWA | 0.00 |

Trade tensions between the United States and Canada are back in focus, with fresh talk of tariffs on autos, steel and softwood lumber increasing uncertainty for companies tied to cross border supply chains. For U.S. investors, this kind of disruption can create both risk and potential opportunity as domestic manufacturers adjust pricing power, sourcing and capacity. This article looks at three U.S. Domestic Manufacturing stocks from the screener that are exposed to this tariff story in different ways, all on the positive side of the thesis, to help you think through where this news might matter most in your portfolio decisions.

Lear (LEA)

Overview: Lear is a U.S. headquartered auto supplier that builds complete seating systems and complex electrical and wiring systems for major carmakers, with products that sit inside many light trucks, SUVs and passenger cars around the world.

Operations: Lear generates most of its revenue from Seating at about US$17.5b, alongside its E-Systems business at about US$6.3b, with a small offsetting amount reported in Other.

Market Cap: US$6.5b

Lear stands out in this tariff story because it already does much of its manufacturing inside the U.S., its direct import exposure from Canada and China has been described as modest, and management says most tariff costs have been recoverable from customers. At the same time, the company is tied into higher value seating and E-Systems content for EVs, is returning cash through buybacks, and analysts are using detailed forecasts and a DCF view that indicate the stock is trading below their estimate of fair value. The catch is that Lear still faces trade policy risk, customer concentration and funding risk. As a result, the potential upside depends on how comfortable investors are with those pressures on margins and cash flow.

Lear’s tariff resilience, EV content and buybacks have investors talking about a possible valuation gap, but the real question is whether the tradeoff between upside and pressure on margins is worth it, according to the DCF valuation analysis for Lear

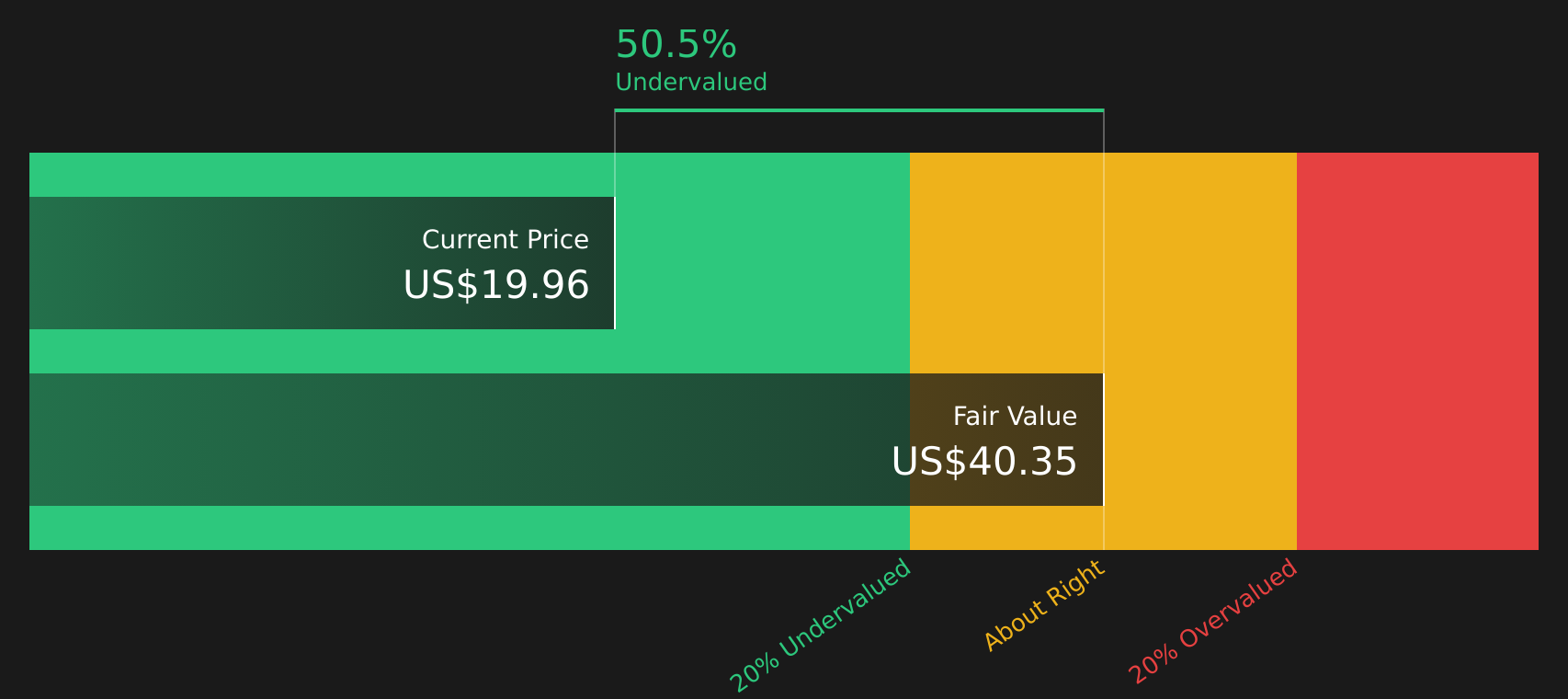

BorgWarner (BWA)

Overview: BorgWarner is a Michigan based auto supplier that provides key components for combustion, hybrid and electric vehicles, including turbochargers, power electronics, battery systems and drivetrain parts used by carmakers around the world.

Operations: BorgWarner generates most of its revenue from Turbos & Thermal Technologies at about US$5.8b and Drivetrain & Morse Systems at about US$5.7b, with additional contributions from PowerDrive Systems at about US$2.4b and Battery Energy Systems at about US$0.5b.

Market Cap: US$13.2b

BorgWarner is attracting fresh attention because it sits at the crossroads of traditional auto parts and electrification. It is also seen as a potential beneficiary of tougher U.S. trade policy toward Canada, given its Detroit base and limited Canada exposure. The company has been winning business in hybrid and EV systems and earning recognition for sustainability, yet still carries meaningful exposure to combustion products, a recently consolidated but challenged battery segment and tariff related cost swings highlighted on recent earnings calls. For investors trying to balance those cross currents, the mix of strong electrification demand, non auto opportunities such as data center related products, and ongoing tariff pass through efforts raises the question of whether the risk reward trade off is becoming more interesting here.

Electrification momentum at BorgWarner is starting to decouple from its combustion exposure, but tariff swings and the battery segment story are easy to miss until you read the 3 key rewards and 2 important warning signs

Adient (ADNT)

Overview: Adient is a global auto supplier that designs and manufactures complete seating systems and components such as frames, foams, head restraints, armrests and trim covers for passenger cars, commercial vehicles and light trucks, selling primarily to major automakers worldwide.

Operations: Adient generates most of its revenue from the Americas at about US$7.1b, alongside EMEA at about US$4.9b and Asia at about US$3.1b, with a small offsetting amount reported in Corporate/Eliminations.

Market Cap: US$1.5b

Adient sits at the intersection of tariff reshoring themes and higher value EV seating, with a large U.S. production base, new foam capacity in Michigan and premium comfort features such as ProForce Massage Flow and StepJoy that help it win business with both domestic and Asia based OEMs. At the same time, the balance sheet carries financing risk, China related tariff exposure has required careful mitigation, and earnings quality is affected by restructuring costs and one off items, while recent results have shifted from deep losses to modest profits. For investors, the combination of a discounted stock price, evolving fundamentals and meaningful execution risks makes Adient a tariff story that may warrant closer consideration rather than a quick judgment.

Adient’s move from deep losses to modest profits suggests a potential turning point for this tariff reshoring story, but the real twist lies within the 3 key rewards and 3 important warning signs (1 is major!)

The three stocks highlighted here are just a starting point, and the full U.S. Domestic Manufacturing screener on Simply Wall St surfaces 17 more companies in the U.S. Domestic Manufacturing screener with equally compelling tariff and reshoring narratives. Use the platform to identify, filter and analyze the specific catalysts, financial health factors and storylines that matter most to you so you can focus on the highest conviction U.S. manufacturing ideas in seconds.

Take Control of Your Investment Journey

If Lear or any of these companies sound like a great opportunity, register for FREE with Simply Wall St and add your companies to a Watchlist to monitor the share price against the fair value the ideal entry point. Once you've made your move, manage your holdings with our Portfolio Command Center that filters out the noise to deliver only the most critical, actionable updates. Throughout your journey, our Community allows you to filter the best ideas from thousands of investor perspectives. By uncovering hidden catalysts and risks early, you'll accelerate your decision-making and stay one step ahead of the market.

Seeking Fresh Alternatives Before They Fly?

Some of the sharpest breakouts start quietly, with momentum building in corners most investors ignore. Before these ideas stop flying under the radar, move with intent and get in early.

- Spot potential trend leaders early by scanning 52 AI infrastructure stocks that could gain from growing demand for data centers, chips and the backbone behind AI workloads while it still goes under followed.

- Track resilient income ideas using the curated 9 dividend fortresses that may offer higher yields while prices are still dropping or flat, before the crowd wakes up to the cash flow story.

- Hunt for under the radar value among the 19 high quality undiscovered gems that pass quality filters yet remain overlooked for now, giving you a shot at potential upside before momentum hits.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.