3 US Software Stocks Trading Below Cash Flow Value

Western Digital Corporation WDC | 0.00 |

With inflation signals mixed, central banks cautious and commodity trade pulses still important for growth, many investors are looking for stocks where current prices already reflect a lot of the worry. The Undervalued Stocks Based On Cash Flows screener focuses on companies that the SWS DCF model values above their current market price, based on their cash flow potential. That means you are looking at businesses where expectations may already be conservative. In this article, three stocks from the screener will be highlighted and their cash flow driven appeal will be broken down in simple, practical terms.

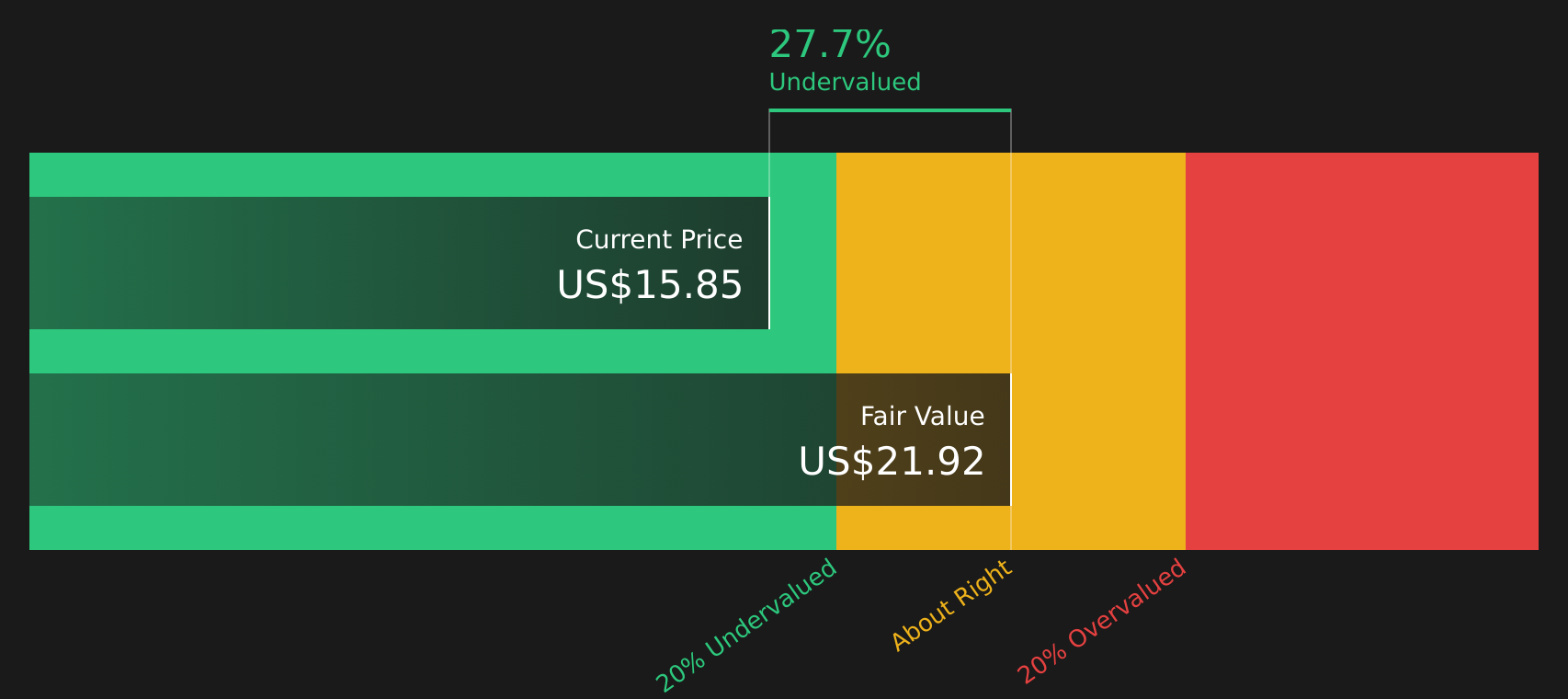

Flywire (FLYW)

Overview: Flywire is a Boston based payments and software company that helps education, healthcare, travel and B2B clients move money across borders, combining its own payment platform and global network with tools like invoicing, reconciliation and recurring billing so institutions and businesses can get paid more easily and accurately.

Operations: Flywire generates all of its US$677.7 million in revenue from data processing services, with roughly US$316.3 million coming from the Americas, US$257.8 million from Europe, the Middle East and Africa, and US$103.6 million from Asia Pacific.

Market Cap: US$1.9b

Flywire appears in this cash flow focused screener because its payment platform is tied directly to billings growth in sectors like education and healthcare. Recent customer wins and partnerships suggest an extended period of digital payment adoption, while a DCF value above the current share price points to a possible difference between cash flow potential and what the market is currently willing to pay. At the same time, the stock has a relatively high P/E and relies on higher risk non deposit funding, so a setback in cross border volumes, regulation or client acquisition could affect earnings more than investors might anticipate. For readers who want to see how these growth drivers and funding risks are reflected in a single, cash flow based view of Flywire, DCF valuation analysis for Flywire.

Flywire’s cross border growth story and high P/E only make sense if its cash flows ramp the way the market is starting to price in, yet one assumption inside the DCF valuation analysis for Flywire quietly shifts the whole picture

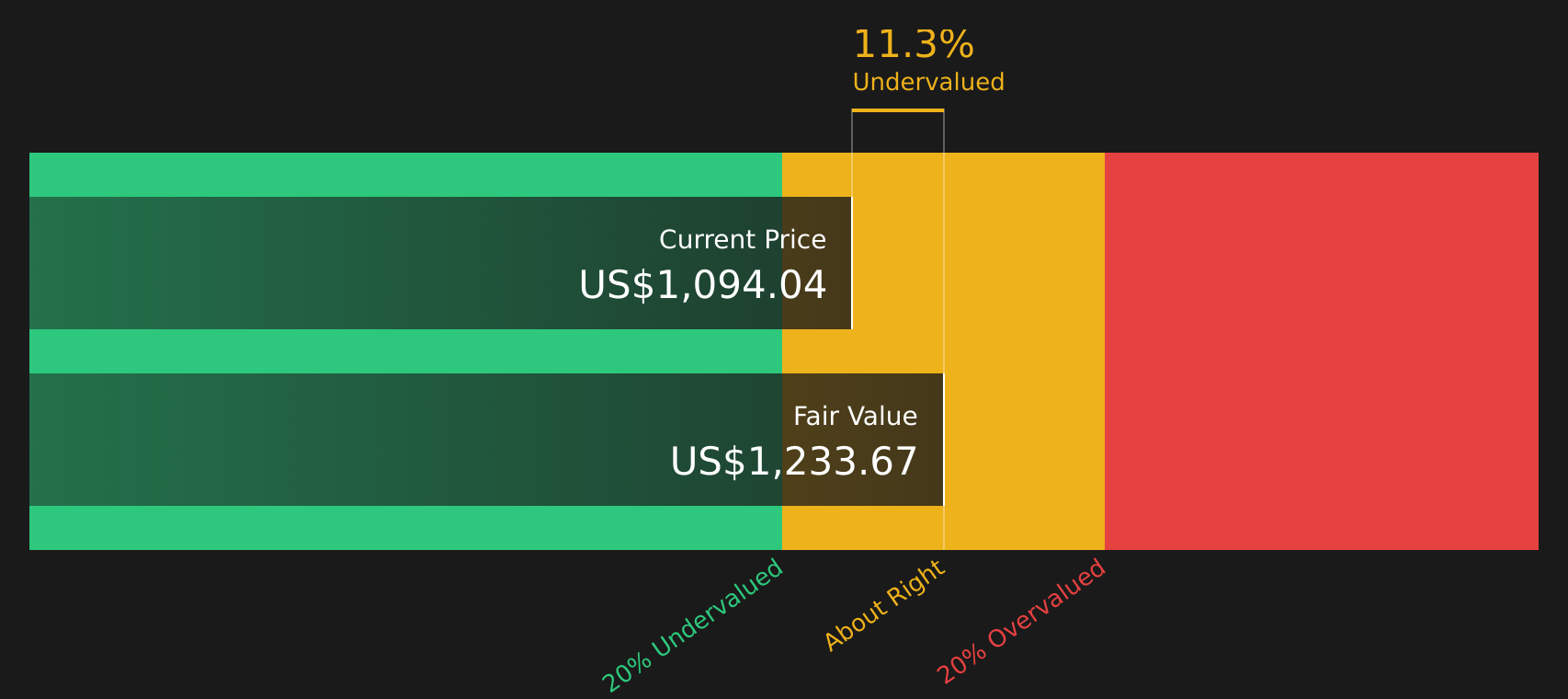

Western Digital (WDC)

Overview: Western Digital is a San Jose based data storage company that produces hard disk drives and storage systems for everything from consumer PCs and external drives to large cloud and AI data centers, selling through device makers, distributors and retailers worldwide.

Operations: Western Digital generates about US$11.8b in revenue from hard disk drives, with reported regional revenue including US$2.1b from Europe, the Middle East and Africa and a large segment adjustment item of US$9.7b.

Market Cap: US$257.2b

Western Digital plays a key role in AI data storage buildout, supplying high capacity HDDs and platforms to major hyperscale cloud customers while developing technologies such as UltraSMR and HAMR that target denser and lower cost storage. Analysts and recent news report strong earnings momentum, high current margins and a return on equity above 60%, supported by improving free cash flow and debt reduction. At the same time, the stock has been described as trading below an internally estimated cash flow value. However, revenue is heavily concentrated in a few large cloud buyers and outcomes depend on adoption of its newer drive technologies, so anyone considering this apparent value gap may wish to weigh customer concentration and technology execution risks carefully.

Western Digital’s strong margins, high return on equity and AI storage role suggest that the story may be bigger than a simple cyclical rebound, and the real twist could sit inside the analysis report for Western Digital

Seagate Technology Holdings (STX)

Overview: Seagate Technology Holdings is a global data storage company that supplies hard drives, solid state drives and external storage systems for PCs, consumer devices, gaming and large cloud and AI data centers, while also offering its Lyve edge to cloud platform for enterprises that need to store and move huge amounts of data across on premise and cloud infrastructure.

Operations: Seagate generates about US$11.0b in revenue from the manufacture and distribution of storage solutions, with most sales coming from the United States (US$5.4b) and Singapore (US$4.5b), alongside contributions from the Netherlands (US$1.1b) and other regions.

Market Cap: US$242.1b

Seagate Technology Holdings is positioned in AI and cloud data storage, supplying high capacity HAMR based Mozaic drives to hyperscale customers that report nearline storage demand is largely spoken for through 2027. Earnings and revenue are described as growing quickly, supported by pricing discipline, a build to order model and agreements that provide visibility into future exabyte shipments, while free cash flow has been described as very strong. The trade off is a very high P/E multiple, sizeable debt and rising competition from SSD and NAND technologies, with insider selling adding another layer to consider. For investors screening for cash flow supported growth stories where expectations are already demanding, Seagate’s mix of potential AI related upside and balance sheet risk may be a notable case study.

Seagate’s AI storage story is accelerating, but the real tension sits between its strong cash generation and that sizeable debt load. The full picture only comes into focus in the analysis report for Seagate Technology Holdings

The three stocks in this article are only a sample of the opportunity. The full Undervalued Stocks Based On Cash Flows results highlight 118 more companies where the SWS DCF model suggests similarly compelling cash flow stories, all bundled into the Undervalued Stocks Based On Cash Flows screener. Use Simply Wall St to identify and analyze the specific catalysts, cash flow trends and risk narratives that matter most to you so you can focus on the highest conviction ideas from that list.

Take Control of Your Investment Journey

If Seagate Technology Holdings or any of these companies have caught your attention, register for FREE with Simply Wall St and add your companies to a Watchlist to monitor the share price against the fair value and track any new developments as they happen. Once you've made your move, manage your holdings with our Portfolio Command Center that filters out the noise to deliver only the most critical, actionable updates. Throughout your journey, our Community allows you to filter the best ideas from thousands of investor perspectives. By uncovering hidden catalysts and risks early, you'll accelerate your decision-making and stay one step ahead of the market.

Seeking Fresh Alternatives Before They Fly?

Some of the best breakout stories are caught while momentum is building and attention is still dropping elsewhere. Scan these fresh ideas before the crowd moves in and get in early.

- Chase reliable income streams by scanning 8 dividend fortresses that focus on steady cash flows while yields remain under the radar for now, then decide which ones truly fit your risk tolerance.

- Spot early leaders in intelligent automation by reviewing 31 robotics and automation stocks, where companies powering factories, warehouses and devices could be building momentum before most investors start paying attention.

- Position portfolio exposure around energy infrastructure by checking 34 power grid technology and infrastructure stocks, highlighting companies tied to grid upgrades and resilience while these opportunities are still flying below the headlines.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.