3 US Stocks For Inflation Resistance And Strong Balance Sheets

Target Corporation TGT | 0.00 |

With the Federal Reserve keeping rates on hold but signaling it may still lift borrowing costs if inflation stays sticky, investors are being reminded that not all stocks handle price pressures in the same way. Companies with stronger balance sheets, resilient cash flows, and a record of disciplined capital returns often have more room to manage higher input costs or funding expenses. This article looks at how that backdrop, along with Kevin Warsh’s more guarded communication style, might affect a selection of stocks exposed to the latest Fed news, and reveals 3 candidates from an Inflation-Resistant Stocks screener that could warrant a closer look.

Target (TGT)

Overview: Target is a large US general merchandise retailer that sells everything from apparel and beauty products to groceries, electronics, home goods, and household essentials through its nationwide stores and digital channels, including Target.com.

Operations: Target generates all of its approximately US$106.4b in annual revenue from U.S. retail operations.

Market Cap: US$58.1b

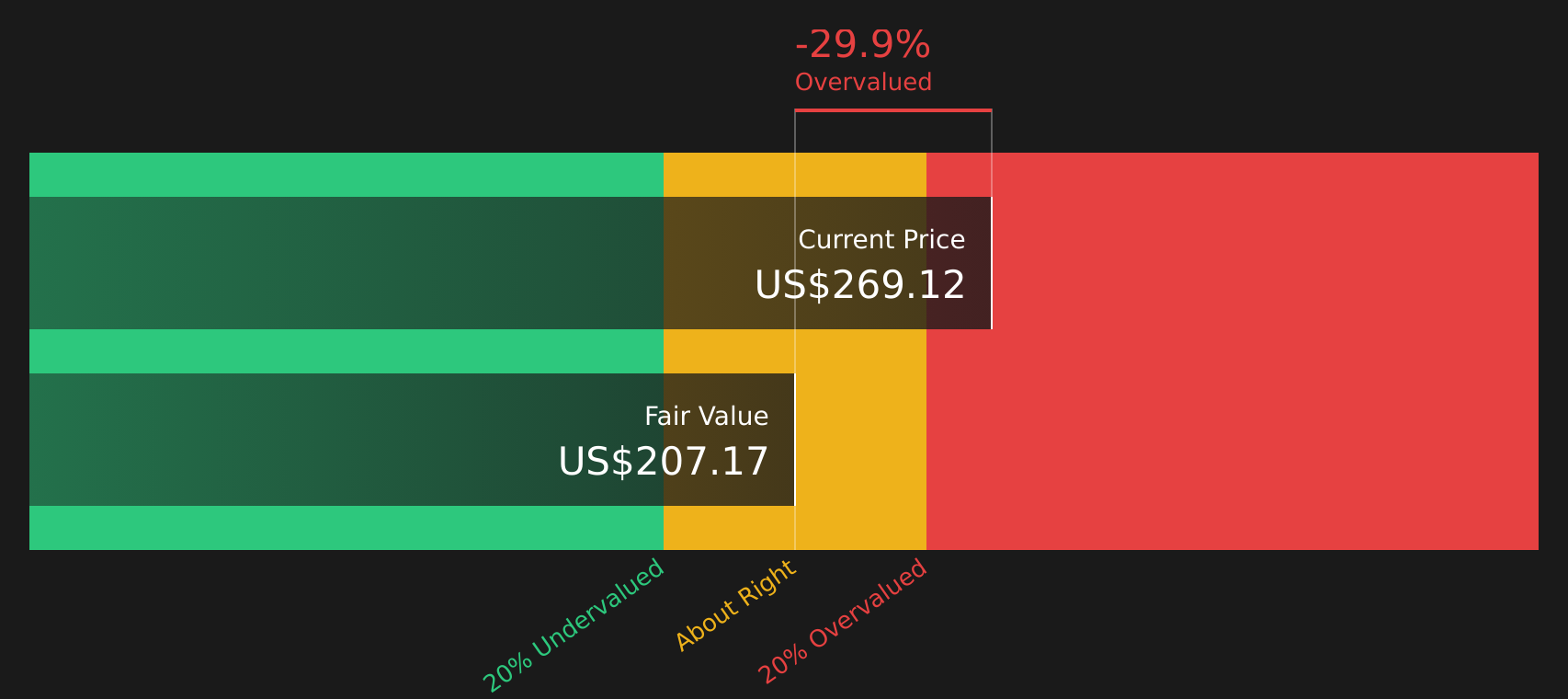

Investors watching inflation and the Fed’s tougher tone may find Target interesting because it combines everyday essentials, brand strength, and a long history of dividend growth with an active reinvestment program in digital, AI, and store upgrades. Recent quarters show improving traffic, higher comps, and raised guidance. Analysts note a potential multi year recovery in profitability, while the stock still carries questions around high debt, thinner margins, and insider selling. With a P/E below many peers and a dividend yield above 3%, the company offers income and potential re rating. The key issue is how Target manages turnaround progress alongside retail competition, cost pressures, and changing consumer habits.

Target’s mix of essential spending, a P/E below many peers, and dividend income could be masking a more interesting setup around valuation. To see how the current price stacks up against the story, review the DCF valuation analysis for Target

Sherwin-Williams (SHW)

Overview: Sherwin-Williams is a global paint and coatings company that sells everything from household paints for DIY projects to high performance industrial coatings used on buildings, cars, packaging, and infrastructure, mainly through its own paint stores and major retailers.

Operations: Sherwin-Williams generates most of its roughly US$29.9b in annual revenue from the Paint Stores Group at about US$13.7b, followed by the Consumer Brands Group at about US$8.8b and the Performance Coatings Group at about US$6.9b, with the majority coming from the United States and the rest from international markets.

Market Cap: US$76.9b

Investors looking at inflation and a more hawkish Fed may find Sherwin-Williams interesting because paints and coatings often hold pricing power, which can help offset higher raw material and financing costs. The company is still investing heavily in its store network, customer programs, and R&D, while analysts highlight both high profitability metrics and meaningful leverage that makes earnings more sensitive to rates and housing activity. Recent commentary from management points to a “slower for longer” demand backdrop, yet they continue to plan around the idea that it is a question of when, not if, volumes improve. How that balance between pricing strength, debt load, and housing exposure plays out could be central to Sherwin-Williams’ role in an inflation resistant portfolio.

Sherwin-Williams looks like pricing strength wrapped around meaningful leverage, and that mix often gets misread when rates and housing are in focus. Before you decide where the balance tilts, review the 2 key rewards and 1 important warning sign

Ecolab (ECL)

Overview: Ecolab provides water treatment, cleaning, hygiene, and infection prevention products and services to industries such as food and beverage, healthcare, hospitality, manufacturing, and life sciences across global markets.

Operations: Ecolab generates most of its revenue from Global Water at about US$7.8b and Global Institutional & Specialty at about US$6.0b, with additional contributions from Global Pest Elimination at about US$1.2b and Global Life Sciences at about US$0.7b, plus an unallocated currency impact of about US$0.7b.

Market Cap: US$75.7b

Ecolab stands out in a more hawkish Fed setting because its cleaning and sanitation solutions are tied to essential activities, which can support pricing power when inflation lingers. The company is leaning into its One Ecolab program, value based pricing, and AI enabled water and data center solutions. At the same time, Q1 2026 results and guidance highlight solid revenue and earnings and high quality earnings. Yet investors also need to weigh a very high P/E, high debt levels, and the impact of new borrowing for acquisitions, all of which can become more sensitive if rates rise. The real question is whether Ecolab’s mix of necessity demand, pricing discipline, and digital tools is strong enough to justify that premium in a higher for longer rate world.

Ecolab’s premium P/E and essential services story may be missing a key piece. The real tension sits between its pricing power, debt load, and new borrowing for acquisitions, which is unpacked in the analysis report for Ecolab

The three stocks here are a starting point, and the full Inflation-Resistant Stocks screener surfaces 16 more companies with equally compelling stories around balance sheet strength, pricing power, and inflation resilience, all captured in the Inflation-Resistant Stocks screener. Use Simply Wall St to identify, filter, and analyze the specific catalysts and narratives that matter most to you so you can focus on your highest conviction ideas.

Take Control of Your Investment Journey

If Ecolab or any of these companies sound like a great opportunity, register for FREE with Simply Wall St and add your companies to a Watchlist to monitor the share price against the fair value the ideal entry point. Once you've made your move, manage your holdings with our Portfolio Command Center that filters out the noise to deliver only the most critical, actionable updates. Throughout your journey, our Community allows you to filter the best ideas from thousands of investor perspectives. By uncovering hidden catalysts and risks early, you'll accelerate your decision-making and stay one step ahead of the market.

Seeking Alternatives Before Momentum Flies Past?

Fresh ideas move first, and the best entry points often appear before the crowd spots the breakout. Do not get caught watching from the sidelines, consider your options carefully.

- Explore potential early-stage candidates by scanning 24 elite penny stocks with strong financials that pair small size with comparatively stronger financial footing before momentum significantly changes valuations.

- Look for under the radar opportunities with the curated 20 high quality undiscovered gems that focuses on quality fundamentals while they may still be developing.

- Evaluate resilient cash generators through the hand picked 8 dividend fortresses designed for investors who prioritize income durability while certain prices may not be widely followed.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.